CRM data becomes a financial decision engine when it is complete, clean, and connected to core banking, portfolio, and accounting systems, enabling firms to move beyond contact tracking into strategic intelligence.

Financial institutions can use CRM insights to improve pricing, risk assessment, liquidity planning, and profitability analysis throughout 2024 and 2025 planning cycles.

InvestGlass, as a Swiss sovereign CRM, lets firms combine client, portfolio, and onboarding data inside Switzerland for compliant decision making under Swiss data protection law and GDPR.

Practical use cases include dynamic client segmentation, product profitability analysis, next best action recommendations, and real time forecasting that connects front office activity to balance sheet outcomes.

This article provides a concrete, step by step path to move from scattered records to a decision grade CRM data framework that delivers measurable financial value.

Introduction: From Relationship Database to Financial Decision Engine

Picture a mid sized Swiss wealth manager in 2024 with separate systems for customer relationship management, portfolio management, and accounting. Advisors spend hours reconciling spreadsheets while finance leaders struggle to answer basic questions about client profitability or pricing optimization. The data exists, but it lives in data silos that prevent anyone from seeing the complete picture needed for confident financial decisions.

CRM data in a financial context includes far more than contact details and meeting notes. It encompasses complete client profiles, KYC documentation, interaction history, product holdings, cash flows, service requests, and behavioral patterns that reveal how customers engage with your firm. When this customer data is properly structured and connected, it transforms from a static relationship database into a dynamic decision engine.

The goal of this article is to show how banks, wealth managers, insurers, and asset managers can turn combined CRM and financial data into better, faster financial decisions at the relationship, product, and balance sheet level. We will focus on concrete examples rather than abstract theory, with direct relevance to 2024 and 2025 planning cycles.

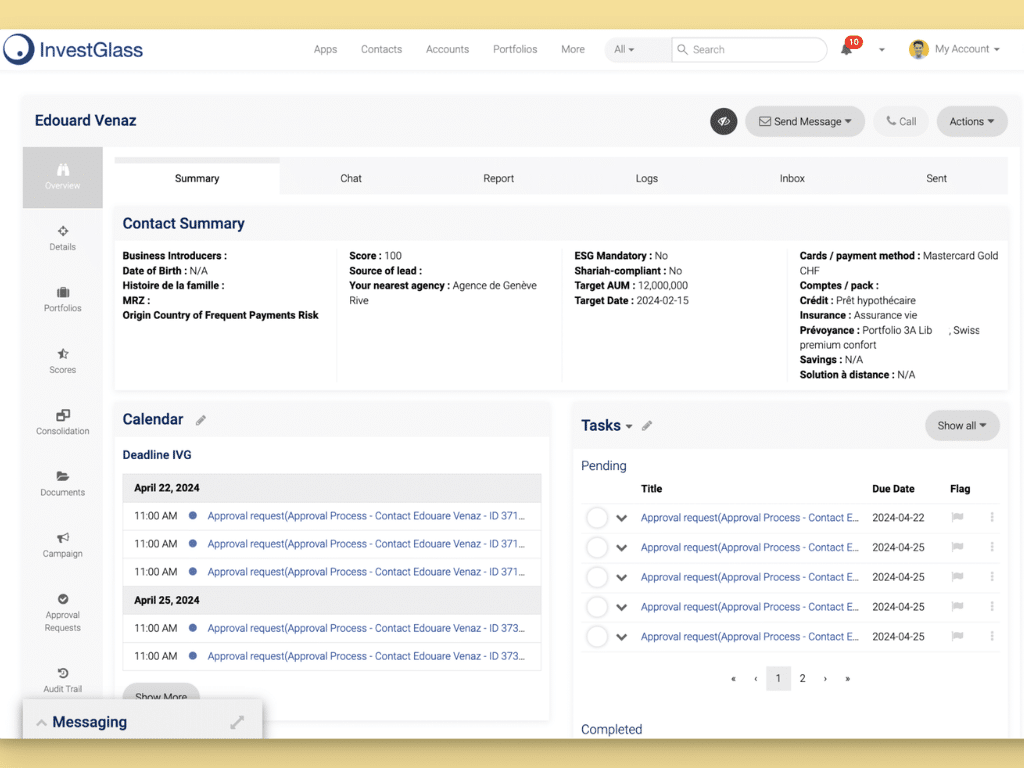

InvestGlass is a Swiss hosted CRM and automation platform used by regulated financial institutions to unify these data points under Swiss data sovereignty rules. Throughout this guide, we will reference how firms are using InvestGlass to build decision grade CRM foundations that connect client engagement to financial performance.

Step 1: Build a Decision Ready CRM Data Foundation

Meaningful financial decisions require accurate, structured, and permissioned data in your CRM systems, not just scattered contact notes and informal relationship tracking. Before you can extract actionable insights, you need to ensure your data foundation supports the analysis you want to perform.

A high quality CRM dataset in finance includes several essential components:

Data Category | Key Elements |

|---|---|

Client Profiles | Complete KYC profiles, risk profiles, investment objectives, documented preferences |

Relationship Hierarchies | Household structures, entity relationships, beneficial ownership |

Portfolio Data | Asset holdings, valuations, performance history, mandate types |

Interaction Records | Communication history, meeting notes, service requests, campaign responses |

Financial Metrics | Revenue attribution, fee structures, service costs, profitability indicators |

Consider a Swiss private bank that consolidated data from its core banking system, portfolio management tool, and email communications into InvestGlass during 2024. Previously, advisors had no way to see total relationship value alongside recent client interactions. After integration, they could identify that certain clients generating modest fee revenue were actually among their most engaged, signaling opportunities for relationship expansion.

Standard data models matter enormously here. When clients, households, entities, accounts, and products follow consistent structures, you can link revenue, cost, and risk figures reliably across the organization. Without this consistency, your client data becomes difficult to aggregate and impossible to trust for strategic decisions.

Data quality routines should run weekly or daily to catch problems before they affect reports. Common issues include missing risk ratings, invalid contact details, or inconsistent currency fields. Automated validation in your crm software can flag these gaps, allowing operations teams to resolve them proactively rather than discovering errors during critical reporting periods.

Step 2: Connect CRM Data with Financial and Risk Systems

Customer relationship management alone is not enough to drive financial decisions. The real power emerges when your CRM is integrated with core banking, portfolio management, treasury, and accounting software, creating a unified view of each client relationship and its financial impact.

InvestGlass can sit at the center of your technology architecture and synchronize data with systems such as Avaloq, Temenos, or proprietary portfolio engines using secure APIs hosted in Switzerland. This eliminates the need for manual data entry between systems and ensures that advisors and finance teams work from the same source of truth.

Effective integration involves several concrete data flows:

- Daily positions and valuations imported from portfolio systems into the CRM

- Batch imports of fees, commissions, and transaction costs from accounting software

- Overnight updates of risk scores, credit ratings, or rating migrations from risk platforms

- Real time alerts when key thresholds are breached across any connected system

When these connections are established, finance teams see client level profitability, product margins, and cash flow schedules directly inside CRM dashboards. They no longer need to reconcile multiple systems using spreadsheets, which reduces errors and accelerates decision cycles.

Consider a 2025 scenario where an insurer uses integrated CRM and policy administration data to adjust underwriting appetite by segment. By analyzing historical data on claims frequency alongside client engagement patterns stored in the CRM, the risk team identifies that highly engaged policyholders in certain segments have significantly better loss ratios. This insight informs both pricing decisions and marketing resource allocation toward the most profitable customer segments.

Step 3: Use CRM Data to Improve Client Level Financial Decisions

The first place to apply CRM data for financial decisions is at the single client or household level where financial advisors operate every day. This is where improved customer insights translate directly into better client relationships and stronger business outcomes.

Advisors in 2024 and 2025 face several critical decisions that benefit from integrated CRM data:

- Investment proposal development based on complete risk profiles and historical preferences

- Credit limit adjustments informed by relationship profitability and behavioral patterns

- Pricing of advisory mandates that reflects true service costs and client value

- Prioritization of outreach based on engagement trends and revenue potential

Combining communication history with portfolio performance and risk profile data allows advisors to make more suitable product recommendations. This approach not only enhances customer service but also reduces the risk of mis selling, which carries both regulatory and reputational consequences for financial institutions.

Here is a practical numerical example. A wealth manager calculates recurring fee revenue and estimates service cost per client based on meeting frequency, administrative requests, and complexity of portfolio reporting. The analysis reveals:

Client Tier | Annual Revenue | Service Cost | Net Profit | Percentage of Clients |

|---|---|---|---|---|

Profitable | Above CHF 15,000 | Below CHF 5,000 | Above CHF 10,000 | 25% |

Marginal | CHF 8,000 to 15,000 | CHF 5,000 to 8,000 | CHF 0 to 7,000 | 45% |

Loss Making | Below CHF 8,000 | Above CHF 8,000 | Negative | 30% |

This segmentation drives different strategies: personalized services and proactive outreach for profitable clients, efficiency improvements for marginal relationships, and fee discussions or service model changes for loss making accounts.

InvestGlass workflows can trigger automated alerts when a client drops below a target profitability threshold or when cash balances exceed a defined idle cash ratio. These alerts enable advisors to take action before small issues become significant problems, supporting better client management across the entire book.

Step 4: Portfolio and Product Decisions Informed by CRM Insights

Looking beyond individual client interactions, aggregated CRM data reveals which products and mandates are truly profitable once acquisition cost, servicing intensity, and churn are taken into account. This analysis often produces surprising results that contradict intuition based solely on headline fee rates.

The approach involves grouping clients by portfolio type, mandate type, and risk class within the CRM, then comparing realized margins, portfolio performance, and retention rates across those groups. Predictive analytics can extend this analysis to forecast future profitability based on client behavior patterns.

A 2024 example illustrates the value. A wealth manager compared two popular offerings: a low fee discretionary mandate and a higher fee execution only service. Initial analysis favored the execution only product based on gross margins. However, when service costs were fully allocated including trade support, reporting requests, and relationship manager time, the discretionary mandate delivered significantly higher net margins. Additionally, retention rates for discretionary clients averaged 92% compared to 78% for execution only clients.

This insight enabled the firm to shift marketing automation campaigns away from the execution only product toward discretionary mandates with better risk adjusted economics. Client acquisition efforts became more strategic, focusing on potential clients likely to adopt the higher retention offering.

Beyond profitability, CRM linked portfolio views support monitoring of product risk concentration. Finance and risk teams can track exposure by sector, currency, ESG score, or other dimensions across the entire client base. When concentrations exceed internal limits, workflow automation triggers reviews and alerts before regulatory or internal policy breaches occur.

Step 5: Forecasting Revenue, Liquidity, and Capital with CRM Data

CRM data serves as a leading indicator that allows financial leaders to forecast revenue and liquidity earlier than accounting figures alone permit. While financial reporting tells you what happened, CRM data tells you what is likely to happen, enabling firms to plan proactively.

Opportunity pipelines, mandate renewals, and expected inflows or outflows recorded in the CRM can feed a monthly revenue forecast for the next 6 to 12 months. This approach transforms financial planning from backward looking analysis into forward looking strategy.

Consider a Swiss asset manager in 2025 using InvestGlass to model scenarios based on:

- Conversion rates for prospects at different pipeline stages

- Average ticket size for new mandates by client segment

- Seasonal redemption patterns based on historical data

- Mandate renewal probabilities informed by client engagement scores

By adjusting these parameters, finance teams can produce optimistic, baseline, and pessimistic revenue forecasts with clear assumptions documented in the system. This data driven approach replaces gut feel with structured analysis that can be tested and refined over time.

Treasury and ALM teams benefit from similar forecasting capabilities. Expected client flows from the CRM refine liquidity buffers and funding plans, particularly for term deposits and structured products where timing of inflows and outflows significantly affects capital efficiency. Real time data access to CRM based forecasts allows treasury to adjust positions as client behavior patterns shift.

Regulators and internal risk committees in FINMA supervised institutions expect documented assumptions behind financial projections. CRM based forecasting provides audit trails that satisfy these requirements, with clear evidence of the customer information and historical data used to generate predictions.

Step 6: Risk Management and Compliance Decisions Based on CRM Data

CRM is also a crucial risk and compliance dataset, not just a sales tool. This is especially true under European and Swiss regulations where firms must demonstrate that they understand their clients and have appropriate controls in place.

Onboarding, KYC, and suitability records stored in InvestGlass enable risk based decisions across the client lifecycle. Examples include:

- Tightening trading limits for high risk jurisdictions

- Enhanced monitoring for politically exposed persons

- Adjusted service models for clients with complex beneficial ownership structures

- Periodic review scheduling based on risk classification rather than arbitrary timelines

Monitoring patterns in 2024 revealed that certain behaviors consistently preceded compliance issues. These included unusually frequent address changes, large cash transactions inconsistent with stated source of wealth, and unexpected cross border activity. When these patterns are detected through CRM analysis, compliance teams can trigger reviews before potential issues escalate.

CRM based segmentation helps compliance teams allocate enhanced due diligence and review resources according to actual risk rather than treating all clients identically. This approach improves operational efficiency while ensuring that higher risk relationships receive appropriate attention.

For firms that must keep regulatory and client records inside Swiss borders, data sovereignty matters enormously. InvestGlass offers Swiss data center hosting or on premise deployment options, ensuring that sensitive customer data and compliance documentation remain within the required jurisdictional boundaries.

Step 7: Applying AI and Automation to Turn CRM Data into Actions

Once CRM data is structured and connected, AI can support decisions by recommending next best actions and predicting outcomes. This transforms raw data into practical guidance that advisors and risk officers can act upon immediately.

InvestGlass AI capabilities can score leads and existing clients for upsell opportunities or retention risk using signals such as:

- Engagement levels measured through email opens, portal logins, and meeting frequency

- Portfolio performance relative to benchmarks and client expectations

- Service ticket frequency and resolution satisfaction

- Life event indicators that suggest changing financial needs

A 2024 example shows an advisory team using AI suggestions to prioritize quarterly reviews with clients whose portfolios deviate from target allocations by more than defined thresholds. The system automatically flagged 47 relationships requiring attention, which advisors would have identified manually only with significant delay.

Workflow automation extends these capabilities by adjusting tasks, reminders, and approvals based on quantitative thresholds. When a portfolio drawdown exceeds acceptable limits, the system creates a review task. When fee coverage ratios fall below minimums, account management receives alerts. These automated responses ensure consistent application of business rules across the organization.

Explainability matters when using AI for financial decisions. Advisors and risk officers need to see which data points drove a given recommendation to maintain accountability and regulatory compliance. InvestGlass provides transparency into AI scoring factors, enabling firms to explain and justify recommendations when required.

Implementing a CRM Data Strategy for Better Financial Decisions

This section provides a practical roadmap for firms that want to start in 2024 and see measurable impact on decisions within 6 to 12 months. The approach is deliberately phased to manage complexity and demonstrate value at each stage.

Phase 1: Discovery and Data Audit (Weeks 1 to 4) Assess current data quality across CRM, portfolio, and financial systems. Identify gaps in client data, inconsistent field definitions, and integration requirements. Document current decision processes that would benefit from better data.

Phase 2: Integration of Key Systems (Weeks 5 to 12) Connect CRM with core banking, portfolio management, and accounting platforms. Establish automated data flows and validation routines. Eliminate manual data entry where possible.

Phase 3: Rollout of Decision Dashboards (Weeks 13 to 20) Deploy client profitability, product margin, and pipeline forecasting dashboards. Train finance and front office teams on interpretation and use. Begin replacing spreadsheet based analysis with CRM based reporting.

Phase 4: AI and Automation Introduction (Weeks 21 to 30) Implement scoring models for retention risk and upsell opportunity. Deploy automated alerts and task management based on business rules. Refine models based on initial results.

Firms should set 3 to 5 measurable targets to track progress:

- Improve revenue forecast accuracy by 15% within 6 months

- Reduce manual spreadsheet reconciliations by 20 hours per month

- Increase client profitability visibility from 60% to 95% of relationships

- Decrease time to prepare regulatory reports by 30%

InvestGlass projects typically begin with digital onboarding and KYC, which immediately improves data quality and consistency. From this foundation, firms expand into portfolio dashboards, marketing automation, and risk workflows. This sequence ensures that each phase builds on verified data from the previous stage.

Looking ahead, firms preparing for 2026 and beyond should recognize that customer expectations and regulatory requirements will continue increasing. A solid CRM foundation built today positions your institution to adapt quickly, whether that means incorporating new data sources, adopting advanced analytics, or responding to emerging compliance mandates.

Why Use InvestGlass for CRM Driven Financial Decisions

InvestGlass is a Swiss sovereign CRM, portfolio management, and client portal platform purpose built for regulated financial institutions. Unlike generic crm platforms adapted for finance, InvestGlass was designed from the ground up for banking, wealth management, and insurance workflows.

Specific strengths for better financial decisions include:

- Integrated Digital Onboarding and KYC: Complete client files from day one, with document management and suitability assessment built in

- Portfolio Reporting: Real time portfolio views connected to CRM client records enable true relationship level profitability analysis

- Marketing Automation: Campaign management that targets clients based on financial characteristics, not just demographics

- Workflow Automation: Business rules that trigger tasks, alerts, and approvals based on financial thresholds and risk indicators

- Client Portal: Self service access that reduces administrative burden while enhancing client engagement

InvestGlass is hosted in Switzerland or available for on premise deployment, supporting Swiss data protection law, GDPR, and internal data residency policies of banks and asset managers. This addresses concerns that prevent many financial institutions from adopting cloud based crm software.

Typical clients include private banks, external asset managers, family offices, insurers, and fintechs that need integrated tools for managing customer relationships across the client lifecycle. These firms benefit from having CRM, compliance, and portfolio capabilities in one environment rather than managing multiple systems.

While competitors like Salesforce Financial Services Cloud, HubSpot, and Microsoft Dynamics 365 offer CRM capabilities, InvestGlass provides the Swiss sovereignty and purpose built financial services functionality that regulated institutions require. The platform enables firms to enhance client engagement while maintaining the data security and compliance standards expected in the financial services industry.

If you want to see how your existing financial and CRM data can be consolidated into decision grade dashboards and workflows, InvestGlass offers demonstrations tailored to your specific use cases and data environment.

FAQ

How quickly can a financial institution start using CRM data for better decisions

Most banks and wealth managers can see first decision making improvements within 60 to 90 days if they start with a focused pilot such as revenue forecasting or client profitability analysis. The timeline typically includes a two week data assessment, a four to six week integration sprint with core systems, and a short training phase for finance and front office teams. InvestGlass projects can follow this phased approach without disrupting existing core banking operations, allowing firms to demonstrate value before expanding scope.

What financial metrics should be tracked inside the CRM

Key metrics include relationship level revenue, service cost per client, assets under management, net new money, fee coverage ratio, and product level margins. Each metric should be mapped to specific CRM fields and data sources so that dashboards remain consistent and auditable over time. A combined metric like profit per client segment requires both CRM engagement data and accounting inputs, illustrating why system integration matters for meaningful financial reporting.

Is it safe to store sensitive financial data in a CRM platform

For regulated institutions, safety depends on security architecture, hosting location, data encryption, and access controls of the CRM provider. InvestGlass offers hosting in Swiss data centers or on premise deployments, with role based access and audit trails designed specifically for banking and wealth management needs. The platform aligns with frameworks such as FINMA circulars and GDPR, providing compliance and risk officers with the assurance they need regarding sensitive data protection.

Do smaller advisory firms really benefit from CRM driven financial decisions

Independent asset managers and small advisory boutiques arguably benefit even more from structured CRM data, as it replaces manual spreadsheets and individual memory with systematic processes. A team of fewer than 10 advisers can use InvestGlass to centralize client files, track recurring revenue, monitor client interactions, and forecast cash flows without dedicated analysts. Cloud based access and preconfigured templates reduce the need for large internal IT teams, making enterprise grade capabilities accessible to smaller firms.

How does CRM data help with regulatory reviews and audits

Regulators increasingly expect complete client files, clear recording of advice, and transparent evidence of suitability and KYC checks. An integrated CRM like InvestGlass stores onboarding forms, risk profiles, investment proposals, customer feedback, and interaction notes with time stamps and user attribution. This structured historical data allows faster responses to audits and reduces operational risk during regulatory inspections, demonstrating that your firm has robust business processes for managing customer relationships and compliance obligations.

Related articles

Swiss Sovereign CRM: Built on AI.

Ready to act.