Key Takeaways

Modern bank loyalty programs and financial loyalty programs are no longer “nice-to-have” perks. In 2026, a financial services loyalty program is a measurable growth engine for customer retention, customer satisfaction, and share of wallet across cards, savings accounts, loans, insurance, wealth, and digital wallets.

- Leading financial institutions use loyalty programs to reduce customer churn, increase customer engagement, and deepen customer relationships with existing customers.

- The best programs reward customer behavior such as saving regularly, using online banking, consolidating assets, paying on time, and adopting digital channels.

- Data, AI, and automation are now table stakes in the banking industry because customer expectations are shaped by real-time, personalized rewards.

- InvestGlass provides an end-to-end loyalty and engagement layer for banks, wealth managers, brokers, and fintechs, helping turn a loyalty initiative into measurable revenue.

What Is a Financial Services Loyalty Program?

Financial services loyalty programs are structured rewards systems offered by banks, credit card issuers, investment firms, and insurance companies. They reward customers for ongoing financial behaviors, not just one-off repeat purchases.

Unlike retail rewards programs, bank loyalty programs connect benefits to balances, risk profile, product usage, and long-term customer relationships. Loyalty programs are customer retention tools used by financial institutions to incentivize product usage.

A bank or credit union can run one customer loyalty program across checking, savings accounts, debit cards, credit cards, mortgages, insurance, and wealth products. Financial institutions track overall relationship and spending behavior to award points, cash back, or premium perks.

Common loyalty program features include loyalty points, interest boosters, fee waivers, cash rewards, cash back rewards, partner discounts, reward coupons, reward sharing, and priority support. Customers receive immediate value through waived account or transaction fees, ATM fee rebates, and discounts on mortgage origination.

In 2026, regulators in the EU, UK, and selected APAC markets scrutinize transparency, expiry rules, data use, and fairness. Transparency in loyalty programs is vital to keeping customers informed on how to earn and redeem rewards, including notifying them about fees, restrictions, and possible reward expirations.

Why Financial Services Loyalty Programs Matter in 2026

Rising interest rates between 2022 and 2024, inflation, and fintech competition pushed financial service providers to defend deposits and their customer base. Loyalty programs improve the value that customers receive from financial services, effectively increasing customer retention and reducing churn.

About 90% of businesses reward devoted customers via a loyalty program, which is a key strategy for enhancing customer retention in the financial sector. In financial services, the stakes are higher because switching a primary bank affects deposits, lending, investments, and trust.

There is also an approachability gap. Many customers still see financial services companies as complex or intimidating. Programs that promote customer satisfaction through education, savings milestones, and recognition of good habits can foster customer loyalty and create lifelong relationships.

Financial services loyalty programs create new touchpoints that engage customers outside of traditional transactions, which helps to maintain customer relationships and reduce the likelihood of switching to competitors. They also help banks encourage repeat business without relying only on higher card spend.

Boards now expect more than enrollment numbers. Open Loyalty’s 2026 trends research notes that loyalty teams increasingly focus on customer lifetime value, while Forrester’s 2026 banking trends highlight AI, trust, and differentiation as key forces reshaping consumer banking.

How the Banking Industry Is Changing the Rules of Loyalty

Since 2020, challenger banks, BNPL providers, embedded finance, and mobile-first products have changed how customers judge loyalty. Younger customers compare a bank loyalty program with subscriptions, retail apps, and travel platforms. If fees, rewards, or digital UX feel outdated, they leave.

The shift is from product-centric rewards to relationship-centric bank loyalty reward programs. Instead of rewarding only card spend, many banks now measure the total value of a household, entrepreneur, or SME across deposits, loans, investments, insurance, and digital activity.

Open banking and APIs make this possible. Financial services loyalty programs can ingest data from cards, robo-advisors, wallets, and partner platforms to personalize offers. Using data analytics and agentic AI in banking to understand customer preferences allows businesses to offer personalized rewards that align with individual interests, enhancing engagement.

AI adds another layer. A global financial services company can score churn risk, detect life events, and trigger the next best action after a salary deposit, mortgage inquiry, or first investment. This is how financial institutions influence loyalty in a competitive market: by showing up at the right moment.

Core Types of Bank Loyalty Programs

Most bank rewards programs are hybrids. The right structure depends on business objectives, target customers, customer preferences, and the cost of rewards.

Type | How it works | Best use |

|---|---|---|

Points-based | Customers earn points for spending or behaviors | Broad engagement |

Tiered | Benefits rise with relationship value | High value customers |

Cashback | Percentage of spending returned | Simple value |

Gamified | Challenges and milestones | Digital adoption |

Partner-based | Benefits across merchants and airlines | Ecosystem loyalty |

Points-based programs allow customers to earn points for each purchase, which can be redeemed for discounts, freebies, or other rewards once a certain threshold is reached. In banking, customers earn points for card spend, salary deposits, referrals, or digital actions. |

Tiered loyalty programs categorize customers into different levels based on their engagement and purchase history, offering unique benefits and rewards to higher-tier customers. High-value tiers grant expedited customer support through dedicated premier helplines and priority service routing.

Cashback programs reward repeat customers with a percentage of their spending, which can be returned as cash, deposited into their accounts, or offered as store credit for future purchases. These models are popular during cost-of-living pressure because the benefit is easy to understand.

Gamification programs engage customers by incorporating game-like elements, where customers complete challenges to earn rewards and enhance their loyalty experience. A bank might rewards customers for going paperless, completing a budget review, or using prepaid and digital wallet accounts.

Referral programs leverage word-of-mouth marketing by rewarding customers for bringing in new leads, often through unique codes that provide monetary rewards or special deals when referrals sign up. They help attract new customers and more customers at lower acquisition cost.

Digital Wallets and Embedded Loyalty

Digital wallets such as Apple Pay, Google Pay, and proprietary bank wallets became mainstream between 2020 and 2025. Today, mobile banking apps often include features to track, manage, and redeem rewards during financial tasks.

Embedded loyalty lets customers see balances, offers, and instant benefits at payment time. Use cases include “pay with points,” instant reward coupons, fee-waiver vouchers, or savings boosters triggered when money moves into a wallet sub-account.

Wallet data is valuable because it is granular and near real time. A bank can identify commuters, frequent travelers, subscription spenders, or customers with high airline and holiday expenditures, then serve meaningful rewards without sending irrelevant promotions.

Neobanks such as Revolut have used in-app incentives and merchant offers to drive engagement. InvestGlass APIs and financial CRM workflows can track wallet behaviors and trigger rewards, reminders, or relationship-manager alerts automatically.

Real-World Examples of Bank Loyalty Programs (2020–2026)

Bank of America’s Preferred Rewards program offers tiered benefits based on account balances, providing customers with increased rewards and discounts as they maintain higher balances, which encourages customer loyalty. The preferred rewards program has been known for fee waivers, rate discounts, and credit card reward boosts. In 2026, Bank of America also moved toward broader access through BofA Rewards.

Citibank’s Citi ThankYou Rewards program allows customers to earn points through various banking activities, which can be redeemed for cash back, gift cards, or travel, showcasing a flexible and engaging loyalty structure. Wells Fargo’s Go Far Rewards program allows customers to earn points on purchases made with their credit cards, which can be redeemed for various rewards, including travel and gift cards, enhancing customer engagement.

American Express Membership Rewards program is known for its extensive redemption options, allowing cardholders to earn points on everyday purchases that can be used for travel, merchandise, and more, demonstrating the effectiveness of diverse reward offerings. Customers also compare ecosystems such as chase ultimate rewards, ultimate rewards, and products like the quicksilver credit card when judging bank’s reputation and value.

In South Africa, FNB eBucks shows how mature services loyalty can shape everyday payments. Public reporting in 2026 highlighted nearly 8 million users, 87% active engagement, R2.3 billion in customer value in 2025, and a high earn-to-spend ratio. Educational or youth-focused programs also matter because early savings rewards, grades-based incentives, and financial literacy badges can foster long term loyalty.

Designing a Modern Financial Services Loyalty Strategy

Start with the outcome. An effective bank loyalty program should support business objectives such as primary-bank status, digital adoption, deposit growth, cross-sell, or lower customer churn.

Set key performance indicators early: customer retention, products per customer, active digital users, CSAT, NPS, profitability, and lifetime value. Measuring and optimizing loyalty program performance requires defining key performance indicators (KPIs) that correspond with the program’s objectives and regularly analyzing them to assess effectiveness.

Segmentation should go beyond age and income. Use customer behavior, life stage, risk profile, product holdings, and channel preference. Young professionals may value fee waivers and overdraft protection. Affluent customers may value preferential yields, wealth access, and dedicated support.

Creating a clear value proposition for loyalty programs is essential, as customers need to understand the benefits they’ll receive in exchange for their loyalty, such as cashback or travel rewards. Simplifying program enrollment and reward redemption processes is crucial to encouraging participation and maintaining customer satisfaction.

Key Features of High-Performing Bank Rewards Programs

A successful loyalty program should offer a variety of reward options to cater to the diverse preferences within a bank’s customer base, including cash rewards, travel benefits, and merchandise discounts.

Key benefits of these programs include lower interest rates, waived service fees, and direct cashback rewards. Enrolled users unlock preferential interest rates on savings products, certificates of deposit (CDs), and lowered borrowing costs on personal loans.

Fee waivers eliminate standard banking costs like ATM fees, foreign transaction fees, and monthly maintenance charges. For loyal customers, this can be more valuable than abstract points.

Personalization is critical. Personalization in loyalty programs can increase customer satisfaction by as much as 6.4 times when implemented effectively. Yet only 20% of loyalty program members are completely satisfied with the brand’s approach to personalization, indicating a significant opportunity for improvement.

Strong programs communicate across email, SMS, push, secure in-app messages, web, ATMs, and branches. They also protect trust through authentication, encryption, consent management, and clear redemption rules.

Leveraging Data, AI, and Automation for Loyalty

Loyalty data becomes powerful when it is connected. Transaction history, balances, product holdings, app logins, wallet usage, partner redemptions, and customer feedback all create valuable insights.

Banks can use AI to predict churn, identify next-best offers, and incentivize customers before they disengage. For example, a customer who stops using online banking or moves salary deposits elsewhere can receive a targeted retention offer.

Real-time decisioning evaluates events such as a card swipe, app login, loan application, or investment trade. The system then chooses whether to offer loyalty points, cash back, a fee waiver, or a relationship-manager task.

Ethical use matters. Financial institutions need anonymization, role-based access, clear consent, and explainable rules. This is especially important when rewards affect pricing, credit, or access.

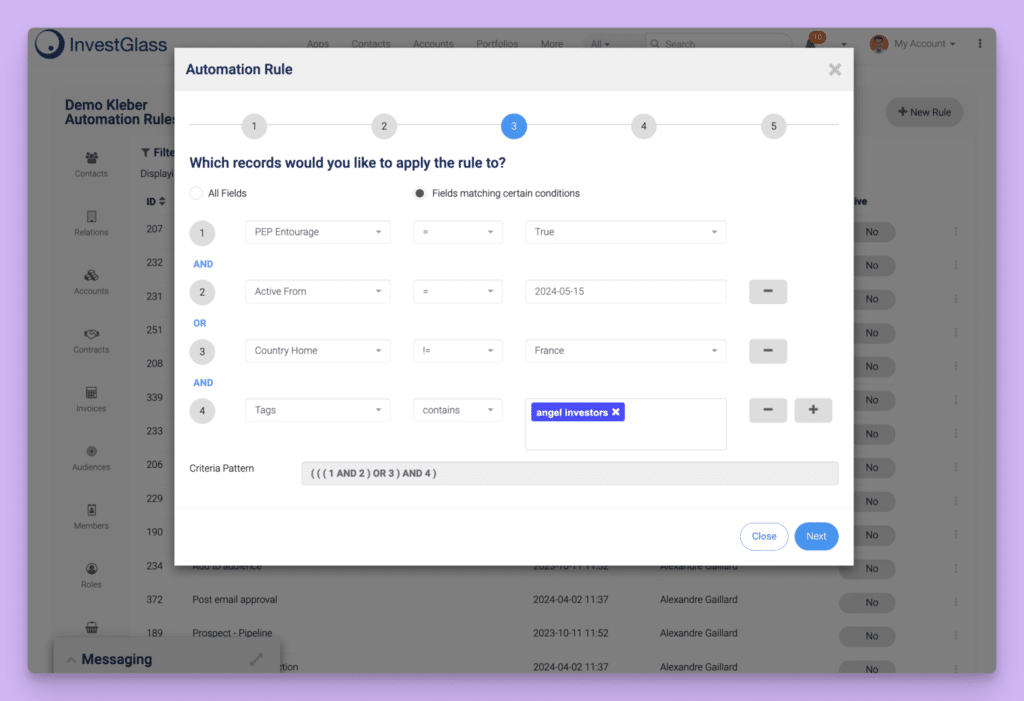

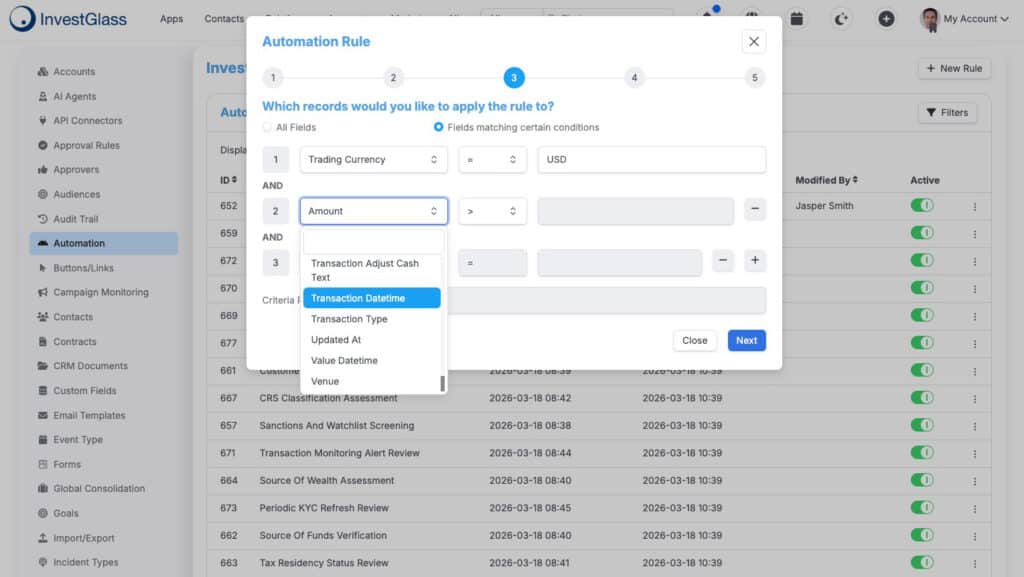

InvestGlass acts as an orchestration layer by centralizing profiles, scores, communication preferences, and workflows, including automated KYC verification. It helps financial institutions create personalized rewards at scale while maintaining compliance controls.

InvestGlass: Building Loyalty Journeys for Banks and Wealth Managers

InvestGlass is a Swiss-based, compliance-ready CRM and automation platform built for banks, wealth managers, brokers, and fintechs. It helps financial services sector teams design, launch, and monitor customer loyalty programs without rebuilding core systems.

InvestGlass centralizes KYC, transactions, product holdings, risk profile, notes, suitability data, and communication preferences. That unified private banking CRM view helps financial services companies understand who should receive a rewards account upgrade, a savings campaign, or a retention journey.

Loyalty-specific workflows can include engagement scoring, balance-based segmentation, product-usage triggers, and digital-adoption campaigns. For example, InvestGlass can trigger a message when a client reaches a savings target, opens a mortgage, makes a first investment trade, or becomes eligible for a premium tier.

The platform can integrate with core banking systems, card processors, CRMs, portfolio tools, and digital wallets via APIs, supporting AI-driven portfolio management alongside loyalty use cases. This lets loyalty logic run on top of current infrastructure.

Practical examples include:

- Fee waivers for customers who move recurring payments to the bank.

- Targeted rate boosters for high-value savers.

- Alerts for relationship managers when customers are close to tier progression.

- Automated campaigns for customers who should redeem rewards before expiry.

InvestGlass also supports private-cloud and on-premise deployment options, European hosting, audit trails, approvals, and GDPR-aligned data protection features.

Implementation Roadmap: From Concept to Live Program

A financial services loyalty program can often move from concept to launch in 6–12 months when the scope is clear.

- Discovery and planning: run workshops with product, marketing, compliance, IT, finance, and frontline teams. Benchmark other financial institutions and collect customer feedback, taking inspiration from specialized CRM setups in other verticals.

- Commercial modeling: forecast reward costs, expected uplift, break-even timelines, and margin impact.

- Technical design: select the technology stack, including InvestGlass as an engagement layer, then map data flows and customer journeys.

- Phased rollout: pilot with one region, one segment, or one product line before full release.

- Internal enablement: train branches, call centers, and relationship managers so staff can explain benefits.

- Communication: use teasers, launch campaigns, FAQs, and ongoing education.

The easiest program to launch is not always the most profitable. Start small, but design for scale.

Managing Risks, Compliance, and Operational Challenges

Common risks include cost overruns, point liabilities, fragmented systems, regulatory scrutiny, fraud, and customer confusion. Many banks underestimate how hard it is to coordinate offers across products and channels.

Data security requires strict access controls, encryption, logging, and monitoring, similar to the safeguards in specialized healthcare and therapy CRMs. Fraud teams must watch for synthetic identities, account takeover, and suspicious loyalty points redemption.

Fair treatment is equally important. Eligibility rules must not exclude vulnerable customers or protected groups unfairly. A customer loyalty program tied only to large balances can create reputational and regulatory risk if it is not balanced with accessible benefits.

InvestGlass workflows, approval rules, permissioning, and audit trails support compliant campaign setup and change tracking. This gives marketing teams speed without removing compliance oversight.

Measuring Success: KPIs and Optimization Cycles

Enrollment is not enough. A successful loyalty program must prove financial impact and customer sentiment.

Track:

- Customer retention and customer churn.

- Share of wallet and products per customer.

- Digital activity, including app logins and wallet use.

- Customer satisfaction and NPS.

- Active members, redemption rate, and offer response.

- Incremental revenue and reward cost.

Compare engaged members with non-engaged customers. If members redeem rewards, hold more products, and stay longer, the program is working.

Review performance quarterly. Adjust earn points rules, partner offers, tier thresholds, and communication frequency. Platforms like InvestGlass provide dashboards and automated reports so executives can align on what is working.

Future Trends in Financial Services Loyalty

Through 2028, financial services loyalty will become more predictive, embedded, and wellbeing-focused.

ESG-linked rewards will grow, including incentives for sustainable investments, green mortgages, and climate-friendly spending. Tokenization may also reshape rewards through programmable points, digital currencies, and blockchain-based transparency.

Subscription-style loyalty will expand, with customers paying monthly for bundled benefits such as higher rates, no fees, insurance perks, and premium support. Some financial institutions may also offer loyalty-as-a-service to partners.

The bigger trend is convergence. Banking, insurance, investments, and advice will merge into unified financial wellbeing journeys. Flexible, API-first tools like InvestGlass help institutions adapt without replacing core systems.

Conclusion

Financial services loyalty programs have moved from simple bank rewards programs to strategic, data-driven ecosystems. They now shape customer retention, customer engagement, pricing, product adoption, and emotional loyalty.

The institutions that win will not be the ones with the most complicated points catalog. They will be the ones that make loyalty easy to understand, easy to redeem, compliant, and personally relevant.

Banks, wealth managers, fintechs, and credit union teams should treat loyalty as an operating capability, not a campaign. If you want to orchestrate compliant, personalized journeys across the entire customer base, InvestGlass gives you the tools to build, automate, and measure them.

FAQ

How is a financial services loyalty program different from a retail loyalty card?

A retail loyalty card usually rewards shopping frequency. A financial services loyalty program is tied to regulated products such as bank accounts, loans, investments, insurance, and payment cards.

That makes design more complex. Bank loyalty programs may influence fees, interest rates, borrowing costs, and risk behaviors such as on-time payments or savings habits.

Financial services also use deeper data, which enables more precise personalization but requires stronger privacy safeguards, consent, and auditability.

Can a bank loyalty program work without a credit card component?

Yes. Modern financial services loyalty programs can reward debit card usage, salary deposits, savings goals, account balances, app logins, paperless statements, and digital education.

For example, a low-risk program for underbanked customers could focus on fee waivers, savings streaks, and digital literacy instead of credit card spend.

InvestGlass can orchestrate non-card journeys by monitoring behaviors across multiple products and channels.

How long does it typically take to launch a new financial services loyalty program?

A realistic timeline for a mid-size institution is 6–12 months from scoping to full rollout, assuming digital channels already exist.

Pilots can often launch in 3–6 months when the bank starts with one region, one product line, or one customer segment.

Using a pre-built engagement platform like InvestGlass can shorten campaign design, workflow automation, and integration phases.

What budget should financial institutions expect to allocate for loyalty initiatives?

Budgets vary, but most include three categories: technology costs, reward funding, and internal staffing or consulting.

The business case should show that incremental profit from higher retention, cross-sell, and engagement outweighs reward and platform costs within 18–36 months.

Start with scenario analysis so the loyalty initiative is neither underfunded nor too generous to remain profitable.

How can smaller banks or wealth managers compete with large-bank loyalty programs?

Smaller institutions can compete by focusing on niche segments, deeper personalization, and faster experimentation instead of copying every large-bank perk.

Local merchant networks, specialized investment partners, and relationship-led service can create benefits that feel more personal than generic cashback.

InvestGlass lowers the technology barrier, helping smaller teams run sophisticated, compliant loyalty journeys without building everything in-house.

Related articles

Swiss Sovereign CRM: Built on AI.

Ready to act.