Much of this risk can be mitigated using a solution like InvestGlass to automate your KYC and remediation. By automating Know Your Customer processes, companies can seamlessly onboard users remotely and securely, which is essential in our increasingly digital world.

Automation significantly enhances regulatory compliance and fraud prevention for businesses. Approximately 32% of companies implement automation specifically to streamline compliance processes and meet stringent regulatory demands (Secureframe). Additionally, adopting AI-driven automation can reduce fraud detection time by up to 60%, effectively protecting financial assets and operational integrity (Coinlaw).

Moreover, automated KYC solutions help maintain high user conversion rates, fuelling business growth. By streamlining these processes, companies can achieve a positive return on investment (ROI) through efficient resource management and by protecting themselves from financial crimes like money laundering and terrorist financing. This comprehensive approach not only enhances operational efficiency but also fortifies your business’s defences against myriad risks.

What is Automated KYC?

Automated KYC, or Know Your Customer, refers to the use of technology to streamline verifying a customer’s identity. This automated system leverages tools like biometric verification and document recognition software to quickly and accurately confirm identities. These technologies help to minimise human error and bypass lengthy manual checks.

Additionally, automated KYC employs advanced data analytics to ensure compliance with regulatory standards. By doing so, it not only speeds up the onboarding process but also enhances the overall customer experience. Automated solutions reduce the time and resources spent on manual reviews, delivering a smoother and more efficient service.

Automated KYC transforms traditional verification methods into a faster, more reliable, and regulatory-compliant process, ensuring businesses meet legal requirements while offering a user-friendly experience.

What are the key areas where an automated KYC solution excels beyond competitors?

When evaluating automated Know Your Customer (KYC) solutions, it’s essential to understand the primary features that set leading platforms apart. These standout areas are often reflected in user feedback from reputable review sites like G2. Here’s how top-tier automated KYC solutions excel:

1. Efficiency and Speed

Automated KYC solutions drastically reduce onboarding time. Unlike manual processes that could take days or even weeks, automated systems verify identities in mere minutes. This acceleration is vital for businesses looking to improve customer experience and enhance operational efficiency.

2. Accuracy and Compliance

Top solutions utilize advanced algorithms and machine learning to enhance the accuracy of identity verification. By minimizing human error, these systems ensure that compliance with regulations such as AML (Anti-Money Laundering) and CFT (Counter-Terrorism Financing) is consistently maintained.

3. Scalability

As businesses grow, so do their needs. Leading KYC platforms provide scalable solutions that can handle increasing volumes of verifications without compromising speed or accuracy. This flexibility is crucial for businesses planning to expand their customer base rapidly.

4. Cost-Effectiveness

Automated solutions often lead to significant cost savings by reducing the need for extensive manual intervention. The cost-per-verification typically decreases as automation levels rise, which is economically beneficial for enterprises processing large numbers of customer verifications.

5. Seamless Integration

Modern KYC solutions offer seamless integration with existing business systems and platforms through APIs. This ease of integration minimizes disruption and allows for a smooth transition from traditional to automated systems.

6. User Experience

User-friendly interfaces and intuitive workflows are hallmarks of superior KYC platforms. By providing a straightforward, hassle-free verification process, these solutions enhance user satisfaction and engagement.

In summary, automated KYC solutions outperform competitors by providing speedy, accurate, and cost-effective identity verification, all while offering seamless integration and a satisfying user experience. These factors not only ensure compliance but also optimize business operations, setting these solutions apart in the crowded marketplace.

How Automated KYC Facilitates Global Expansion and Scaling?

Automated KYC (Know Your Customer) solutions are game changers for businesses aiming to scale rapidly and penetrate global markets. Here’s how they support international growth:

- Efficient Verification Processes: Automated KYC systems process large volumes of customer data swiftly, allowing businesses to verify thousands of applicants without delay. This efficiency is crucial for companies experiencing rapid growth.

- Language and Cultural Adaptability: These systems often incorporate advanced technology, such as AI and machine learning, to handle diverse languages and cultural contexts. This adaptability ensures that businesses can operate smoothly in multiple regions worldwide.

- Regulatory Compliance Across Borders: Navigating different countries’ regulatory landscapes can be complex. Automated KYC solutions integrate compliance checks for various jurisdictions, helping businesses meet local legal requirements effortlessly.

- Enhanced Security Measures: With features like biometric verification and document authentication, automated KYC enhances security and reduces fraud risk. This protection is vital as businesses expand their footprint globally.

By leveraging automated KYC, companies can streamline their customer onboarding process, reduce operational costs, and maintain robust compliance standards, all of which are essential components for scaling up and entering international markets.

Discover the Cost and Time Benefits of an Automated KYC Solution?

Implementing an automated KYC (Know Your Customer) solution can revolutionize your client onboarding process by offering substantial financial and time-saving advantages. Here’s how:

- Significant Cost Savings: Companies can achieve up to a 40% reduction in costs associated with compliance operations. Automating these processes minimizes the need for extensive manual intervention, leading to a leaner and more efficient compliance team.

- Rapid Verification Process: The average speed for customer verification is reduced to just 30 seconds. This quick turnaround not only enhances user experience but also enables your business to engage more clients and reduce wait times significantly.

- Enhanced Efficiency: By decreasing the time spent on compliance tasks by up to 70%, your team can focus on more strategic initiatives. Automation streamlines routine checks, freeing up valuable resources to drive your business forward.

These benefits illustrate why many businesses are turning to automated KYC solutions to bolster efficiency and improve client satisfaction. With faster processes and reduced operational costs, your business can thrive in an increasingly competitive market.

How can businesses onboard clients worldwide with automated KYC?

In today’s global marketplace, businesses are increasingly seeking efficient strategies to onboard clients from across the globe. Automated Know Your Customer (KYC) processes are revolutionizing this effort by providing a streamlined, effective solution. Here’s how businesses can leverage these systems to reach international clients seamlessly.

1. Comprehensive Document Verification

Automated KYC systems can verify thousands of document types from over 220 countries and territories. This extensive reach ensures that no matter where your clients are located, their documents can be authenticated quickly and accurately. This capability removes geographical barriers and enhances the overall user experience.

2. Localized User Experience

To cater to a diverse clientele, offering a localized user experience is crucial. Automated KYC platforms often include support for over 30 languages. This feature not only eases the onboarding process for non-native speakers but also builds trust and improves satisfaction, as clients can engage with your services in their preferred language.

3. Enhanced Security with Automation

Automation in KYC processes minimizes human error, ensuring higher security standards. By using sophisticated technologies like AI and machine learning, these systems can identify fraudulent documents more effectively than manual checks. This provides businesses with a reliable defence against identity theft and compliance breaches.

4. Faster Onboarding Process

Traditional onboarding processes can be time-consuming, often leading to client drop-off. Automated KYC significantly speeds up this process by offering real-time verification. Clients will appreciate the quick turnaround, allowing them to access your services or products without unnecessary delays.

5. Cost Efficiency and Scalability

Implementing an automated KYC solution can reduce operational costs associated with manual processes. Moreover, these systems are scalable, allowing businesses to adjust to increased demands effortlessly. Whether you’re onboarding a hundred or a thousand clients, automation helps maintain efficiency and effectiveness.

Conclusion

By adopting automated KYC solutions, businesses can easily onboard clients worldwide with greater efficiency, accuracy, and personalization. Streamlining the verification process not only enhances security and compliance but also provides a superior client experience, setting your business apart in a competitive global market.

How Automated KYC Solutions Save Money and Resources?

Implementing automated Know Your Customer (KYC) solutions can significantly boost your company’s efficiency while reducing overall expenses. Here’s how:

- Reduction in Staffing Costs: Automating KYC processes means fewer manual verifications, reducing the need for large compliance teams. This can lead to substantial savings on salaries and training costs.

- Minimization of Human Error: Automated solutions provide consistent and accurate results, decreasing the chance of manual errors that can lead to costly compliance violations and reputational damage.

- Time Efficiency: Automation accelerates the verification process, allowing your team to onboard clients faster. This speedy turnaround can increase customer satisfaction and retention, ultimately boosting revenue.

- Resource Allocation: With routine tasks handled by technology, your team can redirect their focus to impactful, strategic work that drives business growth and innovation.

- Scalability: As your business grows, automated KYC solutions can easily scale with you, handling higher volumes without a proportional increase in costs.

By leveraging these advantages, automated KYC solutions not only streamline your compliance framework but also optimize the allocation of resources across your organization.

How Does Ongoing AML Monitoring Help in Staying Updated on a Client’s Status?

Ongoing Anti-Money Laundering (AML) monitoring plays a crucial role in keeping you informed about your client’s current status and potential risks. Here’s how it works:

- Continuous Screening Against Global Databases

Regular checks are performed using international databases that include sanctions, watchlists, and political exposed persons (PEPs). This ensures you’re always aware of any changes in your client’s status, helping you manage compliance risks effectively. - Identification of Adverse Media

By monitoring adverse media sources, you can quickly identify if a client is involved in negative publicity or legal issues. This proactive approach helps in mitigating potential reputational damage early on. - Risk Minimization

By staying updated through ongoing checks, businesses can avoid associating with illegitimate or high-risk clients. This reduces the potential for future liabilities and enhances your credibility. - Automated Alerts and Notifications

Many AML systems offer automated alerts for any changes in a client’s status, ensuring that you stay informed in real-time without constant manual oversight.

Implementing ongoing AML monitoring keeps you informed, safeguards your business from potential threats, and ensures long-term success by maintaining a secure and compliant client base.

How Automated KYC Directs Focus to Edge Cases?

Automated Know Your Customer (KYC) processes can effectively address edge or corner cases by streamlining routine tasks. This allows teams to dedicate their efforts to more complex customer profiles that require human attention.

Here’s How It Works:

- Efficiency and Accuracy: Automated KYC handles most straightforward applications with speed and precision. This reduces the workload dramatically by managing up to 95% of cases without requiring manual intervention.

- Resource Allocation: By freeing up personnel from routine checks, businesses can concentrate on the 5% that are particularly challenging. This includes scenarios involving ambiguous regulations, unusual customer behaviours, or international compliance differences.

- Risk Prioritization: Automation systems flag high-risk or unusual activities immediately. This prioritization allows experts to swiftly address and resolve potential compliance issues with focused strategies.

- Enhanced Customer Experience: While automation ensures a seamless process for most users, it provides personalized attention when necessary. This dual approach enhances customer satisfaction and builds trust.

In essence, automated KYC transforms how companies manage their compliance processes, focusing human expertise where it’s most impactful and leaving routine checks to efficient technology.

How does automated KYC verification speed up onboarding?

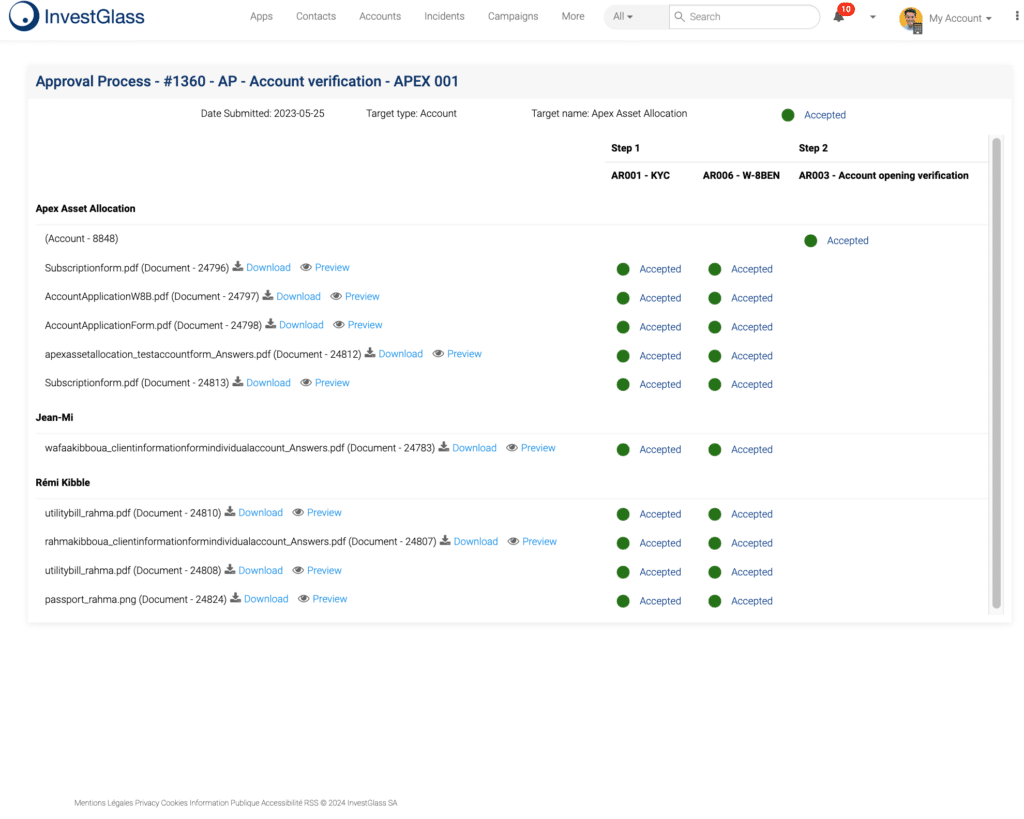

Last but not least, once all information is entered and recorded, companies need to be able to accept or reject customers based on their answers, identity verification, and name check. Banking institutions usually use solutions that provide approval processes for account opening and customer onboarding.

Automated KYC onboarding plays a crucial role in expediting this process. It utilizes biometric identity verification and document recognition technology to swiftly and accurately verify customer identities. These technologies minimize manual errors and enhance accuracy, ensuring regulatory compliance.

Moreover, data analytics is employed to process and analyze information efficiently. This not only speeds up the onboarding process but also contributes to a seamless customer experience. By reducing the time and effort traditionally required, automated KYC enables businesses to onboard customers faster, while maintaining high standards of compliance and security.

How does automated KYC help in detecting fraud?

How can financial institutions, banks, and other businesses perform a complete and compliant KYC process during account opening and customer onboarding? The KYC process can be simplified into five steps enhancing compliance and avoiding fraud:

- Collect Information: Gather essential data from the customer, ensuring all necessary fields are filled accurately.

- Check Documents: Utilize AI-powered tools to detect any graphic editor traces, ensuring that submitted documents are authentic and unaltered.

- Validate Information: Cross-reference collected data with trusted databases. Automated systems can screen against a blocklist of over 1 million known fraudsters, instantly flagging suspicious individuals.

- Start Remediation: If discrepancies are found, automated systems can initiate remediation steps. These include detecting spoofing attempts and verifying the legitimacy of the customer’s identity through advanced behavioral risk scoring.

- Approval Processes: Once all information is validated and any issues are resolved, proceed with approval to onboard the customer securely.

By integrating AI algorithms into the KYC process, businesses not only streamline operations but also strengthen their defences against fraud. These technologies work tirelessly to uncover potential fraud activity, ensuring a more secure and compliant onboarding process.

How does behavioural analysis contribute to fraud detection?

Behavioural analysis evaluates user actions, assigning risk scores based on detected patterns. This helps identify unusual behaviour that may indicate fraudulent activity, thus enhancing the detection process.

How are known fraudsters identified in real time?

By maintaining and continuously updating a comprehensive blocklist of over a million known fraudsters, these systems can instantly cross-reference new data against this list to identify and flag suspicious individuals quickly.

How can automated systems identify attempts at identity spoofing?

Automated systems use advanced pattern recognition to detect anomalies in identity verification processes, flagging potential spoofing attempts that could compromise security.

How does AI help detect document forgery?

AI algorithms can analyze documents to identify signs of tampering, such as traces left by graphic editing tools, ensuring the authenticity of submitted documentation.

How do AI algorithms assist in detecting fraudsters in the KYC process?

Once the data collection is made, you need to check the identity of the customers and the validity of their documents. To compare the data, Artificial Intelligence should extract the data from the records (ID, passport, debit/credit card, proof of residence, corporation documents, etc.) and double-cross it against the information manually entered. This comparison check is a basic, yet useful, pre-verification.

Beyond these initial steps, AI algorithms offer advanced capabilities to detect fraudsters more effectively:

- Reveal Manipulations: AI can identify graphic editor traces, ensuring that submitted documents haven’t been tampered with.

- Detect Spoofing Attempts: These algorithms are equipped to recognize and flag attempts to spoof identity, enhancing security measures.

- Comprehensive Fraud Screening: AI systems efficiently manage and cross-reference vast datasets by screening a blocklist of over a million known fraudsters.

- Behavioural Analysis: AI assigns behavioural risk scores, analysing patterns in user behaviour to uncover potential fraud activity that may go unnoticed in manual checks.

Integrating these AI-driven insights into the KYC process strengthens not only fraud detection but also streamlines verification, providing a robust defence against fraudulent activities.

How can a business integrate automated KYC solutions with their existing tech stack?

Indeed, for part of the second stage and the third one, InvestGlass connects with Regtech partners to provide seamless integration and complete KYC compliance. We also connect with fintech companies providing additional depth.

To ensure a smooth integration with your existing tech stack, InvestGlass offers multiple options:

- Web SDK: Easily embed KYC solutions directly into your web applications, allowing for a streamlined user experience.

- Mobile SDK: Integrate seamlessly with mobile platforms, ensuring your customers can access services on the go.

- RESTful API: For those with more complex systems, our API provides the flexibility to tailor the integration to your specific needs.

Rest assured, our solutions are designed to maintain high reliability, offering 99.9% uptime so your operations run without interruptions. This commitment to stability ensures that your business can rely on consistent performance as you enhance your compliance capabilities.

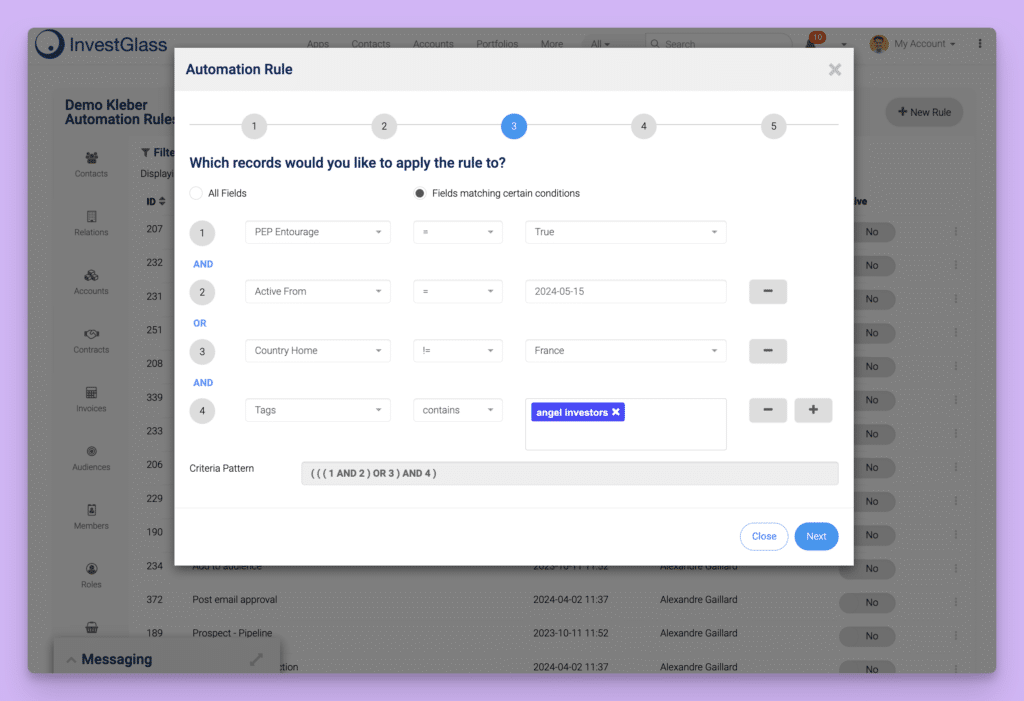

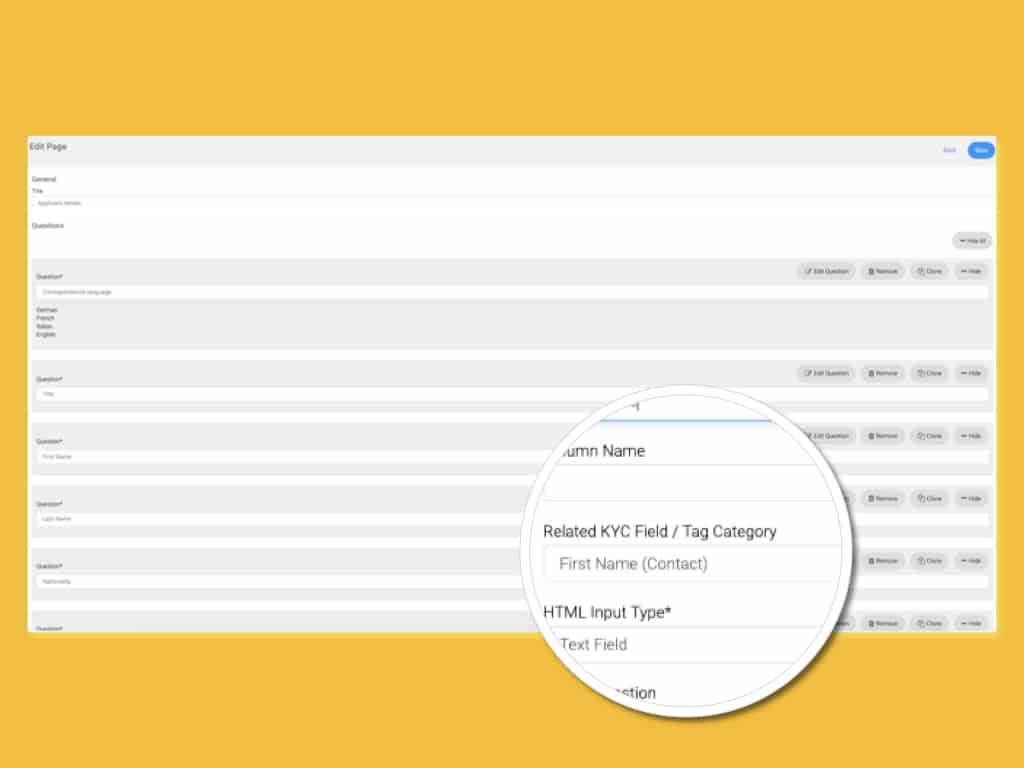

How can the KYC process be customized to fit specific policies?

Last but not least, once all information is entered and recorded, companies need to be able to accept or reject customers based on their answers, identity verification, and name check. Banking institutions usually use solutions that provide approval processes for account opening and customer onboarding.

To achieve this, a flexible KYC process is essential. It must be adaptable to your specific policies, ensuring compliance without compromising efficiency. Automated systems can handle up to 95% of routine verifications, allowing your team to concentrate on complex cases that require personalized attention.

Moreover, a robust system should support global operations, enabling verification of over 14,000 types of documents from 220+ countries and territories. This international capability is further enhanced by localization features supporting more than 30 languages, smoothing the onboarding experience for diverse customer bases.

These enhancements ensure that your KYC process not only meets regulatory demands but also aligns seamlessly with your organizational goals, providing a comprehensive and customizable solution.

What makes the user-friendly verification process quick and efficient?

The customer experience and engagement should remain positive and the speed of the process should remain as fast as possible. To achieve this, implementing customer onboarding automation can be a game-changer. By removing the hassle of manual form-filling, applicants breeze through the process without unnecessary delays.

Moreover, instant document pre-checks ensure that all submissions are accurate and complete, minimizing back-and-forth communication. Real-time tooltips offer immediate assistance, guiding users through each step, so they get verified successfully on the first attempt.

This approach not only enhances user satisfaction but also significantly boosts efficiency, making the verification process seamless and swift.

InvestGlass the best tool to automate your KYC

InvestGlass stands at the forefront of this revolution, offering a comprehensive platform that streamlines compliance, enhances customer experience, and mitigates risks. By automating KYC and AML processes, InvestGlass enables businesses to onboard clients efficiently, reduce operational costs, and ensure adherence to ever-changing regulatory requirements.

Whether you’re looking to scale globally, safeguard your business against fraud, or improve your bottom line, InvestGlass delivers a tailored, robust solution that integrates seamlessly into your existing systems. Its user-friendly interface, advanced fraud detection, and commitment to compliance make it the go-to choice for businesses striving for growth and resilience in an increasingly competitive market.

Choose InvestGlass to transform your compliance operations, drive efficiency, and focus on what truly matters: growing your business with confidence.

Frequently Asked Questions

1. What is automated KYC and why is it important?

Automated Know Your Customer (KYC) uses AI, biometrics, and document verification to confirm identities quickly and accurately. InvestGlass automates this process, reducing manual errors, ensuring compliance, and delivering a smoother onboarding experience.

2. How does InvestGlass improve compliance with regulations?

Regulations such as AML and CFT demand strict oversight. InvestGlass automates compliance checks, monitors client status against global watchlists, and provides real-time alerts to ensure you remain compliant across multiple jurisdictions.

3. Can automated KYC help prevent fraud?

Yes. Fraud detection is strengthened through AI-driven analysis, spoofing detection, and behavioural risk scoring. InvestGlass combines these tools with ongoing AML monitoring, protecting your business against identity theft and financial crime.

4. How much faster is onboarding with InvestGlass?

Manual onboarding can take days, but InvestGlass reduces verification to under a minute. With biometric checks and instant document pre-validation, customers enjoy a seamless onboarding journey while businesses cut drop-offs.

5. How does InvestGlass support global scalability?

InvestGlass verifies over 14,000 document types across 220+ countries, supports more than 30 languages, and adapts to regional compliance frameworks. This makes it the ideal solution for businesses expanding internationally.

6. What integration options does InvestGlass provide?

InvestGlass offers web and mobile SDKs as well as a RESTful API for smooth integration with existing platforms. This flexibility ensures KYC automation fits seamlessly into your current tech stack without disruption.

7. Is automated KYC cost-effective with InvestGlass?

Yes. By automating up to 95% of verifications, InvestGlass reduces staffing costs, minimises manual reviews, and lowers compliance expenses: delivering a strong ROI while maintaining efficiency at scale.

8. How does InvestGlass handle complex or high-risk cases?

Routine checks are automated, freeing compliance teams to focus on edge cases. InvestGlass flags suspicious profiles with advanced risk scoring, allowing human experts to prioritise and resolve complex scenarios quickly.

9. How does automated KYC improve customer experience?

InvestGlass provides a frictionless process with real-time tooltips, instant document validation, and multilingual support. This user-first approach keeps conversion rates high and builds trust from the first interaction.

10. Why choose InvestGlass for automated KYC and AML?

InvestGlass offers a Swiss-hosted, secure, and fully customisable KYC solution that combines automation, fraud prevention, and regulatory compliance. It empowers businesses to scale globally while staying safe, efficient, and client-focused.

Related articles

Swiss Sovereign CRM: Built on AI.

Ready to act.