Advisory firm profitability in 2025 depends less on chasing ever higher fees and more on systematically reducing costs without harming client service. With fee compression squeezing margins and regulatory obligations expanding, the firms that thrive will be those that master operational efficiency while maintaining the quality of advice their clients expect.

Understanding the various fee structures and fee models that advisors charge such as AUM fees, flat fees, or hourly rates is essential for optimizing costs and ensuring transparency. Aligning these fee models with clients’ best interests not only supports regulatory compliance but also builds trust and satisfaction, forming the foundation for sustainable cost reduction in financial advisory firms.

Key Takeaways

- Advisory firm profitability in 2025 depends less on chasing ever higher fees and more on systematically reducing costs without harming client service

- The fastest savings usually come from automating onboarding and compliance tasks, rationalising technology stacks, and standardising investment and financial planning processes

- Firms that adopt integrated platforms such as InvestGlass can cut duplicated software costs, manual labour, and regulatory risk at the same time

- Cost reduction should be an ongoing discipline with defined metrics, not a one time project after markets fall

- This article focuses on practical actions for partners, COOs, and heads of compliance in small and mid sized advisory firms

Why Cost Control Matters For Financial Advisory Firms Today

Fee pressure, regulation, and rising staff salaries are compressing margins in wealth management and independent advisory firms in 2025. The economic environment has shifted dramatically, and many advisors find themselves working harder to maintain the same level of profitability they achieved five years ago.

Consider the numbers: many firms still run operating margins under 20 percent despite charging financial advisor fees around one percent of assets under management. The aum fee structure, also known as asset based fees, typically means firms charge a certain percentage of client assets annually a hallmark of the aum model. This approach has evolved, with some firms integrating or differentiating AUM fees with other service fees to optimize revenue. When you factor in the cost of compliance staff, technology subscriptions, office space, and senior advisor compensation, the money that actually flows to the bottom line can be surprisingly thin. This creates new challenges for firms trying to invest in growth while maintaining service quality.

Cost structures in advisory firms are often fixed. Rent, core systems, and senior staff salaries are difficult to adjust quickly when markets decline. When a portfolio drops 20 percent, your AUM fees drop accordingly, but your lease payment and your compliance officer’s salary stay exactly the same. This mismatch between variable revenue and fixed costs is what makes so many advisory firms vulnerable during downturns. Adopting different fee models such as flat fee, hourly fees, annual retainer, or a fee for service model can help firms better align costs and revenue, providing more flexibility in managing profitability.

Lowering the cost to serve each client allows firms to keep competitive fees, invest in better service, and withstand market volatility. When you can deliver comprehensive financial planning at a lower internal cost, you gain flexibility. You can choose to offer lower financial advisor fees to win business, or maintain current pricing and reinvest the savings into better tools and talent. Negotiating advisory fees, charging fees based on client value, and considering alternative fee structures like charging hourly, setting an hourly rate, or offering a flat annual retainer can also help achieve a lower fee for clients while maintaining firm sustainability.

The remainder of this article provides a structured roadmap rather than generic cost cutting tips. Each section addresses a specific area where advisory firms can find meaningful savings without sacrificing the quality of financial advice their clients depend on. We will also touch on fee calculation and the importance of selecting a fee structure that aligns with both firm profitability and client value.

Map Your Current Cost Structure And Client Profitability

No cost reduction initiative should begin without a detailed baseline of where money is currently spent. Too many firms jump straight to cutting expenses without understanding which cuts will actually improve profitability and which might damage their ability to serve clients effectively.

The main cost buckets in a financial advisory firm typically include:

Cost Category | Typical Percentage of Total Expenses | Key Components |

|---|---|---|

Staff Compensation | 50 to 65 percent | Advisor salaries, bonuses, employee benefits, disability insurance, payroll taxes |

Technology | 8 to 15 percent | CRM, portfolio management, reporting tools, cybersecurity |

Compliance | 5 to 10 percent | Staff, training, regulatory filings, legal reviews |

Third Party Research | 3 to 6 percent | Market data, investment research subscriptions |

Custody and Trading | 2 to 5 percent | Platform fees, trading costs |

Office Expenses | 5 to 12 percent | Rent, utilities, supplies, insurance |

Building a simple client level profitability model requires allocating time spent, technology usage, and regulatory work to each relationship. This means tracking how many hours advisors spend on each client annually, what compliance activities each client triggers, and which technology tools each relationship requires. Accurate fee calculation and understanding the impact of different fee models is essential for charging fees that reflect the true cost to serve each client.

Use historical data from 2023 and 2024 to compare how costs evolved through market cycles and regulation changes like new ESG reporting obligations in the European Union. This analysis often reveals surprising patterns about which activities consume the most resources relative to the revenue they generate.

Here is a concrete example: many firms discover that clients with less than one million Swiss francs or dollars in assets consume forty percent of service time for only fifteen percent of revenue. This insight does not necessarily mean dropping those clients. Instead, it points to the need for different service tiers or more efficient delivery models for smaller relationships. Serving a niche market with tailored fee models can improve profitability for both the firm and the client segment.

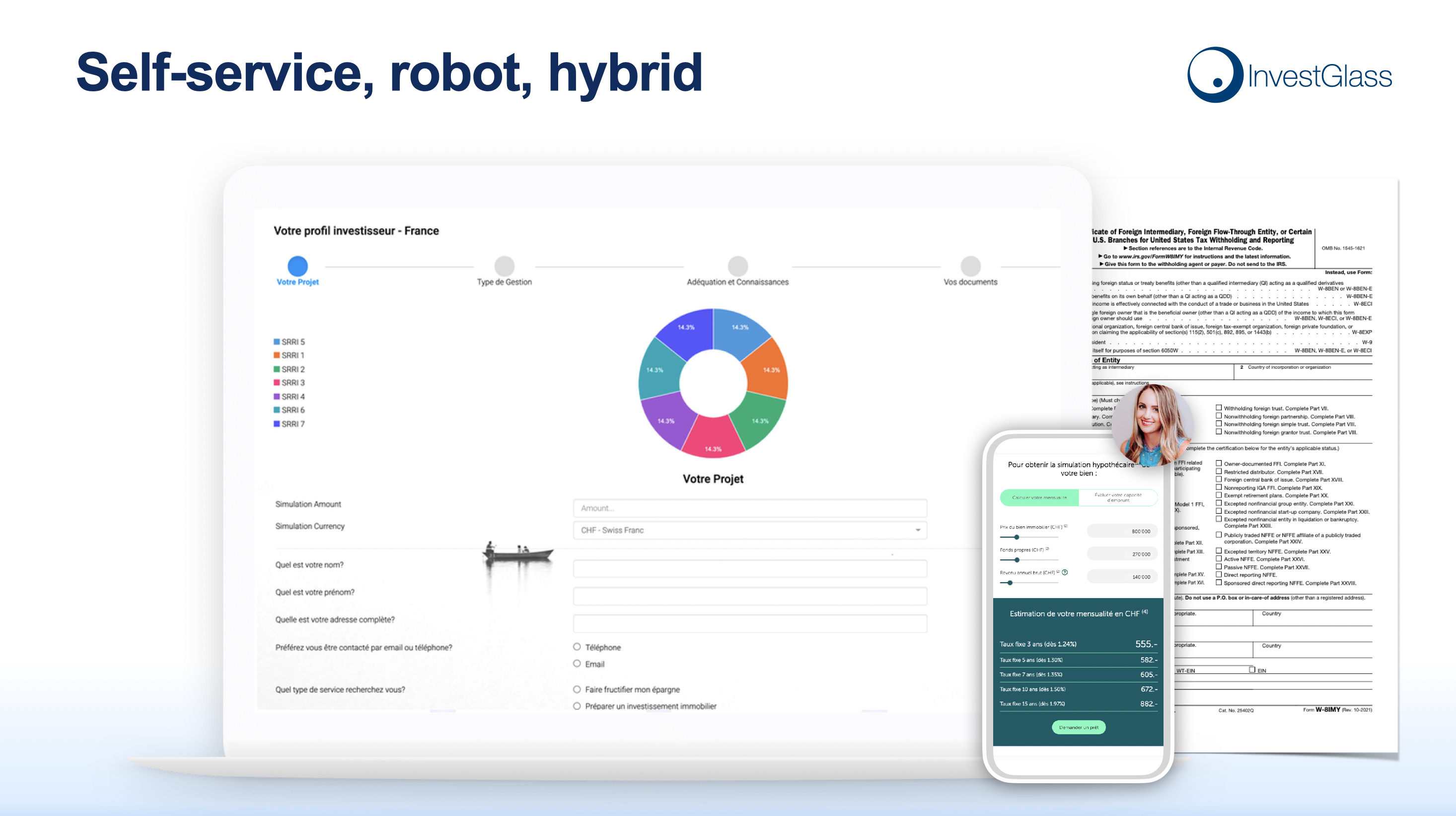

Streamline Digital Onboarding And KYC To Cut Operational Costs

Onboarding and know your client processes are often among the most labour intensive tasks in advisory firms. Every new client relationship begins with gathering personal information, verifying identity, assessing risk tolerance, understanding financial goals, and ensuring compliance with anti money laundering regulations.

Consider a typical manual onboarding workflow from 2020: paper forms mailed or handed to clients, signed documents scanned and emailed back, data manually entered into the CRM, then re entered into the portfolio management system, then again into the custodian’s platform. A compliance officer reviews everything, requests missing documents via email, waits for responses, and eventually clears the account for trading. The entire process could take three to four weeks and involve five or more people.

Contrast this with an automated digital journey in 2025. A digital onboarding tool such as InvestGlass can collect client data once through a secure online form, trigger automated KYC checks against sanctions lists and politically exposed person databases, create client profiles in the CRM, and open custodian accounts without retyping information. Documents can be signed electronically and stored automatically with full audit trails.

Automation can reduce onboarding time from weeks to a few days. More importantly, it frees senior advisors from administrative work so they can focus on revenue generating meetings with potential clients and existing relationships. Instead of chasing signatures and filling forms, your financial planner can spend time on actual financial planning services.

We recommend measuring cost per new client before and after implementation. A realistic target reduction of twenty to thirty percent within the first twelve months is achievable for most firms that fully commit to digital onboarding. Track metrics including total hours spent per client, number of touches required, and time from first advisor meeting to account funded.

Streamlined onboarding and KYC processes also make it easier for firms to adopt alternative fee structures such as a flat fee for financial planning or an annual retainer for ongoing advisory services. By reducing administrative costs and making billing more predictable, firms can help clients avoid sticker shock from large, infrequent charges and provide greater transparency around service costs.

Reduce Technology Spend Through Platform Consolidation

Many firms accumulated overlapping tools between 2015 and 2022. Separate systems for CRM, email marketing, document management, risk profiling, and portfolio reporting seemed like reasonable choices at the time. Each vendor promised best in class functionality in their narrow domain.

The reality today is that multiple systems increase licence fees, integration projects, training requirements, and security risks. When data is hosted in several countries across different platforms, compliance becomes more complex. Your team spends time transferring information between systems rather than serving clients. Every new hire needs training on five or six different platforms before they can be productive.

Consolidating onto an integrated platform such as InvestGlass, hosted in Switzerland or on premise, can replace several distinct subscriptions. A single platform handling CRM, digital onboarding, portfolio management, marketing automation, and client portal functions eliminates the friction of moving data between systems and reduces your total vendor management overhead. Integrated technology also makes it easier for firms to implement fee based, flat fee, or fee for service models by simplifying billing and reporting processes.

To evaluate consolidation opportunities, create a technology inventory that lists:

- Each tool currently in use

- Annual cost including all users and tiers

- Core features actually being used versus features available

- Number of active users

- Data location and sovereignty implications

- Integration dependencies with other systems

Rate each system as keep, replace, or retire. Focus first on retiring tools with significant overlap. A mid sized wealth manager might reduce its monthly software bill by twenty percent by replacing three marketing and CRM tools with one compliant Swiss platform like InvestGlass.

Standardise Investment And Planning Processes To Lower Service Costs

Highly customised portfolios and plans for every client can dramatically increase research, trading, and review work without necessarily improving outcomes. When every client has a unique investment portfolio built security by security, your investment management costs scale linearly with client count.

Creating model portfolios based on risk profiles, tax residence, and investment horizon can reduce portfolio construction time and trading costs. Instead of building each portfolio from scratch, advisors select the appropriate model and make targeted adjustments for specific client circumstances like concentrated stock positions or estate planning considerations.

Consider this approach to asset allocation:

Risk Profile | Equity Allocation | Fixed Income | Alternatives | Cash |

|---|---|---|---|---|

Conservative | 25 percent | 55 percent | 10 percent | 10 percent |

Moderate | 45 percent | 40 percent | 10 percent | 5 percent |

Growth | 65 percent | 25 percent | 8 percent | 2 percent |

Aggressive | 80 percent | 12 percent | 6 percent | 2 percent |

Standardised planning templates for retirement, succession, and corporate liquidity events help junior staff handle more cases with consistent quality. A well designed template ensures nothing important is missed while reducing the time required for each plan. This approach allows your firm to serve many investors with limited staff capacity. Standardisation also enables firms to implement flat fee, annual retainer, or fee-for-service model pricing structures, which are especially effective when targeting a niche market. By streamlining processes, firms can offer transparent and scalable pricing options tailored to specialized client segments.

Portfolio management tools, whether integrated in InvestGlass or connected systems, can rebalance automatically against target models and generate client ready reports in a few clicks. This automation reduces errors and ensures clients receive consistent treatment regardless of which advisor manages their relationship.

Standardisation does not remove personal advice. It moves personalisation to the level of financial goals and strategy rather than individual security selection. Clients still receive tailored recommendations on retirement timing, estate planning, and tax optimisation. What changes is the efficiency of executing those recommendations through standardised investment vehicles like mutual funds and model portfolios.

Automate Compliance And Reporting To Avoid Hidden Costs

Regulatory expectations have increased every year since regulations such as MiFID II in Europe and FinSA in Switzerland took effect. Each new requirement adds work for compliance teams: new forms to collect, new checks to perform, new reports to file. The cumulative burden has made compliance one of the fastest growing cost centers in the wealth management industry.

Many firms still track tasks like suitability checks, cross border restrictions, and document retention with spreadsheets and email reminders. This approach creates risk and consumes staff time. When compliance depends on someone remembering to check a spreadsheet, things inevitably slip through cracks.

Compliance workflows inside a CRM such as InvestGlass can trigger tasks automatically based on client type, jurisdiction, or product category. The system maintains full audit trails without manual logging. When regulators ask for documentation of your compliance process, you can generate reports in minutes rather than days.

Specific examples of automation that save time include:

- Automated alerts when a client profile is missing a risk questionnaire updated during the current year

- Automatic flagging when a politically exposed person requires enhanced due diligence

- System generated reminders for periodic reviews based on client tier and regulatory requirements

- Automated cross border restriction checks before any investment recommendation

- Triggered document requests when client circumstances change

Automated reporting to regulators and internal committees reduces last minute manual work at quarter end. Instead of scrambling to compile data from multiple sources, your compliance team can generate required reports with a few clicks. This efficiency limits the need for additional compliance hires as the client base grows, allowing your firm to scale without proportional increases in compliance cost. By reducing compliance overhead through automation, firms can maintain competitive advisory fees and more easily support a fee based model, ensuring transparency and cost-effectiveness for clients.

Optimise Staffing, Outsourcing, And Use Of AI

Personnel costs usually represent the largest single expense line in advisory firms. Advisor compensation, support staff salaries, employee benefits, and payroll taxes often consume more than half of total operating expenses. This makes staffing optimisation critical for any serious cost reduction effort.

Start by mapping tasks performed by senior advisers, junior advisers, relationship managers, assistants, and operations staff. Identify routine work that could be reassigned to lower cost roles or external providers. Many firms discover that highly paid advisors spend significant time on activities that do not require their expertise or licence.

Consider this task reallocation framework:

Task Category | Current Owner | Optimal Owner | Potential Annual Savings |

|---|---|---|---|

Meeting scheduling | Senior Advisor | Virtual assistant | 100+ hours per advisor |

Data entry and CRM updates | Junior Advisor | Operations staff | 150+ hours per advisor |

Quarterly report preparation | Analyst | Automated system | 200+ hours firm wide |

Document collection | Relationship Manager | Digital onboarding | 300+ hours firm wide |

Optimizing staffing in this way enables firms to offer lower fee services and save money for both the firm and clients, making advisory services more accessible and competitive.

Outsourcing makes sense for specialised tasks that do not require in house expertise. Examples include specialised tax reporting in the United States for clients with American connections, back office reconciliation, or translation of client documents for cross border business. External providers can often deliver these services at lower costs than building internal capabilities.

Modern AI tools can support summarising meeting notes, drafting client emails, and generating first versions of investment commentary. A financial advisor can review and personalise AI drafted content in minutes rather than spending an hour writing from scratch. By focusing staff on activities that deliver the most client value, firms improve both efficiency and client satisfaction. Human advisers retain responsibility for final review, ensuring good advice still carries the personal touch clients expect.

Firms should set clear policies on AI usage. Data processed through secure platforms such as InvestGlass AI modules hosted in Switzerland maintains client confidentiality while enabling productivity gains. This approach lets you save time without compromising the data sovereignty that regulated institutions require.

Enhance Client Self Service To Lower Financial Advisor Fees

Digital client portals can transfer routine information requests from staff to secure online interfaces available twenty four hours a day. When clients can answer their own questions about account balances, recent transactions, or tax documents, your team spends less time on phone calls and emails that do not generate revenue.

Features clients value in self service portals include:

- Viewing performance with interactive charts showing portfolio growth over time

- Downloading statements, tax documents, and contract copies

- Signing documents electronically without printing or mailing

- Sending secure messages instead of using regular email

- Updating personal information and preferences

- Scheduling meetings with their advisor

These features help clients save money by reducing the need for manual support and focusing on delivering client value, as clients can access the services they value most such as time savings and immediate access to information without incurring additional advisory fees.

When clients can access answers themselves, call volumes and email backlogs fall. Firms report twenty to forty percent reductions in routine client inquiries after implementing comprehensive portals. This reduction means your support team can handle a larger client base without proportional staffing increases.

Client segmentation ensures appropriate service levels across your book. Very high net worth individuals may still expect white glove treatment with immediate phone access to their advisor. Mass affluent clients benefit equally from digital channels that provide faster responses than waiting for a callback. Both segments receive most value from the approach that matches their preferences.

InvestGlass offers branded client portals where firms maintain control of data sovereignty within Switzerland or on their own servers. This combination of self service convenience and Swiss data protection addresses both cost reduction and compliance requirements simultaneously.

Measure Results And Build A Continuous Cost Discipline

One time cuts are less effective than ongoing measurement and small adjustments over several years. Firms that treat cost optimisation as a project rather than a discipline often see expenses creep back up within two to three years as new tools accumulate and processes become less efficient over time.

Key metrics to track for ongoing cost management include:

Metric | Definition | Target Direction |

|---|---|---|

Operating margin | Net income divided by revenue | Increase over time |

Cost per client | Total operating costs divided by client count | Decrease or stable |

Revenue per employee | Total revenue divided by headcount | Increase over time |

Onboarding time | Days from first meeting to funded account | Decrease |

Technology cost per advisor | Annual software spend divided by advisor count | Decrease or stable |

Compliance hours per client | Hours spent on regulatory tasks per relationship | Decrease |

Advisory fees | Total fees charged to clients for advisory services | Decrease or stable |

Regularly tracking advisory fees and reviewing fee calculation methods such as flat fees, tiered fees, hourly rates, or project-based fees helps ensure your pricing remains competitive and aligned with the value provided, supporting ongoing cost management.

Set explicit targets tied to specific timeframes. For example: reduce average onboarding time by thirty percent and technology spending per adviser by fifteen percent between January 2025 and December 2026. These concrete goals create accountability and allow progress tracking.

Involve advisers, operations, and compliance teams in regular reviews. The people doing the work often have the best ideas for improving efficiency. They can also flag when cost measures unintentionally damage client experience or create compliance risks. Monthly or quarterly reviews keep cost discipline visible without becoming burdensome.

Treat cost optimisation as part of your firm’s culture. Use platforms such as InvestGlass to continually refine workflows as regulations and client expectations change. The firms that build efficient operations as a core capability will outperform those that cut costs only when forced by market conditions.

How InvestGlass Helps Advisory Firms Reduce Costs

InvestGlass is a Swiss sovereign CRM and automation platform purpose built for regulated financial institutions. Unlike generic business software adapted for financial services, InvestGlass was designed from the ground up for banks, wealth managers, and advisory firms operating under strict regulatory requirements.

The platform combines digital onboarding, KYC, portfolio management, marketing automation, and a client portal in one integrated environment. This consolidation eliminates the need for multiple point solutions that create data silos and integration headaches.

Hosting data in Switzerland or on the client firm’s own servers addresses data sovereignty concerns that matter increasingly to regulators and clients alike. This approach can reduce the overhead linked to multi country cloud solutions where data governance becomes complex and compliance validation difficult.

Practical cost savings available through InvestGlass include:

- Removing several separate subscriptions for CRM, email campaigns, document signing, and basic portfolio reporting

- Eliminating manual data transfer between disconnected systems

- Reducing compliance risk through automated workflows and audit trails

- Accelerating onboarding from weeks to days with digital document collection and electronic signatures

- Lowering training costs by having staff learn one integrated system rather than five separate tools

InvestGlass also supports a wide range of fee models and fee structures, including flat fees, tiered fees, AUM-based fees, and subscription-based models. This flexibility makes it easier for firms to manage advisory fees and charging fees efficiently, ensuring billing aligns with client needs and regulatory requirements.

Consider starting with a pilot project where one team or office migrates to InvestGlass. Measure time spent on onboarding, compliance, and client communication before and after the transition. This controlled approach lets you validate savings before committing to a full firm rollout.

The pay structure for InvestGlass scales with your firm’s needs, allowing you to start with core functionality and expand as you realise benefits. This flexibility means smaller firms can access enterprise grade capabilities without enterprise grade pricing.

FAQ

What is a realistic timeframe to see cost savings after adopting an integrated platform?

Firms usually see visible time savings in onboarding and reporting within three to six months once staff are trained and core processes are mapped into the new system. Adopting a new fee structure or fee models such as flat fees, tiered fees, or subscription-based models can also influence how quickly cost savings are realized, as these changes may streamline billing and reduce administrative overhead. The initial period involves learning curves and workflow adjustments that temporarily reduce productivity gains.

Deeper reductions in overall operating costs often appear within twelve to eighteen months as duplicate tools are retired and new workflows become standard practice. The full financial impact depends on how completely firms commit to retiring legacy systems and adopting new processes rather than running parallel approaches.

Can small advisory firms with fewer than ten employees benefit from these measures?

Small firms often benefit even more from automation because partners currently handle both advisory and administrative work. When a founding advisor spends twenty hours monthly on paperwork that automation could eliminate, those hours immediately become available for client relationship building or business development.

In addition, small firms can benefit from adopting alternative fee models such as flat fee, hourly fees, or a fee-for-service model, especially when targeting a niche market. These flexible pricing structures can help attract specific client segments, improve transparency, and align services with the unique needs of their chosen niche.

Such firms should start with a narrow project rather than attempting complete transformation. Digital onboarding and client portal rollout provide quick wins that demonstrate value before tackling full process redesign. The focus should be on changes that free advisor time for activities that generate revenue.

How can firms reduce costs without harming client relationships?

Most recommended changes focus on back office efficiency, standardisation, and better use of technology rather than cutting client contact. In fact, many improvements enhance client experience by providing faster responses, easier document access, and more consistent service.

Communicate improvements openly with clients. Explaining that a new portal or digital signature process will allow faster responses and clearer reporting positions changes as service enhancements rather than cost cutting. Clients generally appreciate innovations that make their interactions with your firm more convenient, especially when those changes come with a fair price for services rendered. Additionally, maintaining transparent advisory fees, adopting a fee based model, and focusing on delivering client value can help strengthen client relationships while reducing costs.

What are the main risks when implementing cost reduction programmes?

Rushed cuts to experienced staff or compliance resources can increase regulatory and reputational risk significantly. Firms that reduce headcount without first automating the work those people performed often find themselves overwhelmed or facing compliance failures.

Recommend phased implementation with clear documentation and regular feedback from advisers and clients. Watch for early warning signs like increased client complaints, longer response times, or compliance near misses. These indicators suggest the firm is cutting too fast or in the wrong areas. Additionally, be mindful of the risk of sticker shock if clients are not adequately informed about changes in fee structure or billing practices, as unexpected or infrequent large fees can negatively impact client satisfaction.

How important is data sovereignty when selecting tools to reduce costs?

For banks and wealth managers subject to strict privacy rules, choosing platforms with clear data residency is essential. Swiss hosted solutions like InvestGlass provide assurance about where client data lives and which legal frameworks govern its protection.

Ignoring data sovereignty can lead to fines, forced migrations, or client mistrust. A compliance violation that triggers remediation costs and reputational damage will ultimately increase total cost rather than reducing it. The buy in from compliance and legal teams is essential before selecting any new technology platform, regardless of promised cost savings.

Related articles

Swiss Sovereign CRM: Built on AI.

Ready to act.