Digital transformation in banking has moved far beyond simple online forms and mobile apps. In 2025 and beyond, it represents a fundamental shift in how financial institutions design products, interact with customers, and manage compliance across retail, private, corporate, and investment banking segments. Digital transformation is also reshaping financial organizations by improving operational efficiency, enhancing customer experience, and supporting regulatory compliance.

This transformation is both technological and cultural. It reshapes everyday customer journeys across mobile, web, branch, and open banking APIs while demanding new operational approaches, updated business models, and continuous regulatory adaptation. The digital transformation journey is a comprehensive process that involves adopting new technologies, driving organisational change, and aligning business goals with digital innovation. European banks face specific pressures including the rise of mobile-only customers, PSD2 open banking requirements, and instant payments across the SEPA zone.

For institutions seeking a sovereign alternative, InvestGlass provides Swiss-hosted CRM, digital onboarding, portfolio management, and compliance tools without dependence on American or Chinese infrastructure.

Building a strong business case is essential to justify digital transformation initiatives and secure stakeholder support, ensuring that the benefits, costs, and strategic value are clearly communicated.

Key benefits of digital transformation in banking:

- Improved customer convenience through faster service delivery

- Enhanced security via modern authentication and fraud detection

- Personalised services powered by data analytics and AI

- Cost efficiency achieved through automated processes

What Is Digital Transformation in Banking?

Digital transformation in banking is the strategic use of digital technologies to fundamentally redesign banking products, processes, and customer interactions, with a particular emphasis on rethinking and modernising core processes to improve customer experience and enable technological upgrades rather than simply digitising existing paper-based forms.

Modern transformation programmes typically span three to five years, covering core banking systems, digital channels, data infrastructure, and risk management. The transformation process is guided by a structured roadmap that outlines the steps for implementing technological and organisational change across the institution. This affects all banking segments from retail to wealth management and corporate banking. Banking financial institutions of all types are impacted by digital transformation, requiring change management, enhanced data analytics capabilities, and strategic alignment to succeed in an evolving financial landscape.

Typical components include:

- Mobile apps and online banking platforms as primary customer interfaces

- Digital onboarding with e-signatures and identity verification

- Straight-through processing reducing manual intervention

- Data-driven decision-making using analytics and AI

- Cloud computing or sovereign hosting for flexible infrastructure

- API layers enabling integration and open banking partnerships

Key Factors Driving the Digital Shift in Banking

Several forces are accelerating banking digital transformation across the financial services sector.

Customer expectations have fundamentally changed. Waiting days for loan decisions or visiting branches to open accounts is no longer acceptable. Digital banks launched in the 2010s and 2020s established new benchmarks for onboarding speed and app usability that traditional banks must now match.

Primary drivers include:

- Regulatory change including PSD2, open banking, and tightened KYC and AML requirements after 2016

- Competitive pressure from fintechs and neobanks setting new customer experience standards. In response, banks are closely monitoring emerging market trends and adopting technologies driving digital transformation, such as advanced analytics, artificial intelligence, and automation, to remain competitive and agile.

- Cost-income ratio pressures demanding operational efficiency through automation

- Executive prioritisation with many banks appointing Chief Digital Officers and allocating dedicated transformation budgets

- Operational resilience requirements following COVID-19

- Data sovereignty concerns driving European and Middle Eastern institutions toward non-American and non-Chinese vendors

Customer Centric Approach

Modern digital banking strategies begin from detailed customer journeys rather than internal systems. Banks map complete experiences across onboarding, mortgage approval, investment advice, and service recovery to identify friction points. Digital transformation in banking aims to enhance the customer journey at every touchpoint, aligning data, technologies, and strategic planning to meet evolving customer expectations.

Financial institutions now use customer data from mobile apps, transactions, and CRM interactions to personalise offers, alerts, and recommendations in real time.

Customer centric practices include:

- AI-powered virtual assistants handling routine enquiries

- Proactive alerts for upcoming payments and unusual transactions

- Personalised goal-based savings and investment plans

- Single client views enabling relationship managers to orchestrate personalised interactions

- Omnichannel experiences integrating mobile, web, branch, and partner channels, with a focus on delivering a consistent user experience across all banking channels to ensure seamless and reliable customer interactions

InvestGlass CRM helps advisers see unified client views and manage personalised engagement across email, portal, and in-person meetings.

Enhanced Infrastructure and Modern Core

Many banks still operate core banking systems built in the 1980s and 1990s. These legacy systems, often referred to as legacy infrastructure, can significantly hinder digital transformation efforts by making it difficult to integrate new technologies and processes. Addressing the challenges posed by legacy infrastructure is essential for banks aiming to remain competitive and innovative.

Complete replacement carries unacceptable risk, so successful banks adopt incremental modernisation patterns.

Infrastructure modernisation approaches:

- API layers encapsulating legacy core functionality

- Microservices architectures for new products running alongside existing systems

- Cloud or sovereign private cloud environments for analytics and channels

- Real-time data integration ensuring balances and compliance statuses synchronise instantly

- Modular platforms providing flexibility without vendor lock-in

InvestGlass can integrate on top of existing core systems to deliver modern CRM, onboarding, and portfolio management without risky big-bang replacement.

Advanced Data Analytics and AI

Banks are building unified data platforms that consolidate transaction data, onboarding data, risk data, and interaction history into governed data lakes. These platforms enable banks to extract valuable insights from large datasets, driving better risk assessment, personalisation, and compliance management.

By 2025, AI and machine learning power numerous banking functions with proper governance frameworks ensuring explainability for regulated decisions.

Key AI use cases:

- Next best offer recommendations guiding customers toward suitable products

- Risk scoring and credit decisioning replacing rule-based systems

- Churn prediction identifying at-risk customers for retention campaigns

- Portfolio risk alerts and ESG screening for wealth managers

- Generative AI drafting client communications with human oversight

- Document processing automating classification and data extraction

InvestGlass embeds AI for workflow automation and client insights while keeping data hosted in Switzerland or on premise for sovereignty.

Security First and Compliance by Design

Digital banking significantly expands the attack surface compared to traditional branch-based models. This shift introduces new security concerns, as online banking and digital services create additional vulnerabilities that must be addressed to protect customer information and maintain trust.

Security and compliance essentials:

- AI-driven anomaly detection identifying fraud and money laundering patterns faster than rule-based systems

- Multi-factor authentication as standard for all digital interfaces

- Zero trust architectures assuming no user or device is inherently trustworthy

- Implementation of robust cybersecurity measures to protect customer data and banking infrastructure

- Adherence to data privacy regulations to ensure customer data is handled in compliance with legal standards

- Identification and management of compliance risks during digital transformation to mitigate regulatory penalties and reputational damage

- Protection of sensitive data from breaches and unauthorized access through strict security protocols and staff training

- Securing access to accounts with advanced authentication and fraud detection systems to prevent unauthorised entry

- Compliance with GDPR, Swiss data protection law, KYC, and AML requirements

- Embedded compliance workflows capturing decision rationale and approval chains

- Audit-ready records for regulatory examinations

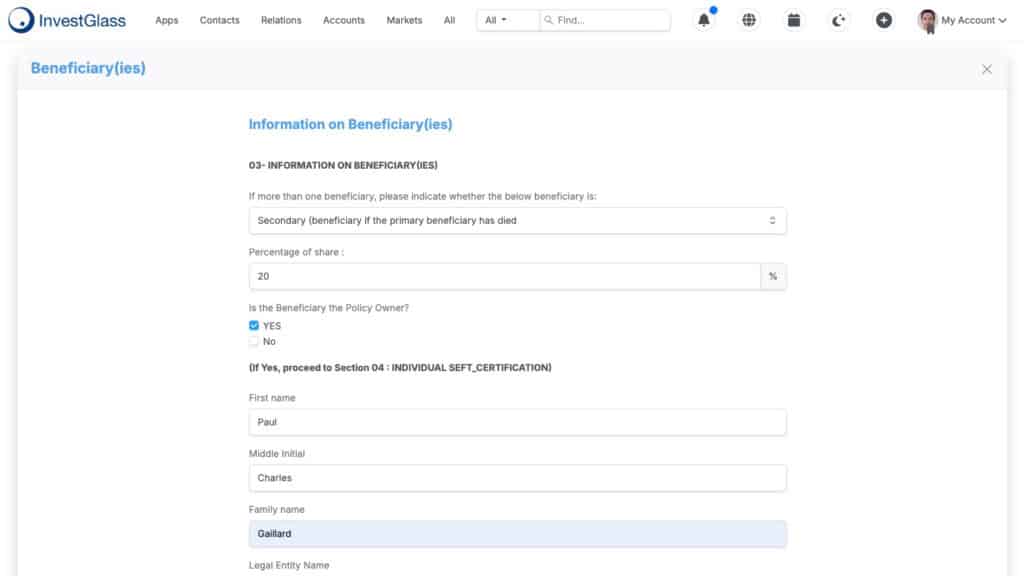

InvestGlass embeds KYC checks and approval chains directly into CRM and onboarding processes, providing audit-ready documentation.

Key Technologies Enabling Digital Transformation in Banking

Digital transformation relies on integration of complementary technologies. Banks are implementing digital solutions and new digital tools such as mobile apps and digital wallets to enhance customer experience and modernise services. Technology choices reflect regulatory constraints, latency requirements, and strategic preferences around data sovereignty.

Core technology pillars:

- Mobile platforms as primary customer interfaces

- Cloud computing providing scalable infrastructure

- Artificial intelligence enabling intelligent automation

- APIs enabling open banking and partner integration

- Blockchain for specific settlement and tokenisation use cases

Banks increasingly seek vendors offering sovereign or on-premise environments rather than exclusive reliance on American hyperscalers or Chinese ecosystems.

Cloud Computing and Sovereign Hosting

Most sophisticated financial institutions employ hybrid approaches combining public cloud, private cloud, and on-premise environments rather than single-cloud strategies.

Cloud architecture considerations:

- Elastic scaling critical for digital channels experiencing variable demand

- Faster experimentation through shorter provisioning cycles

- Improved disaster recovery through geographic redundancy

- Data residency requirements mandating that personal financial data remain within specific borders

- Protection from extraterritorial access by foreign government authorities

InvestGlass provides Swiss hosting and full on-premise deployment options, helping banks avoid dependence on American or Chinese cloud services while benefiting from modern architecture.

Artificial Intelligence and Machine Learning in Banking

AI and machine learning have transformed credit decisioning, customer service, and wealth management operations.

Concrete AI applications:

- Underwriting automation incorporating hundreds of variables for accurate credit decisions

- Conversational chatbots handling routine customer enquiries

- Robo-advisory systems suggesting asset allocations matching customer risk profiles

- Document classification accelerating onboarding by extracting key information automatically

- Generative AI creating draft portfolio summaries and internal reports

Ethical AI governance requires clear documentation of how models make decisions, regular testing for bias, and human oversight for sensitive decisions like lending and suitability assessments.

APIs, Open Banking, and Integration

PSD2 in the European Union and UK Open Banking Standards mandate that banks share customer data with licensed third parties through standardised APIs.

API strategy elements:

- Account aggregation enabling fintech apps to consolidate customer financial accounts

- Embedded finance allowing retailers to offer financial services through bank APIs

- Internal API architecture decoupling front-end channels from core systems

- OAuth and similar frameworks controlling third-party data access

- Rate limiting and encryption protecting data flowing through APIs

InvestGlass exposes and consumes APIs so that CRM, onboarding, and portfolio modules integrate with core banking, market data providers, and external KYC sources.

Blockchain and Distributed Ledger Technology

Banks experiment with blockchain for specific use cases where distributed ledgers offer clear advantages over traditional approaches.

Realistic blockchain applications:

- Cross-border payments potentially eliminating correspondent bank intermediaries

- Tokenised bonds and securities enabling faster settlement in European pilot projects

- Trade finance documentation reducing fraud in international trade

- Central bank digital currencies under development incorporating distributed ledger technology

Regulated institutions favour permissioned blockchains supporting privacy, regulatory compliance, and governance requirements.

Internet of Things and New Payment Interfaces

Wearables and connected devices enable contactless payments and authentication in several European and Asian markets.

IoT banking applications:

- Smartwatch payments for public transport and retail purchases

- In-car payment systems for fuel, tolls, and parking

- Connected POS terminals gathering transaction data for analytics

- Biometric authentication via fingerprint or face recognition on wearable devices

These channels rely on core digital banking infrastructure including tokenisation, strong customer authentication, and risk engines.

Examples of Digital Transformation in Banking

Many banks across Europe, the Middle East, and Asia have launched concrete digital programmes with measurable outcomes. These digital transformation initiatives are part of a broader transformation process that requires evaluating and improving existing processes to successfully integrate emerging technologies and modernise banking operations.

Transformation examples by segment:

- Regional retail banks reducing account opening from 10 days to 24 hours

- Private banks digitising investment proposals and risk profiling questionnaires

- Unified mobile and web platforms with digital signatures

- Integrated client portals for wealth and corporate clients

- Automated suitability checks embedded in advisory workflows

Retail Banking Transformation

Mobile-first retail banks now provide instant account opening, digital debit cards, and personalised savings goals. Mobile banking plays a crucial role in enhancing customer experience by offering real-time access to banking services and seamless interactions across digital channels.

Retail digital capabilities:

- Self-service features including card freezing and limit management

- Dispute handling directly within mobile apps

- Branch redesign focusing on advice rather than transactions

- Fully digital journeys replacing paper forms entirely

Wealth Management and Private Banking Transformation

Wealth managers digitise onboarding and risk profiling to comply with MiFID II while keeping human advisers central to the relationship.

Wealth management digital features:

- Secure client portals with portfolio views and performance reports

- Digital investment proposal generation

- Automated suitability checks and compliance documentation

- Secure messaging between clients and advisers

InvestGlass was specifically built for wealth and private banking workflows, combining CRM, portfolio management, and compliance in a sovereign Swiss environment.

Corporate and Investment Banking Transformation

Corporate banking portals centralise cash management, trade finance, and FX services for business clients.

Corporate digital capabilities:

- Analytics identifying client opportunities and informing deal execution

- Advanced analytics and machine learning to predict market trends and improve decision-making

- Digital document rooms for multi-stakeholder approvals

- e-KYC for large corporates

- Workflow tools tracking complex transaction approvals

Challenges in Banking Digital Transformation and How to Address Them

Successful digital transformation requires addressing several key obstacles beyond technology implementation.

Primary challenges:

- Legacy systems limiting agility and increasing integration complexity

- Regulatory complexity across GDPR, KYC, AML, and local requirements

- Cybersecurity threats expanding with digital channels

- Cultural resistance and skills gaps across the organisation. Engaging human resources and applying change management models such as ADKAR are essential to address resistance and ensure employees adopt new technologies effectively.

- Change management requiring alignment between business, IT, risk, and compliance. Digital transformation also supports broader strategic initiatives, enabling banks to drive operational efficiency and focus on long-term organisational goals.

Legacy Systems and Technical Debt

Core banking platforms built decades ago constrain modernisation and create operational risk.

Addressing legacy complexity:

- Progressive modernisation rather than risky big-bang replacement

- Wrapping cores with API layers enabling new capabilities

- Adopting modular front-office platforms like InvestGlass

- Realistic timelines and phased migrations with strong testing

Regulation, Data Privacy, and Sovereignty

Regulatory regimes vary by geography but share common expectations around data protection and residency.

Regulatory considerations:

- GDPR requirements around personal data processing and incident reporting

- Swiss data protection law for institutions operating in Switzerland

- KYC and AML mandates across virtually all jurisdictions

- Data residency requirements specifying where certain data must remain

Choosing a sovereign platform hosted in Switzerland or on premise helps banks protect client data sovereignty and avoid extraterritorial access risks.

Cybersecurity and Operational Resilience

Cyber attacks on financial institutions have escalated substantially, including phishing, credential stuffing, and ransomware incidents.

Security best practices:

- Multi-factor authentication and strong encryption

- Zero trust architectures with granular access control

- Continuous monitoring using AI-driven tools

- Regular penetration testing and incident response planning

Cultural Change and Skills Gap

Digital transformation affects roles across branches, operations, IT, compliance, and relationship management.

Change management approaches:

- Training in data literacy, digital tools, and agile methods

- Internal academies and digital champions programmes

- Co-creation with front-line staff to design better digital journeys

- Clear communication about transformation goals and timelines

How Banks Can Build a Successful Digital Transformation Strategy

Building a successful digital transformation strategy requires structured planning from vision through execution. A well-executed strategy not only drives operational efficiency but also provides a competitive advantage and opens up new revenue streams for banks by enabling innovative service offerings and business models.

Strategy framework steps:

- Define clear vision and measurable outcomes

- Assess current capabilities and identify gaps

- Prioritise initiatives balancing quick wins with foundational work

- Select technology partners understanding financial regulation and data sovereignty

- Implement with agile delivery and continuous improvement

Define Vision, Outcomes, and Metrics

Set a clear three to five year digital vision linked to measurable business outcomes.

Vision setting guidance:

- Target specific improvements such as reducing cost-income ratio or cutting onboarding time

- Link initiatives to KPIs including digital adoption rate and straight-through processing rate

- Ensure metrics connect explicitly to business strategy

Assess Current Capabilities and Gaps

Perform detailed assessment of current systems, processes, data quality, and organisational capabilities.

Assessment focus areas:

- Map core customer journeys end to end identifying manual steps and bottlenecks

- Cover client-facing, middle-office, and back-office functions

- Include IT infrastructure and data quality evaluation

Prioritise Initiatives and Build a Roadmap

Start with high-impact, achievable use cases that build momentum for longer-term projects.

Roadmap development:

- Sequence quick wins and foundational work over six to twelve month waves

- Account for dependencies and resource constraints

- Establish cross-functional governance including business, IT, risk, and compliance

Select the Right Platforms and Partners

Evaluate vendors on security, regulatory alignment, data residency options, and financial sector references.

Vendor selection criteria:

- Swiss or EU hosting options protecting data sovereignty

- Integration capabilities with existing core systems

- Total cost of ownership and implementation timelines

- Ability to customise workflows without heavy coding

Choosing sovereign platforms like InvestGlass avoids reliance on American or Chinese ecosystems for sensitive financial data.

Implement, Train, and Iterate

Successful implementation combines agile delivery with comprehensive change management.

Execution best practices:

- Pilot projects with selected branches or business units

- Comprehensive training for relationship managers, operations, compliance, and IT

- Feedback loops with users and clients to refine journeys over time

Why InvestGlass Is a Sovereign Solution for Banking Digital Transformation

InvestGlass is a Swiss CRM and automation platform built specifically for banks, wealth managers, and regulated institutions requiring data sovereignty.

The platform unifies CRM, digital onboarding, portfolio management, compliance workflows, marketing automation, AI tools, and a secure client portal in a single environment.

InvestGlass strengths:

- Swiss hosting or full on-premise deployment options

- Control over where client data resides and who can access it

- Purpose-built for financial services regulatory requirements

- Alternative to American or Chinese software ecosystems

- Integration with existing core banking systems via APIs

Core Capabilities of InvestGlass for Banks

InvestGlass provides comprehensive functionality across the client lifecycle.

Platform modules:

- CRM centralising client information, interactions, and relationship hierarchies

- Digital onboarding with electronic forms, document collection, and identity verification integration

- Rule-based approval workflows for KYC and compliance

- Portfolio management monitoring positions, performance, and risk metrics

- Marketing automation enabling compliant segmented campaigns

- Secure client portal for document access, portfolio viewing, and adviser communication

- AI-powered workflow automation and client insights

Data Sovereignty, Compliance, and Security Advantages

Swiss hosting and on-premise deployment support strict data residency policies and reduce exposure to foreign extraterritorial laws.

Compliance and security features:

- Fine-grained access control and comprehensive audit trails

- Encryption meeting regulatory expectations for client data protection

- Built-in compliance workflows documenting KYC decisions and suitability assessments

- Audit-ready records for regulatory examinations

These characteristics make InvestGlass suitable for private banks, asset managers, and public sector entities prioritising sovereignty and regulatory certainty.

Conclusion: Preparing for Banking’s Digital Future

Digital transformation in banking is now an ongoing capability rather than a one-off project. Customer expectations, regulatory requirements, and competitive pressure from digital-native providers continue accelerating the pace of change across the financial sector.

Success requires combining modern technology with strong governance, cultural change, and careful partner selection. For financial institutions planning long-term digital roadmaps, data sovereignty and trusted European solutions have become strategic priorities. InvestGlass provides a practical sovereign platform helping banks modernise CRM, onboarding, portfolio management, and compliance while retaining full control over client data. The next three to five years will reward institutions that embrace digital transformation with platforms designed for both innovation and sovereignty.

Related articles

Swiss Sovereign CRM: Built on AI.

Ready to act.