Introduction

SaaS customer onboarding software is critical for regulated financial institutions, including banks, wealth managers, insurers, and real estate firms. The stakes for onboarding in financial services have never been higher. In 2025, B2B SaaS sales cycles average 84 days according to HubSpot data, but the real challenge begins after the contract is signed. SaaS benchmarks consistently show 5-7% monthly churn rates, with studies indicating that optimized onboarding can reduce this figure by 20-30%.

This guide is intended for compliance officers, operations leaders, and client onboarding teams at banks, wealth managers, insurers, and real estate firms. Effective onboarding software is essential for reducing compliance risk, accelerating revenue recognition, and improving client satisfaction in regulated industries. For banks, wealth managers, insurers, and real estate firms operating under strict regulatory frameworks, the onboarding process is where compliance meets client experience, and where both can fail spectacularly. SaaS businesses and SaaS companies in regulated industries face unique onboarding challenges, as they must balance strict compliance requirements with delivering a seamless client experience.

This guide focuses specifically on SaaS customer onboarding software for regulated industries. We’re not talking about generic project management tools or consumer-facing app walkthroughs. We’re addressing the complex, compliance-heavy journey of bringing B2B clients whether high-net-worth individuals, corporate banking clients, or institutional investors from contract signature to first measurable value. InvestGlass, a Swiss sovereign CRM and automation platform, is purpose-built for exactly these sectors: banks, private banks, wealth managers, insurance firms, real estate entities, and the public sector. The right onboarding tools are essential for streamlining onboarding for both your team and clients, ensuring intuitive workflows and efficient collaboration.

Poor onboarding in financial services creates tangible regulatory and revenue risk. Failed KYC (Know Your Customer) checks can trigger FINMA (Swiss Financial Market Supervisory Authority) inquiries. Slow account openings push AUM (Assets Under Management) booking into the next quarter. Missed MiFID II (Markets in Financial Instruments Directive II) suitability assessments expose firms to fines and client complaints. Manual KYC processes for private banking clients can stretch to 15-20 business days versus 2-3 days with digital flows, delays that translate directly into lost revenue and eroded client trust. When relationships in wealth management often last 10-20 years, the first impression during onboarding sets the tone for everything that follows.

What follows is a practical, software-focused guide to selecting, implementing, and optimizing SaaS customer onboarding software for regulated financial institutions in 2024-2026. We’ll cover essential features, real-world workflows, best practices, and the specific capabilities that make InvestGlass a strong fit for institutions prioritizing Swiss data sovereignty and integrated financial workflows. Choosing onboarding software that can streamline onboarding for both your team and clients is critical to improving user engagement and accelerating time-to-value.

Glossary and Regulatory Background

Before diving into the details, here is a brief glossary of key terms and regulatory frameworks relevant to onboarding in financial services:

- KYC (Know Your Customer): Regulatory process for verifying the identity of clients and assessing potential risks of illegal intentions for the business relationship.

- UBO (Ultimate Beneficial Owner): The individual(s) who ultimately own or control a client, especially relevant for corporate and institutional clients.

- MiFID II (Markets in Financial Instruments Directive II): European Union legislation that regulates firms providing services to clients linked to financial instruments, focusing on transparency and investor protection.

- FATCA/CRS (Foreign Account Tax Compliance Act/Common Reporting Standard): International standards for tax reporting and information exchange to prevent tax evasion.

- AML (Anti-Money Laundering): Laws and procedures designed to prevent criminals from disguising illegally obtained funds as legitimate income.

- AMLD5/6 (5th/6th Anti-Money Laundering Directive): EU directives enhancing due diligence and reporting requirements for financial institutions.

- FINMA: The Swiss Financial Market Supervisory Authority, responsible for financial regulation in Switzerland.

- Customer Onboarding: The end-to-end process of bringing a new client from contract signature to first measurable value, including KYC, product setup, and relationship establishment.

- User Onboarding: The process of guiding individual users (often within a client organization) through initial product activation and feature adoption.

- Digital KYC: The use of digital tools and workflows to automate and streamline the KYC process.

What Is SaaS Customer Onboarding Software?

SaaS customer onboarding software is a cloud-based platform designed to guide new B2B clients from contract signature through to first measurable value, whether that’s product activation, task completion, or engagement milestones like first login or feature adoption. In practical terms, these onboarding tools automate task assignment, facilitate client communication via portals and automated emails, manage documentation collection including forms and digital signatures and track onboarding progress against predefined milestones.

Key Definitions at First Mention:

- KYC (Know Your Customer): A regulatory process for verifying client identity and assessing risk.

- UBO (Ultimate Beneficial Owner): The person(s) who ultimately own or control a company or account.

- MiFID II (Markets in Financial Instruments Directive II): EU regulation for transparency and investor protection in financial markets.

- FATCA/CRS (Foreign Account Tax Compliance Act/Common Reporting Standard): International tax reporting standards.

- AML (Anti-Money Laundering): Laws and procedures to prevent money laundering.

Relationship Between Customer Onboarding, User Onboarding, and Digital KYC

- Customer Onboarding: Refers to the overall process of integrating a new client organization, including compliance, documentation, and product setup.

- User Onboarding: Focuses on individual users within the client organization, guiding them through product features and initial usage.

- Digital KYC: A subset of onboarding, specifically addressing the digital verification of client identity and regulatory checks.

Customer onboarding tools and user onboarding tools are specifically designed to automate and streamline the onboarding process for both customers and users, enhancing engagement and accelerating time-to-value.

For financial institutions, the customer onboarding process looks different than in other industries. Examples include:

- Opening an investment account for a new HNWI (High-Net-Worth Individual) client

- Setting up discretionary portfolio mandates

- Activating an insurance policy with full fact-finding documentation

- Onboarding corporate banking clients with complex UBO structures

- Integrating external asset managers into a custodian platform

Unlike generic project management tools such as Asana or Trello, or spreadsheets like Excel, onboarding software is purpose-built for recurring client journeys. It offers built-in client collaboration, dynamic KYC data capture, role-based approvals, and compliance audit trails that spreadsheets and email chains simply cannot provide. Onboarding projects can be automated and triggered immediately after a deal closes, ensuring a smooth transition for new customers and a seamless onboarding process.

InvestGlass combines CRM, digital onboarding & KYC, workflow automation, and a client portal in a single Swiss-hosted platform. This integration handles the entire onboarding lifecycle without requiring clients or internal teams to switch between disconnected systems. Onboarding software should also integrate seamlessly with existing tools, such as CRM systems, to maintain unified data flow.

Core Capabilities of SaaS Customer Onboarding Software

- Digital workflows with dynamic forms and conditional logic for KYC, suitability, and documentation collection

- Client portals for self-service uploads, progress tracking, and secure messaging

- Automation of reminders, approvals, and task routing based on predefined rules

- Analytics and reporting capabilities for bottleneck detection and onboarding metrics tracking

Why SaaS Customer Onboarding Is Especially Critical for Financial Institutions

Onboarding represents the decisive phase in any financial client relationship. It’s the moment that determines time-to-first-trade for investment accounts, time-to-first-policy for insurance products, and the foundation of client trust that will shape the entire customer journey. For regulated institutions, it’s also the gauntlet of regulatory clearance, PEP (Politically Exposed Person) screening, sanctions checks, source-of-wealth documentation, and suitability assessments that must be completed before any revenue-generating activity can begin.

Regulatory Drivers

The regulatory and business drivers are intensifying:

- AMLD5/6 (Anti-Money Laundering Directives 5 and 6): Mandate enhanced due diligence for high-risk clients. Learn more about AMLD5/6

- FINMA (Swiss Financial Market Supervisory Authority): Requires risk-based approaches and comprehensive source-of-wealth documentation for Swiss banks.

- GDPR (General Data Protection Regulation): Imposes data minimization principles and cross-border data flow restrictions.

Manual KYC checks cost banks $50-100 per client versus $5-10 when automated, a tenfold difference that compounds across thousands of client onboardings annually.

Revenue Impact

Reducing onboarding from weeks to days can boost AUM growth by 15-25% through earlier fee collection and trade execution. NPS (Net Promoter Score) scores in wealth management drop 10-20% from slow account openings, directly impacting referral rates in a business where word-of-mouth drives significant new client acquisition. Poor onboarding execution correlates with up to 40% churn in the first 90 days for fintechs, according to industry reports.

Client Expectations

Client expectations have shifted:

- HNWIs and institutional clients in 2026 expect mobile-first, self-service experiences with transparent status updates, not email attachments and in-person signature ceremonies.

- Churn costs compound over time: In wealth management relationships lasting 10-20 years, losing a client to poor onboarding means forfeiting decades of fees and referral potential.

- Cross-border complexity demands structure: Onboarding clients across jurisdictions requires segmented workflows that handle Swiss residents differently from high-risk cross-border clients with complex wealth structures.

- Onboarding effectiveness must be measured: Tracking key metrics such as time-to-value, customer activation, completion rates, and early satisfaction scores is essential to assess how well new users are integrated and retained.

The customer success team plays a crucial role in onboarding, customer engagement, and ongoing support, especially in high-touch onboarding models where personalized guidance and training are key to client success.

Transition: With a clear understanding of why SaaS customer onboarding software is critical, let’s examine how it accelerates time-to-value and revenue recognition for financial institutions.

Faster Time-to-Value and Revenue Recognition

The difference between manual and software-driven customer onboarding is measured in weeks, not hours.

Manual vs. Software-Driven Onboarding

Consider a typical private banking client onboarding under manual processes:

- PDF forms emailed for completion

- Manual PEP and sanctions checks

- Physical signatures required

- Documents re-keyed into core systems

- 15-20 business days if everything goes smoothly

With onboarding software, the same journey compresses to 2-3 days:

- Client receives a secure portal link

- Completes dynamic KYC forms with conditional logic

- Uploads documents directly

- E-signs agreements

- Receives automated approval routing

In InvestGlass, this entire flow KYC forms, risk profiling, MiFID II suitability questionnaires, investment policy statements, and digital signatures happens in a single journey. New users interact with one branded portal rather than juggling email threads and disconnected PDF attachments. The client completes each step with clear onboarding progress indicators, while compliance officers review flagged items in real-time.

Revenue Impact

The revenue impact is immediate. Earlier onboarding completion means trades execute sooner, management fees begin accruing, and AUM gets booked in the current quarter rather than slipping to the next. For a wealth manager handling dozens of new HNWI relationships each month, accelerating time to value by two weeks translates directly to earlier revenue recognition and improved cash flow.

Before and After Comparison

Manual Onboarding | Software-Driven Onboarding |

|---|---|

Email PDFs for KYC completion | Secure portal link with dynamic forms |

Manual PEP/sanctions screening | Automated screening with risk flags |

Physical signatures required | Digital e-signatures in portal |

Manual data entry to core systems | API integration pushes data automatically |

15-20 business days | 2-3 business days |

Transition: Beyond revenue acceleration, onboarding software also plays a vital role in reducing operational and compliance risk.

Lower Operational and Compliance Risk

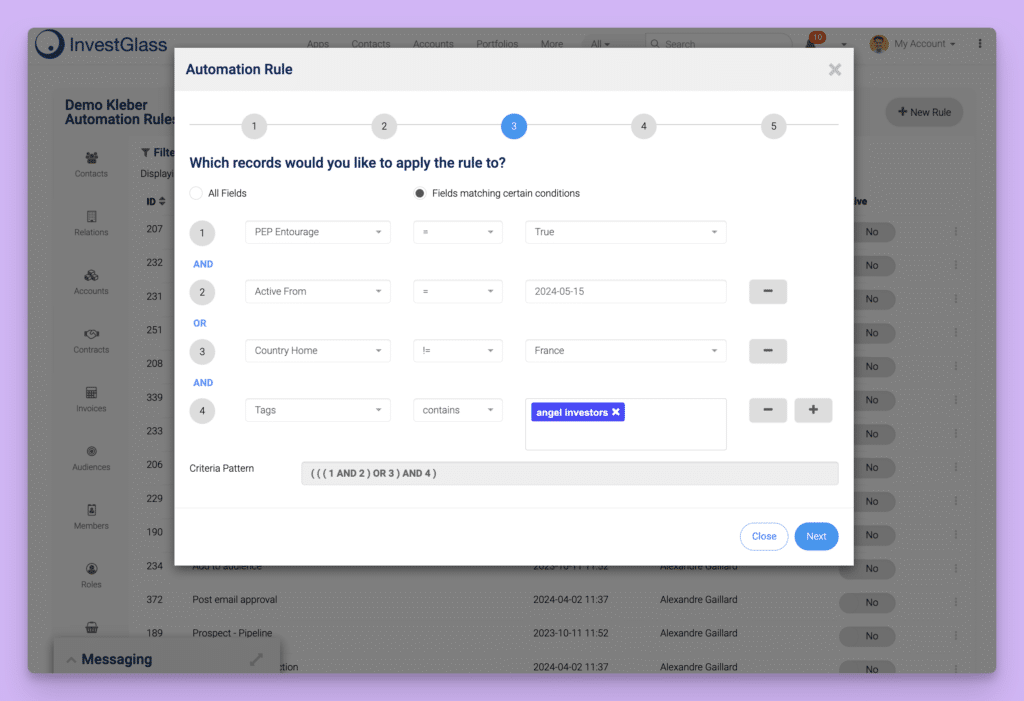

Onboarding software enforces mandatory steps that manual processes frequently miss. PEP screening, sanctions list checks, source-of-wealth documentation, UBO collection for corporate clients these steps cannot be skipped or forgotten when they’re built into automated workflows.

Compliance Automation

When certain conditions are met, such as a risk score exceeding a defined threshold or missing mandatory documents, the system automatically routes the case to compliance for review before proceeding.

InvestGlass maintains an immutable audit trail documenting who approved which step, when, and on which dataset. This audit trail proves invaluable during 2024-2026 regulatory inspections, where examiners expect to see documented evidence that compliance procedures were followed consistently. The platform logs every approval, every document upload, every form completion, creating the paper trail that FINMA, AMLD6, and other regulatory frameworks demand.

Standardization and Error Reduction

Standardized onboarding workflows also eliminate errors caused by inconsistent processes. When relationship managers each handle onboarding their own way some via email attachments, others with shared network folders, others with physical document binders errors multiply. Documents get lost, steps get skipped, and version control becomes impossible.

Critical Compliance Benefits

- Enforced mandatory steps reduce non-compliance incidents by up to 70%

- Immutable audit trails satisfy regulatory inspection requirements

- Standardized workflows eliminate version control errors and lost documentation

Transition: In addition to compliance and operational benefits, onboarding software significantly enhances the client experience and relationship building.

Improved Client Experience and Relationship Building

A modern, portal-based user onboarding experience transforms how clients perceive their new financial relationship.

Portal-Based Experience

Instead of sending unencrypted emails with sensitive documents attached, clients access a branded portal where they:

- Upload identification

- Complete questionnaires

- Track their onboarding progress through clear visual indicators

Tracking customer progress provides visibility into the customer’s journey and onboarding status, enabling proactive management and improved customer success outcomes. Secure messaging within the portal replaces scattered email threads, keeping all communication in one documented location.

Meeting Modern Client Expectations

HNWI and institutional clients in 2026 expect more:

- Mobile-first interfaces that work on any device

- Self-service checklists for task completion at their convenience

- Transparent status updates showing exactly where their onboarding stands and what’s needed next

- A sense that their time is valued, not that they’re navigating bureaucratic obstacles

InvestGlass client portals deliver this experience while maintaining Swiss data residency and bank-grade security. The platform’s no code client portals can be branded to match each institution’s identity, with multilingual support for the diverse client bases that Swiss and European banks serve. Push notifications alert clients when action is needed, reducing the back-and-forth that frustrates both clients and relationship managers.

Real-World Example

Consider a mid-size private bank in Geneva that modernized its onboarding process in 2025. Previously, HNWI onboarding averaged 18 days with multiple in-person meetings and courier-delivered documents. After implementing digital onboarding journeys, average completion dropped to 5 days with higher overall customer satisfaction scores. The bank’s relationship managers reported spending 40% less time on administrative follow-up, freeing them to focus on relationship building and investment advice.

Transition: Now that we’ve explored the impact of onboarding software, let’s review the key features to look for when selecting a solution for your institution.

Key Features to Look For in SaaS Customer Onboarding Software

Not all onboarding tools are created equal, especially for regulated businesses with complex KYC requirements, multi-party approval workflows, and stringent suitability rules. Generic project management software lacks the compliance DNA that financial institutions require.

Essential Feature Categories for Financial Onboarding

- Digital KYC workflows: Dynamic forms with conditional logic, automated risk scoring, MiFID II questionnaires, FATCA/CRS self-certification, and UBO collection for corporate clients

- Integrated CRM: Banking-grade client records with household mapping, relationship tracking, multi-currency portfolios, and regulatory classifications

- Client portals: Self-service onboarding interfaces with secure document uploads, progress tracking, e-signatures, and multilingual support

- Automation and playbooks: Standardized templates with conditional triggers, automated reminders, and approval workflows

- Learning management system integration: Deliver personalized onboarding experiences through e-learning content, including blended and mobile learning options, to enhance user engagement and tailored training

- Product analytics tool: Capture and analyze user behavior data during onboarding, focusing on critical activation events to improve engagement and reduce time to value

- Analytics and engagement tracking: Metrics on onboarding completion times, drop-off rates, bottleneck identification, and user engagement patterns

- Security and data sovereignty: Swiss or EU hosting options, on-premise deployment capabilities, encryption at rest and in transit, and granular role-based access control

- Integration capabilities: REST APIs connecting to core banking, portfolio management, document management, and e-signature providers

- AI-powered assistance: Risk scoring, form pre-filling, next-best-action suggestions, and automated document classification

Transition: With these features in mind, let’s see how InvestGlass streamlines SaaS customer onboarding for regulated industries.

How InvestGlass Streamlines SaaS Customer Onboarding for Regulated Industries

InvestGlass functions as an all-in-one Swiss SaaS platform built specifically for onboarding and lifecycle management of financial clients. Unlike generic onboarding or project tools that require extensive customization for regulated use cases, InvestGlass natively combines CRM, digital onboarding, portfolio management, marketing automation, and client portals in a single integrated platform.

Integration Across the Client Lifecycle

This integration matters because financial client onboarding isn’t an isolated event it’s the beginning of a relationship that spans products, services, and years. Data captured during onboarding must flow seamlessly into portfolio management, marketing campaigns, periodic reviews, and regulatory reporting. With InvestGlass, onboarding projects can be automated and triggered immediately after the sales process concludes, ensuring a seamless transition for new customers and continuity from sales to onboarding. When these capabilities live in separate systems, data silos emerge, manual re-keying introduces errors, and the client experience fragments.

Typical Onboarding Journey in InvestGlass

1. From Lead Capture to Qualified Prospect in the CRM

Prospects arrive through multiple channels:

- Website forms

- Referral programs

- Networking events

- Digital marketing campaigns

- Direct outreach

InvestGlass captures these prospects directly into the CRM, associating each with the source and any initial information provided. No leads fall through cracks between marketing systems and sales processes.

Marketing automation scores leads based on profile characteristics and engagement. An HNWI prospect in Zurich with expressed interest in discretionary portfolio management receives a higher score than a retail inquiry about basic savings products. Lead scoring triggers appropriate onboarding pathways high-value prospects route to senior RMs with white-glove onboarding flows, while straightforward cases proceed through more automated journeys.

All communication history, emails, calls, meeting notes, stores within the CRM record, preserving context before formal KYC begins. When a prospect converts to formal onboarding, the relationship manager has full visibility into prior interactions and expressed preferences.

Example Journey:A prospect downloads a whitepaper on sustainable investing from the firm’s website, providing contact information and indicating investable assets above CHF 1 million. Marketing automation tags this as a qualified lead, sends a nurture email sequence, and alerts the appropriate RM team. When the prospect responds expressing interest in opening an account, the RM initiates formal onboarding with full context on the prospect’s interests and background.

2. Digital Onboarding and KYC in a Single Flow

The digital onboarding journey in 2026 begins when the client receives a secure link to their personalized portal. Within the portal, they encounter a guided experience:

- Personal information collection

- Identification document upload

- Proof of address submission

- Tax residency and FATCA/CRS self-certification

- Risk profile questionnaire

- Investment suitability assessment

- Legal agreement review and e-signature

InvestGlass applies rules throughout this flow to flag items requiring compliance attention. PEP matches trigger enhanced due diligence workflows. High-risk country indicators route to senior compliance review. Incomplete or inconsistent data generates clarification requests before the case can proceed. All routing happens automatically based on configured business rules no manual triage required.

Both retail clients with straightforward profiles and complex corporate structures with multiple UBOs follow appropriate workflows. Corporate onboarding forms capture each beneficial owner, their ownership percentages, their individual KYC data, and the corporate documentation establishing the entity’s legitimacy.

This single digital process replaces what previously required multiple emails, PDF attachments, physical signatures, and manual data entry. The client completes everything in one portal; the institution receives structured data ready for compliance review and core system integration.

3. White-Glove Client Portal Experience with Swiss Hosting

The InvestGlass portal presents a branded interface matching each institution’s visual identity. Multilingual support accommodates Swiss and European client bases German, French, Italian, English, and other languages as needed. Clear progress indicators show clients exactly where they stand in the onboarding journey, what’s completed, and what actions remain.

Portal content extends beyond KYC forms. Clients access their onboarding checklist, investment proposals prepared by their advisor, model portfolio recommendations aligned with their risk profile, policy documents, regulatory disclosures, and educational content about products and services. The portal serves as a resource hub throughout the in-app onboarding experiences, not just a form collection mechanism.

Data and documents host in Switzerland, aligning with the requirements of banks and wealth managers that need Swiss data sovereignty. For clients concerned about where their sensitive financial information resides, Swiss hosting provides reassurance that their data remains subject to Swiss privacy protections.

Relationship managers and advisors manage multiple client portals using templates, ensuring consistent treatment across all relationships. A new customer receives the same professional, organized experience whether they’re the RM’s first client of the day or the twentieth.

4. Portfolio Setup, Product Activation, and Ongoing Lifecycle Management

Once onboarding completes, InvestGlass connects directly to portfolio management and product modules. For investment accounts, advisors propose portfolios aligned with the client’s documented risk profile, investment objectives, and any specific constraints or preferences captured during onboarding. Suitability and appropriateness documentation generates automatically, creating the audit trail that MiFID II requires.

For insurance products, policy activation proceeds with full fact-finding documentation already captured. For banking products, account opening triggers with KYC data already verified and ready for core system integration.

The same platform supports the ongoing lifecycle:

- Periodic KYC reviews triggered by regulatory requirements or risk-based schedules

- Portfolio performance reviews

- Cross-selling opportunities identified through product holding analysis

- Relationship health monitoring

Data captured during onboarding persists and informs every subsequent interaction.

Lifecycle Continuity Benefits

- Onboarding data reused for periodic reviews, no re-collection of unchanged information

- Investment suitability reassessments build on documented baseline

- Cross-selling recommendations consider complete product holdings and stated objectives

- Single platform reduces friction versus navigating disconnected systems for each lifecycle stage

5. Automation and AI to Reduce Manual Work

InvestGlass automation handles repetitive tasks that consume relationship manager and operations staff time:

- Automated reminders prompt clients when document uploads remain pending

- Scheduled review tasks appear in compliance officer queues at appropriate intervals

- Forms pre-fill with existing CRM data so clients confirm information rather than re-entering it

AI-powered tools extend these capabilities further:

- Client profile summarization helps RMs quickly understand new relationships

- Draft suitability notes generate based on risk questionnaire responses and stated objectives

- Next-best-action suggestions guide RMs toward appropriate follow-up based on client activity and portfolio data

This automation configures without heavy IT projects. Operations and compliance teams adapt workflows as regulations evolve, adding new fields after a FINMA circular, adjusting risk scoring thresholds, creating new document requirements without waiting for development resources or vendor professional services.

Concrete Example: A compliance officer previously spent 8-10 hours weekly reviewing periodic KYC updates and chasing outstanding documentation. With automated reminders, pre-filled forms, and risk-based routing that prioritizes high-risk cases, the same reviews now take 3-4 hours weekly, freeing half the time for higher-value compliance activities.

Transition: With a clear understanding of how InvestGlass streamlines onboarding, let’s turn to best practices for designing a SaaS customer onboarding process in financial services.

Best Practices for Designing a SaaS Customer Onboarding Process in Financial Services

Software alone doesn’t guarantee successful onboarding. Banks and wealth managers need defined, compliant onboarding playbooks that translate platform capabilities into consistent execution. Choosing the right onboarding tools is essential for efficient and effective onboarding processes, ensuring seamless integration and improved user experience.

Action-Oriented Best Practices

- Map risk-based journeys segmented by client type, jurisdiction, and product complexity

- Minimize friction while ensuring complete KYC data capture through progressive disclosure and smart defaults

- Standardize templates for documents and questionnaires while allowing advisor personalization in appropriate sections

- Integrate onboarding software with core banking and portfolio management systems to eliminate re-keying

- Leverage the right onboarding tools and expertise to help users onboard at scale, maximizing product adoption and ensuring a smooth transition for large numbers of users

- Define SLAs for each onboarding phase and track compliance through dashboards

- Involve compliance early in journey design, not as a final review gate

- Measure continuously and refine workflows quarterly based on analytics data

Map Risk-Based Journeys and Segment by Client Type

Onboarding flows should differ substantially based on client characteristics. A retail client opening a simple savings account requires different steps than an HNWI establishing a discretionary portfolio mandate, which differs again from a corporate client with complex UBO structures or an institutional investor with specific reporting requirements.

InvestGlass enables teams to build different templates and checklists for each segment:

- Low-risk Swiss residents proceed through streamlined flows with basic KYC, standard risk questionnaires, and expedited approvals.

- High-risk cross-border clients with complex wealth structures, perhaps involving multiple jurisdictions, politically exposed persons connections, or unusual source-of-wealth scenarios, follow enhanced due diligence paths with additional documentation requirements and senior compliance review.

Practical Difference: A low-risk Swiss resident with straightforward employment income might complete onboarding in 2-3 days through a largely automated flow. A high-risk cross-border client with wealth derived from business interests across multiple jurisdictions might require 2-3 weeks with extensive documentation, multiple compliance reviews, and potentially external verification services.

Minimize Friction While Gathering Complete KYC Data

Balancing regulatory thoroughness with streamlined user onboarding experience requires deliberate design:

- Progressive disclosure shows only relevant fields, personal information first, then tax residency details, then risk questionnaire, rather than overwhelming clients with massive forms upfront.

- Draft saving allows clients to pause and resume without losing progress.

- Mobile-friendly forms accommodate clients who prefer completing onboarding from phones or tablets.

InvestGlass supports pre-filling client data from existing CRM records. If a prospect provided information during marketing interactions or if the client has prior relationships with the institution, that data populates into onboarding forms for confirmation rather than re-entry. This reduces abandonment, increases completion rates, and minimizes support calls from frustrated clients.

Visual elements reinforce progress and reduce perceived burden:

- Progress bars show completion percentage

- Step indicators clarify what’s next

- Estimated completion times set appropriate expectations

These UX improvements translate to tangible metrics: higher form completion rates, lower drop-off at challenging steps, and reduced time spent on client support.

Standardize Templates but Allow Advisor Personalization

Institutions need bank-wide templates for documents, questionnaires, and approval workflows. Without standardization, each relationship manager invents their own process, creating compliance risk and inconsistent client experiences. Templates ensure that mandatory regulatory content appears consistently, approval sequences follow defined protocols, and documentation meets institutional standards.

At the same time, high-touch onboarding requires human personalization. InvestGlass templates can lock mandatory sections legal disclosures, regulatory questionnaires, compliance acknowledgments while leaving sections open for advisor notes, personalized recommendations, or custom commentary. The investment policy statement might include standard risk language alongside advisor-specific notes on the client’s expressed preferences and concerns discussed during initial meetings.

This balance reduces internal negotiation about process while preserving the human touch that distinguishes premium financial services. RMs don’t argue about whether certain steps are required the template enforces them. But they retain flexibility to demonstrate understanding of each client’s unique situation.

Integrate Onboarding with Existing Core Systems

Connecting onboarding software to core banking, portfolio management, and document management systems eliminates the re-keying that introduces errors and delays. When onboarding completes in InvestGlass, approved client data should flow automatically to the core system for account opening. Completed documents should archive to the institution’s document management system. Portfolio instructions should transmit to trading and custody systems.

InvestGlass offers REST APIs and connectors for these integration scenarios. For on-premise deployments, direct integration with legacy systems becomes possible within the institution’s own infrastructure. Practical integration points include:

- Client master data synchronization

- Account and product records

- Securities and portfolio positions

- Document archival and retrieval

- E-signature provider connections

Implementation Timeline Example:

Phase | Duration | Scope |

|---|---|---|

Phase 1: MVP | 8-12 weeks | Digital onboarding forms, client portal, basic workflows |

Phase 2: Integration | 3-6 months | Core banking connection, document management, e-signature |

Phase 3: Expansion | 3-6 months | Additional segments, regions, CRM, portfolio modules |

Measure and Continuously Improve Onboarding

Tracking concrete KPIs enables continuous improvement:

- Average onboarding duration benchmarks performance over time

- Number of back-and-forth interactions per client reveals process friction

- KYC rejection rate indicates form clarity and client communication effectiveness

- First-year churn among recently onboarded clients signals whether the onboarding experience sets relationships up for success

InvestGlass dashboards let managers compare teams, branches, or regions to identify best performers and bottlenecks. If one team consistently completes onboarding faster with fewer client escalations, their practices can inform training for other teams. If a particular form shows high drop-off rates across all teams, the form itself likely needs redesign.

Quarterly reviews bringing together operations, compliance, and front-office stakeholders create forums for refining workflows based on data. What worked well? Where did clients struggle? What regulatory changes require workflow updates? These collaborative reviews ensure that onboarding processes evolve rather than stagnating.

Transition: With these best practices in mind, let’s explore how to select the right onboarding software for your institution.

How to Choose SaaS Customer Onboarding Software for Your Bank or Wealth Firm

Selecting an onboarding platform in 2024-2026 requires balancing regulatory, technical, and business criteria. Generic SaaS tools may not satisfy Swiss or EU regulatory requirements, complex financial instrument workflows, or the security standards that bank IT and compliance teams demand. The evaluation process should involve compliance, IT, operations, and front-office stakeholders to ensure all perspectives inform the decision.

Key Evaluation Dimensions

- Regulatory fit: Does the platform support FINMA, GDPR, AMLD5/6, and MiFID II requirements out of the box?

- Data residency: Can data be hosted in Switzerland, the EU, or on-premise as required?

- Configurability: Can operations teams adapt workflows without developer resources or vendor professional services?

- Usability: Is the interface intuitive for RMs, compliance officers, and end-clients?

- Client experience: Do portals meet the expectations of HNWIs and institutional clients?

- Integration: Does the platform connect to existing core banking, portfolio management, and document systems?

- Total cost of ownership: What are realistic costs for licenses, implementation, and ongoing support?

InvestGlass represents a strong option for institutions prioritizing Swiss sovereignty, integrated CRM, and wealth-specific workflows. The platform’s all-in-one approach, combining onboarding, CRM, portfolio management, and marketing automation, reduces vendor proliferation and integration complexity.

Regulatory and Data Residency Requirements

Validating that onboarding software can be hosted in Switzerland or the EU, and supports on-premise deployments where required by regulators, should be an early evaluation step. Generic US-based SaaS platforms may store data in multi-tenant environments across various jurisdictions, creating complications for institutions subject to Swiss banking secrecy or GDPR data localization requirements.

Vendor Selection Checklist for CIO/CISO

Requirement | Questions to Ask |

|---|---|

Data location | Where are data centers located? Can we specify Switzerland/EU only? |

Subprocessors | Which third parties access data? Where are they located? |

Encryption | What encryption standards apply at rest and in transit? |

Incident response | What are notification timelines and procedures for security incidents? |

Audit rights | Can we audit the platform or receive audit reports (SOC 2, ISO 27001)? |

On-premise option | Can the platform be deployed within our own infrastructure? |

Configurability Without Heavy IT Projects

Financial institutions need no-code or low-code configuration capabilities so operations teams can adapt onboarding as regulations evolve in 2025-2026. When a new FINMA circular requires additional disclosure language or modified risk assessment criteria, the institution shouldn’t wait months for vendor development or internal IT projects.

InvestGlass allows non-technical users to build forms, workflows, and templates directly in the user interface. Adding a new field to a KYC form, creating a conditional logic rule, or modifying an approval workflow happens in a few clicks rather than requiring code changes. This configurability empowers operations and compliance teams to own their processes without dependency on technical resources.

Tangible Example: A FINMA circular published in October requires updated suitability assessment questions by January. With InvestGlass, the compliance team updates the relevant form within days, tests with a pilot group, and deploys to production before the deadline. With a code-dependent platform, the same change might take 6-8 weeks of development, testing, and deployment, potentially missing the deadline entirely.

User Experience for Both Internal Teams and Clients

Relationship managers, compliance officers, operations staff, and end-clients all interact with onboarding software. Each group has different needs and different tolerance for complexity. RMs need efficient workflows that don’t pull them away from client relationship activities. Compliance officers need clear visibility into flagged cases and audit trails. Operations staff need task management capabilities that organize their queues. Clients need intuitive self-service interfaces that don’t require training.

Multilingual interfaces matter particularly for Swiss and European banks serving diverse client bases. InvestGlass supports German, French, Italian, English, and other languages, allowing each user to work in their preferred language while sharing the same underlying data and workflows.

Concrete UX Story: A mid-size Swiss bank previously required two weeks of training before new RMs could handle onboarding independently. Complex legacy systems with multiple screens and manual handoffs created confusion and errors. After implementing InvestGlass, new RM training dropped to three days, with most learning happening through guided use of intuitive interfaces. Error rates decreased, client satisfaction increased, and RM time spent on administrative tasks dropped significantly.

Total Cost of Ownership and Implementation Timeline

Understanding the main cost components licenses, implementation, integrations, and ongoing configuration support enables realistic budgeting. License costs vary based on user counts and modules selected. Implementation costs depend on workflow complexity, integration requirements, and customization needs. Integration costs reflect the technical effort to connect with existing core systems. Ongoing costs include support, maintenance, and periodic configuration updates as requirements evolve.

Realistic Implementation Ranges:

- 8-12 weeks for a focused digital onboarding MVP covering forms, workflows, and portal without deep core system integration

- 3-9 months for broader CRM and portfolio management integrations, depending on scope and regional complexity

InvestGlass can start with a digital onboarding pilot perhaps one country or business line before expanding to full CRM and portfolio management deployment. This phased approach reduces initial investment risk, allows teams to build expertise, and generates early wins that build organizational support for broader rollout.

User Behavior Analysis in Financial Onboarding

Understanding user behavior is fundamental to optimizing the onboarding process in regulated financial institutions. By leveraging onboarding software equipped with robust analytics and reporting capabilities, banks and wealth managers can gain deep insights into how new users interact with onboarding flows, which steps drive engagement, and where friction points arise.

Key Features of User Behavior Analysis

- Track every user interaction within the onboarding journey, such as form completions, document uploads, and time spent on each step

- Monitor user engagement with educational content and onboarding resources

- Collect and analyze user feedback through in-app surveys or direct portal input

With these analytics, onboarding teams can segment users based on behavior, tailor onboarding resources to specific needs, and proactively address drop-off points. For example, if reporting capabilities reveal that a significant percentage of users abandon the process at a particular form, the onboarding team can redesign that step for clarity and ease of use. This data-driven approach ensures that the onboarding process is not only compliant but also user-centric, driving higher completion rates and overall customer satisfaction.

Product Adoption Strategy for Financial Institutions

A well-defined product adoption strategy is essential for ensuring that customers not only complete the onboarding process but also fully embrace the financial products and services offered. Successful product adoption begins with a deep understanding of each customer’s unique needs, goals, and expectations. Onboarding software plays a pivotal role by enabling personalized onboarding experiences that align with these needs from the very first interaction.

Key Features of an Effective Product Adoption Strategy

- Map the customer journey and design onboarding flows that guide users through key product features

- Provide ongoing support to encourage continued engagement

- Automate onboarding workflows and deliver targeted onboarding resources

- Track onboarding progress to ensure that no customer is left behind

Ongoing engagement is critical customer onboarding doesn’t end with account activation. Regular check-ins, educational content, and proactive support help customers realize the full value of their investment, driving higher product adoption rates and long-term loyalty. By integrating these elements into the onboarding process, financial institutions can accelerate time to value, reduce churn, and maximize the impact of their product offerings.

Onboarding Team and Resources: Building a High-Performing Onboarding Function

A high-performing onboarding function is built on the foundation of a dedicated team and the right resources. At the core is the customer success manager, who orchestrates the entire onboarding process and ensures that each new customer receives a seamless, personalized experience. Supporting roles, such as technical specialists and training personnel, provide expertise and guidance at every stage of the onboarding journey.

Key Resources for Onboarding Teams

- Advanced onboarding software with automated workflows and task management tools

- Clear communication channels within the team and with customers

- Training materials and support documentation

By equipping onboarding teams with the right tools and resources, financial institutions can ensure that every new customer receives the attention and support needed for a successful onboarding experience. This collaborative approach not only improves operational efficiency but also drives customer success and satisfaction throughout the entire customer lifecycle.

Customer Communication and Support During Onboarding

Effective customer communication and support are at the heart of a successful onboarding process. Financial institutions must provide clear, concise information and responsive support to guide customers through each step of the onboarding journey. Onboarding software enhances this experience by offering a suite of communication tools, including in-app messaging, email support, and real-time notifications.

Key Features of Customer Communication and Support

- Personalized communication tailored to each customer’s specific needs and onboarding stage

- Timely guidance, answers to questions, and issue resolution as they arise

- Ongoing support beyond onboarding completion, with easy access to help resources

By maintaining open lines of communication and providing easy access to help resources, financial institutions can foster long-term customer engagement and satisfaction. This proactive approach not only reduces onboarding friction but also lays the groundwork for lasting customer relationships and continued success.

Frequently Asked Questions About SaaS Customer Onboarding Software

These questions reflect common inquiries InvestGlass receives from banks, wealth managers, and regulated institutions evaluating onboarding solutions between 2024-2026. Each answer addresses the specific context of financial services rather than generic software considerations.

What is the difference between SaaS customer onboarding and digital KYC?

Digital KYC represents one component of the broader onboarding journey, focused specifically on identity verification and regulatory checks. KYC confirms who the client is, assesses risk factors, and satisfies regulatory requirements for client identification. Onboarding encompasses the entire journey from contract signature to first value, including KYC, but also extending to product setup, portfolio opening, documentation completion, and relationship establishment.

InvestGlass combines KYC with CRM, workflows, and client portal capabilities to handle the entire onboarding process rather than just identity verification. A client might pass KYC verification, then immediately receive investment proposals, complete suitability documentation, review and sign agreements, and access their new portfolio, all within the same platform and portal experience. Separating these functions across different systems creates handoff delays and fragmented experiences.

Can SaaS onboarding software support both high-touch and self-serve models?

Banks and wealth managers often need both approaches. HNWI clients and complex corporate relationships warrant high-touch onboarding with significant RM involvement, guided portal sessions, and personalized attention. Mass affluent or retail clients may prefer, and the institution may require for efficiency, more self-serve flows with automated guidance and minimal RM intervention.

InvestGlass supports both models within the same platform. RMs can guide users through portal sessions in real-time, providing assistance and answering questions as clients complete forms. Other clients complete steps independently, with automated reminders prompting action and escalating to RMs only when needed. Practical controls like conditional content visibility, hideable sections, and advisor review steps before final approval allow flexible configuration for different client segments.

This flexibility contrasts with pure self-serve SaaS onboarding tools common in non-regulated industries, which assume minimal human involvement throughout the journey.

How does InvestGlass integrate with existing banking or insurance systems?

InvestGlass offers REST APIs enabling connection to core banking systems, portfolio management platforms, document management systems, and e-signature providers. Data flows bidirectionally: client information captured during onboarding pushes to core systems for account opening; portfolio positions sync back to client records for unified relationship views.

For on-premise deployments, InvestGlass installs within the institution’s own infrastructure, enabling direct integration with existing data sources that may not be accessible from external cloud platforms. This deployment model suits institutions with strict network segregation requirements or legacy systems that cannot expose APIs externally.

Concrete integration examples include:

- Pushing KYC-approved client master data to the core banking system to trigger account creation

- Syncing portfolio positions nightly from custody systems to display in client portals

- Archiving signed documents to the institution’s document management system with appropriate metadata

- Connecting to e-signature providers for legally binding digital signatures

How long does it take to implement InvestGlass for onboarding?

Implementation timelines depend on scope, complexity, and internal resources. A focused digital onboarding MVP forms, workflows, and portal without deep integration typically deploys in 8-12 weeks. This phase establishes the platform, configures initial workflows, trains key users, and begins handling real client onboardings.

Broader deployments including CRM integration, portfolio management connections, and multi-region rollout extend to 3-9 months depending on the number of systems involved, data migration requirements, and regulatory approval processes.

Many institutions start with one market segment, for example, Swiss onshore private clients, and demonstrate success before expanding to cross-border segments or institutional client types. This phased approach manages risk, builds internal expertise, and generates measurable results that support continued investment.

Do clients need an account to access InvestGlass onboarding portals?

External clients access their onboarding portal via secure links with multi-factor authentication, without needing full internal InvestGlass accounts. This approach simplifies client access no registration process, no additional credentials to remember, no account management overhead.

Only internal users relationship managers, compliance officers, operations staff require InvestGlass user accounts. This separation reduces client friction while maintaining appropriate access controls for internal functions.

The practical difference matters for user adoption. Requiring clients to create accounts, verify email addresses, set passwords, and remember credentials adds friction that increases abandonment rates. Secure link access with MFA authentication achieves security objectives without the overhead.

How does SaaS onboarding software help reduce churn in wealth management and banking?

Early interactions during onboarding set the tone for relationships that may last decades. Clients who experience slow, confusing, or error-prone onboarding begin their relationship frustrated a poor foundation for long-term retention. Clients who experience fast, transparent, professional onboarding begin with confidence in their institution’s competence.

InvestGlass enables proactive communication, clear timelines, and fewer errors during onboarding, directly addressing the friction that creates early dissatisfaction. Transparent progress tracking shows clients that things are moving forward. Automated reminders reduce the feeling of being forgotten. Professional portal experiences demonstrate institutional sophistication.

Beyond the onboarding period, data captured during onboarding feeds into personalization, cross-selling, and periodic review processes. Understanding client preferences, risk tolerance, and stated objectives from day one enables more relevant ongoing service. Institutions using structured onboarding software report first-year churn reductions of 5-10%, meaningful improvements in a business where client relationships drive long-term value.

Getting Started with InvestGlass for SaaS Customer Onboarding

The market and regulatory pressures facing regulated financial institutions in 2024-2026 make onboarding modernization urgent rather than optional. AMLD6 enhanced due diligence requirements, FINMA’s continued focus on client identification practices, and rising client expectations for digital experiences all point toward the same conclusion: manual, paper-based onboarding processes cannot scale and cannot compete.

InvestGlass offers regulated institutions a clear path forward. As a Swiss sovereign platform combining CRM, digital onboarding & KYC, portfolio management, marketing automation, and client portals, InvestGlass addresses the full spectrum of needs without requiring integration between disconnected systems. Swiss data sovereignty satisfies the residency requirements that European financial institutions face. No-code configuration empowers operations and compliance teams to adapt workflows as requirements evolve.

The practical next step: a discovery call to understand your institution’s current onboarding challenges, followed by a demo focused specifically on onboarding workflows relevant to your client segments. From there, a pilot configuration for one segment perhaps HNWI clients in Switzerland or a specific product line demonstrates value within 8-12 weeks before broader rollout. Involving compliance, IT, and front-office stakeholders from the beginning ensures that the resulting solution addresses all requirements and builds organization-wide support.

Schedule a demo or workshop to map your current client onboarding process into an InvestGlass-powered workflow. The institutions that modernize onboarding now will capture faster revenue recognition, lower compliance risk, and stronger client relationships, while competitors continue struggling with email attachments and spreadsheet tracking.

Related articles

Swiss Sovereign CRM: Built on AI.

Ready to act.