ChatGPT affects banking by bringing advanced ai into core banking work, changing how financial institutions handle fraud detection, customer service automation, personalized financial advice, and credit risk assessment. The banking industry is experiencing its most profound transformation since the advent of digital banking, with artificial intelligence reshaping every facet of financial services. Technological innovation is a driving force behind this transformation, enabling banking industries to adapt to rapid change and integrate advanced AI solutions. From fraud detection systems that process millions of transactions in milliseconds to personalized financial advice delivered through virtual assistants, ai systems are fundamentally changing how banks operate and serve customers.

This transformation isn’t happening gradually it’s accelerating at breakneck speed. In 2025, ai technologies have moved from experimental pilots to mission-critical infrastructure across financial institutions worldwide. For banking professionals, financial institutions, technology decision-makers, and other stakeholders tracking the future of financial services, the shift is now tied directly to competitiveness, efficiency, risk control, and customer growth. The impact spans every aspect of banking operations, from customer-facing applications to back-office processes that drive operational efficiency.

يتطلب فهم كيفية تأثير الذكاء الاصطناعي على الخدمات المصرفية دراسة كل من التغييرات الفورية التي تعيد تشكيل العمليات اليومية والتحولات الاستراتيجية طويلة الأجل التي ستحدد مستقبل الخدمات المالية. ولكي تظل البنوك قادرة على المنافسة، يجب على البنوك مواءمة تبني الذكاء الاصطناعي مع استراتيجية عمل واضحة تدعم الابتكار والكفاءة التشغيلية والتركيز على العملاء في المشهد المالي المتطور. يستكشف هذا التحليل الشامل الوضع الحالي ل الذكاء الاصطناعي في الأعمال المصرفية, changes in customer experience, operational efficiency, risk management, regulatory and compliance challenges, investment trends, best practices for adoption, and the emerging technologies shaping banking’s future.

مقدمة في الذكاء الاصطناعي في الأعمال المصرفية

الذكاء الاصطناعي (AI) is your gateway to redefining your banking operations and delivering the exceptional experiences your clients demand. When you embrace AI technologies, you’re not just staying competitive you’re positioning your institution to thrive and scale faster in today’s rapidly evolving financial landscape. By integrating advanced AI systems into your core banking operations, you can automate those time-consuming routine tasks like fraud detection and credit risk assessment, freeing up your teams to focus on what truly matters: building valuable client relationships and driving growth.

Your adoption of artificial intelligence isn’t just about automation it’s about transforming how you connect with clients and manage risk. With AI models analyzing vast amounts of customer behavior data, you can deliver personalized financial advice and tailored solutions that truly meet individual needs. This level of personalization doesn’t just enhance client satisfaction; it builds the long-term loyalty that keeps your institution ahead of the competition.

علاوةً على ذلك، تساعدك الابتكارات القائمة على الذكاء الاصطناعي على البقاء في المقدمة من خلال تبسيط العمليات وخفض التكاليف التشغيلية ودعم استراتيجيات النمو المستدام. ومع ازدياد تطور أدوات الذكاء الاصطناعي، يمكنك الاستفادة من هذه التقنيات لاكتساب رؤى أعمق حول احتياجات العملاء، وتحسين عملية اتخاذ القرارات، وخلق فرص جديدة لتوسيع نطاق أعمالك. إن تكامل الذكاء الاصطناعي into your banking operations is no longer optional it’s your strategic advantage for thriving in the digital age and delivering exceptional client experiences.

التأثير الفوري: كيف يعيد الذكاء الاصطناعي تشكيل العمليات المصرفية اليوم

لقد وصل تبني القطاع المصرفي للذكاء الاصطناعي إلى مستويات غير مسبوقة، حيث استثمرت المؤسسات المالية $21 مليار دولار أمريكي على وجه التحديد في تقنيات الذكاء الاصطناعي خلال عام 2023. ويعكس هذا الاستثمار الضخم زيادة في معدل التبني بمقدار 78% عن العام السابق عبر المؤسسات المالية، مما يدل على أن تبني الذكاء الاصطناعي قد انتقل من المرحلة التجريبية إلى الضرورة الاستراتيجية.

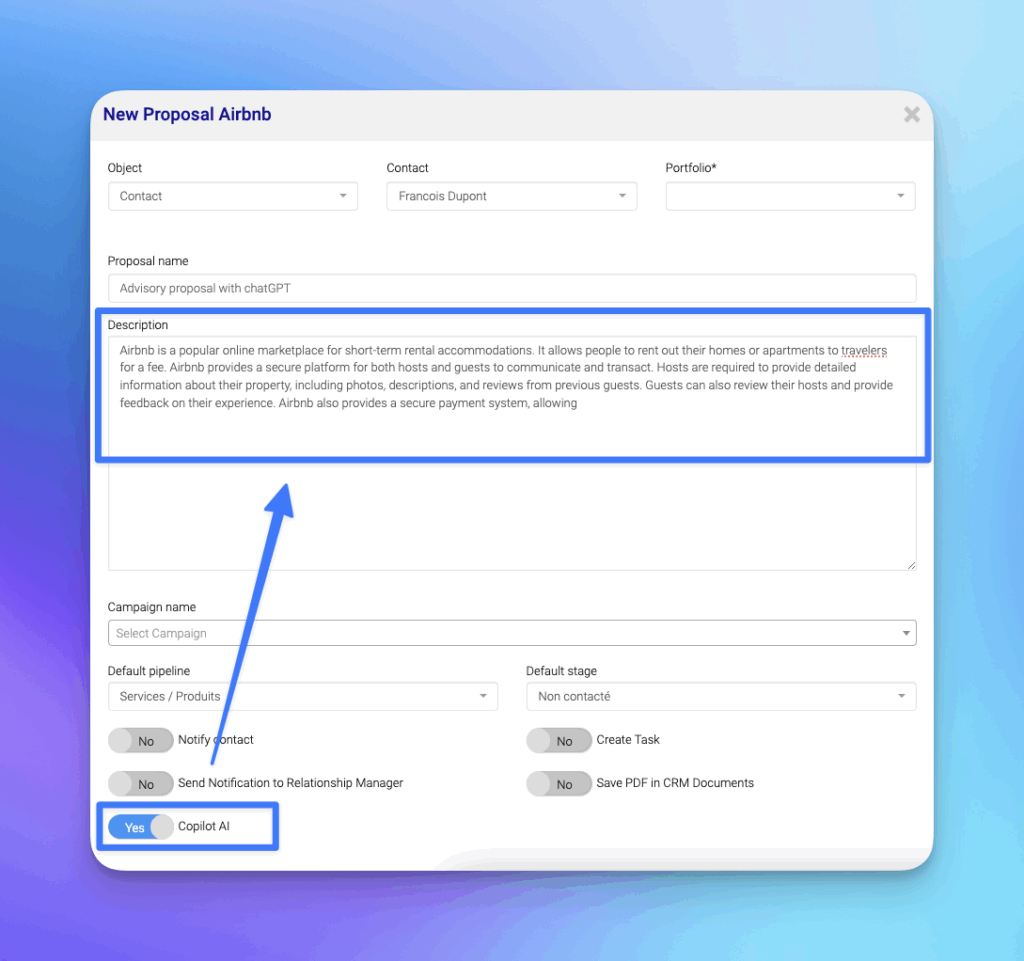

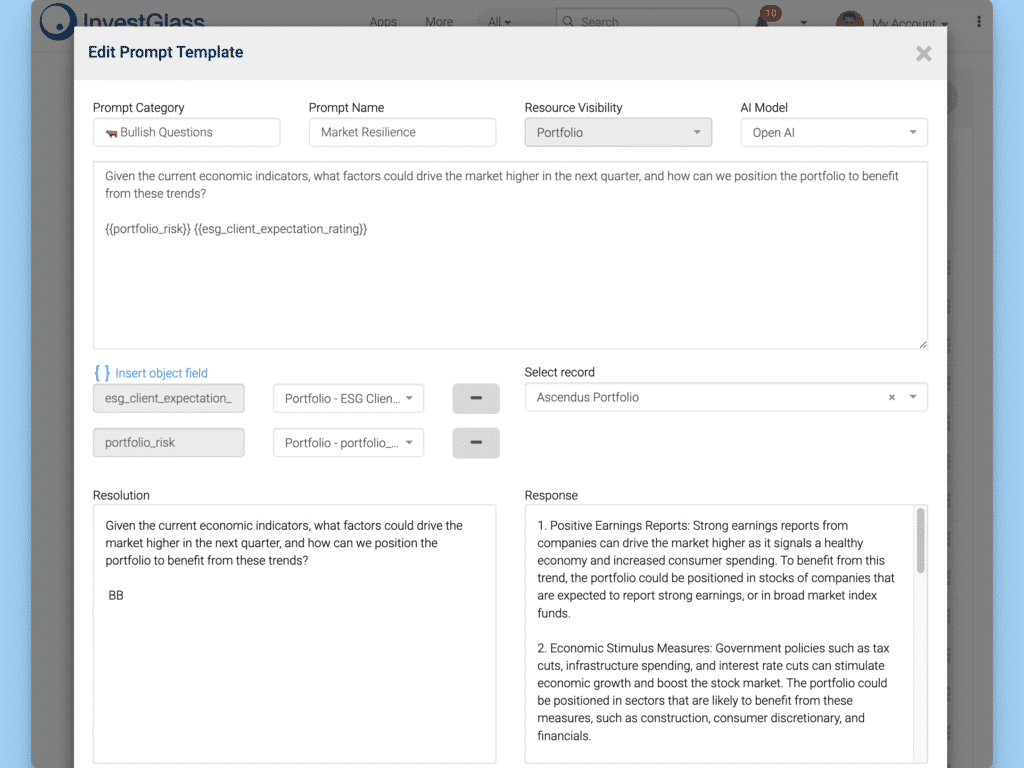

تكامل ChatGPT مع InvestGlass لمساعدة البنوك والمستشارين

The integration of AI technologies in financial institutions is driving a shift toward ai driven solutions that modernize traditional banking operations. These solutions streamline manual processes, improve decision-making, and, with emerging agentic AI in banking, help banks stay competitive in a rapidly evolving landscape.

يمثل الكشف عن الاحتيال في الوقت الحقيقي أحد أكثر التطبيقات وضوحًا حيث يؤثر الذكاء الاصطناعي على العمليات المصرفية بشكل فوري. تقوم نماذج الذكاء الاصطناعي المتقدمة بتحليل أنماط المعاملات وسلوك المستخدم ومؤشرات المخاطر لتحديد النشاط المشبوه في غضون أجزاء من الثانية. وقد حققت هذه الأنظمة نتائج رائعة، حيث قللت من خسائر الاحتيال بنسبة تصل إلى 401 تيرابايت إلى 3 تيرابايت مقارنةً بالطرق التقليدية مع تحسين تجربة العملاء في الوقت نفسه من خلال تقليل النتائج الإيجابية الخاطئة التي كانت تحجب المعاملات المشروعة في السابق.

يمتد التحول إلى خدمة العملاء من خلال روبوتات الدردشة الآلية والمساعدين الافتراضيين المدعومين بالذكاء الاصطناعي على مدار الساعة طوال أيام الأسبوع، والتي تتعامل مع الاستفسارات الروتينية دون تدخل بشري. تقوم أدوات الذكاء الاصطناعي هذه بمعالجة استفسارات اللغة الطبيعية، والوصول إلى بيانات العملاء في الوقت الفعلي، وتقديم ردود مخصصة بناءً على تاريخ الحساب الفردي وتفضيلاته. تشير البنوك الكبرى إلى أن هذه الأنظمة تتعامل الآن مع أكثر من 801 تيرابايت من تفاعلات خدمة العملاء الأساسية، مما يحرر الوكلاء البشريين للتركيز على المشكلات المعقدة التي تتطلب التعاطف وحل المشكلات المعقدة. ومن خلال أتمتة المهام المتكررة مثل الإجابة على الأسئلة المتداولة ومعالجة الطلبات البسيطة، يستطيع الموظفون التركيز على الأنشطة ذات القيمة الأعلى التي تؤدي إلى رضا العملاء ونمو الأعمال.

ولعل الأهم من ذلك كله، هو تسجيل الائتمان الآلي والقرض عمليات الموافقة have revolutionized lending operations. ai algorithms analyze structured and unstructured data from multiple sources including traditional credit reports, bank transaction history, social media activity, and alternative data sources to make credit risk assessments. This comprehensive analysis cuts decision time from days to minutes, and some ChatGPT-assisted internal tasks that once took 12-15 minutes can now be completed in just a few seconds, helping to enhance efficiency in lending operations while improving accuracy in predicting repayment probability.

لقد مكّن دمج نماذج التعلم الآلي في تقييم مخاطر الائتمان البنوك من توسيع نطاق الوصول إلى الائتمان للفئات السكانية التي كانت محرومة من الخدمات في السابق. ومن خلال النظر في مجموعات البيانات الأوسع نطاقًا وتحديد الأنماط التي قد يغفلها المكتتبون البشريون، يمكن لأنظمة الذكاء الاصطناعي تحديد المقترضين الجديرين بالائتمان الذين يفتقرون إلى التاريخ الائتماني التقليدي، مما يدعم الشمول المالي مع الحفاظ على معايير إدارة المخاطر.

ثورة تجربة العملاء من خلال تقنيات الذكاء الاصطناعي

The way customers interact with their banks has been completely transformed through ai capabilities, creating more personalized and efficient services that adapt to individual needs and preferences in real-time. AI enables banks to deliver personalized services by leveraging advanced data analysis and machine learning to tailor offerings, communications, and support to each customer’s unique financial situation. Modern banking apps powered by ai technologies analyze spending patterns, financial goals, and behavioral data to provide hyper-personalized recommendations that help customers make better financial decisions.

وقد قامت مؤسسات مالية رائدة مثل JPMorgan Chase بتطبيق منصات تعتمد على الذكاء الاصطناعي تقدم مشورة مالية مخصصة بناءً على تحليل شامل لسلوك العملاء وظروف السوق. يمكن لمساعدهم الافتراضي تحليل أنماط الإنفاق، واقتراح تحسينات في الميزانية، والتوصية بفرص استثمارية مصممة خصيصًا لملفات المخاطر الفردية والأهداف المالية.

Bank of America’s Erica virtual assistant exemplifies how ai tools have revolutionized customer interactions. This ai agent handles millions of customer requests monthly, from basic account inquiries to complex financial planning assistance. This kind of conversational banking helps customers feel understood and supported, which matters because 79% of customers expect brands to demonstrate understanding and care, especially from a trusted financial brand. Erica can predict customer needs based on transaction history, proactively alert users to unusual spending patterns, and provide insights that help customers achieve their financial goals.

As part of broader banking technology, these interfaces show how conversational banking extends beyond simple voice commands into more natural customer interactions. Customers can check account balances, transfer funds, pay bills, and receive financial insights using natural language voice commands. This technology integrates seamlessly with existing smart home ecosystems, making banking services accessible through familiar interfaces that customers already use daily.

Conversational AI also supports digital onboarding and compliance documentation.

مراقبة المعاملات في الوقت الفعلي يمثل تقدمًا حاسمًا في حماية العملاء وتجربتهم. تقوم خوارزميات الذكاء الاصطناعي بتحليل أنماط المعاملات باستمرار لتحديد الأنشطة الاحتيالية المحتملة وتنبيه العملاء على الفور من خلال الإشعارات الفورية أو الرسائل النصية أو البريد الإلكتروني. هذا النهج الاستباقي لا يمنع الخسائر المالية فحسب، بل يعزز الثقة من خلال إظهار التزام البنك بأمن العملاء.

ai-driven wealth management platforms have democratized access to sophisticated investment advice previously available only to high-net-worth individuals. Robo-advisory services use advanced ai models to create and manage diversified investment portfolios based on individual risk tolerance, time horizons, and financial objectives. These platforms provide continuous إدارة المحافظ الاستثمارية القائمة على الذكاء الاصطناعي, automatic rebalancing, and tax-loss harvesting, delivering professional-grade wealth management at a fraction of traditional costs.

The personalization extends beyond investment advice to include customized product recommendations. ai systems analyze customer data to identify life events, changing financial needs, and opportunities for additional services. When a customer’s spending patterns suggest they’re planning a major purchase, the system can proactively offer relevant financing options or savings strategies, with financial education helping customers act on those recommendations confidently.

موجه العميل الذكي "إنفست جلاس

تعزيز الكفاءة التشغيلية وإدارة المخاطر التشغيلية

Behind the scenes, ai technologies are driving unprecedented improvements in efficient services, risk management, and banking operations. مراقبة الامتثال الآلي برزت كتطبيق بالغ الأهمية، مما يقلل من الانتهاكات التنظيمية بنسبة 60% من خلال المراقبة المستمرة للمعاملات والاتصالات والعمليات التجارية مقابل المتطلبات التنظيمية المعقدة. تعد استراتيجيات الذكاء الاصطناعي الفعالة الآن ضرورية للامتثال التنظيمي وإدارة المخاطر، مما يضمن قدرة البنوك على التكيف مع اللوائح المتطورة والاتجاهات المستقبلية.

ai-powered document processing has eliminated manual data entry tasks that previously consumed thousands of hours of human labor. Natural language processing systems can extract relevant information from contracts, loan applications, regulatory filings, and other documents with greater accuracy and speed than human processors. This automation not only reduces costs but also minimizes errors that could lead to compliance issues or customer dissatisfaction. By automating these processes, banks reduce manual work for bank employees so teams can focus on higher-value tasks that drive growth and competitiveness.

Predictive analytics for market trends and investment opportunities represent another area where ai capabilities provide significant competitive advantages. ai models analyze vast amounts of market data, economic indicators, news sentiment, and historical patterns to identify trends and opportunities that human analysts might miss. These insights inform trading strategies, risk management decisions, and product development initiatives, and they are increasingly embedded in generative ai tools used across modern banking technology. AI also enhances a bank’s ability to monitor compliance and manage risk more effectively, improving risk mitigation and overall إدارة المحافظ الاستثمارية المدعومة بالذكاء الاصطناعي. These advanced capabilities provide a competitive advantage for banks, enabling them to stay ahead of industry trends and outperform their rivals.

لقد أحدثت خوارزميات التعلّم الآلي ثورة في مجال الكشف عن مكافحة غسيل الأموال (AML) من خلال تحديد الأنماط المشبوهة عبر شبكات معقدة من المعاملات والعلاقات. وغالبًا ما كانت الأنظمة التقليدية القائمة على القواعد تولد العديد من النتائج الإيجابية الخاطئة التي تتطلب مراجعة يدوية، في حين أن الأنظمة القائمة على الذكاء الاصطناعي يمكنها التمييز بين المعاملات المعقدة المشروعة وأنشطة غسل الأموال الفعلية بدقة أكبر بكثير.

لقد أدت إمكانات إعداد التقارير التنظيمية المؤتمتة واختبار الإجهاد إلى تبسيط عمليات الامتثال التي كانت تتطلب في السابق جهدًا يدويًا كبيرًا، حيث يمكن لأنظمة الذكاء الاصطناعي إنشاء التقارير المطلوبة من خلال تجميع البيانات من مصادر متعددة، مما يضمن الدقة والاتساق مع الالتزام بالمواعيد النهائية التنظيمية الضيقة. يمكن لنماذج اختبار الإجهاد المدعومة بالتعلم الآلي محاكاة الآلاف من سيناريوهات السوق لتقييم مرونة المحفظة في ظل الظروف الاقتصادية المختلفة.

يمتد دمج أدوات الذكاء الاصطناعي في إدارة المخاطر إلى الائتمان إدارة المحفظة, where predictive models continuously assess the likelihood of default across entire loan portfolios. These systems can identify early warning signs of borrower distress and recommend proactive interventions to minimize losses while supporting customer retention. In some banking use cases, generative AI can improve risk assessment efficiency by 27–35%.

اكتشاف الاحتيال والتقدم في مجال الأمن السيبراني

يمثل تطور الكشف عن الاحتيال من خلال الذكاء الاصطناعي أحد أكثر عمليات الكشف عن الاحتيال تطوراً تطبيقات الذكاء الاصطناعي in the banking sector. Modern ai systems analyze transaction behavior in real-time, identifying suspicious patterns within milliseconds of transaction initiation. These systems consider hundreds of variables simultaneously including transaction amount, merchant type, geographic location, time of day, and historical spending patterns to calculate risk scores with remarkable precision.

Behavioral biometric authentication has emerged as a powerful replacement for traditional password-based security systems. ai algorithms learn individual typing patterns, mouse movements, touch screen interactions, and other behavioral characteristics to create unique biometric profiles. This technology, combined with التحقق الآلي من معرفة عميلك, can detect account takeover attempts even when criminals have obtained legitimate login credentials, providing an additional layer of security that’s nearly impossible to replicate.

تحمي أنظمة الكشف عن التهديدات التي يحركها الذكاء الاصطناعي البنية التحتية المصرفية من خلال تحليل حركة مرور الشبكة وسجلات النظام وسلوك المستخدم لتحديد الهجمات الإلكترونية المحتملة قبل أن تتسبب في أضرار. وتستخدم هذه الأنظمة التعلم الآلي لتحديد أنماط السلوك العادي الأساسية والإبلاغ عن الحالات الشاذة التي قد تشير إلى نشاط ضار. يُمكِّن هذا النهج الاستباقي فرق الأمن من الاستجابة للتهديدات قبل أن تتفاقم وتتحول إلى اختراقات خطيرة.

وقد أدى تبادل البيانات بين المؤسسات من أجل تعزيز شبكات منع الاحتيال إلى إنشاء أنظمة دفاعية تعاونية تتشارك فيها البنوك مؤشرات الاحتيال مجهولة المصدر لحماية النظام المالي بأكمله. تقوم أنظمة الذكاء الاصطناعي بتحليل الأنماط عبر مؤسسات متعددة لتحديد مخططات الاحتيال الناشئة وتحديث التدابير الدفاعية في الوقت الفعلي عبر المؤسسات المشاركة.

اتخاذ القرارات باستخدام الذكاء الاصطناعي

AI is revolutionizing decision-making in banking, giving financial institutions the power to make smarter, faster, and more profitable decisions than ever before. With cutting-edge AI models at your fingertips, banks can unlock massive volumes of customer data, market trends, and economic indicators to drive real-time decision making across every corner of their operations. This isn’t just about technology it’s about empowering your institution with the insights that separate industry leaders from the competition.

يعني هذا التحول المستند إلى البيانات أن مصرفك يمكنه التمحور على الفور عندما تتغير الأسواق، وتقليل التعرض للمخاطر، واقتناص الفرص المربحة لحظة ظهورها. تهتم الأتمتة المدعومة بالذكاء الاصطناعي بالقرارات الروتينية تلقائيًا، مما يحرر فرقك القيّمة لمعالجة التحديات الاستراتيجية المعقدة التي تحقق قيمة حقيقية للأعمال. والنتيجة؟ مكاسب هائلة في الكفاءة وتخصيص أكثر ذكاءً للموارد، مما يضع منافسيك في مرآة الرؤية الخلفية.

AI-driven predictive analytics are your crystal ball for spotting risks and opportunities before they hit your bottom line. By continuously scanning customer behaviors and market signals, AI systems help you stay three steps ahead adjusting strategies proactively and driving sustainable growth that builds lasting value. When you make informed, data-backed decisions, you’re not just improving your competitive edge you’re securing your institution’s financial future.

In today’s lightning-fast finance sector, AI-powered decision making isn’t optional it’s essential. Banks that harness this technology don’t just survive; they deliver exceptional customer experiences and achieve the kind of sustainable growth that transforms good institutions into industry titans. The question isn’t whether you can afford to invest in AI it’s whether you can afford not to.

التحديات الحرجة وإدارة المخاطر في الخدمات المصرفية القائمة على الذكاء الاصطناعي

في حين أن الذكاء الاصطناعي يوفر فرصاً هائلة للقطاع المصرفي، إلا أنه يطرح أيضاً تحديات كبيرة يجب على المؤسسات المالية إدارتها بعناية لضمان نشر الذكاء الاصطناعي بشكل مسؤول. ويمثل التحيز الخوارزمي الذي يؤثر على الموافقات على القروض والقرارات الائتمانية أحد أخطر المخاوف، حيث إن نماذج الذكاء الاصطناعي المدربة على البيانات التاريخية قد تديم أو تضخم الممارسات التمييزية القائمة.

Data privacy concerns with customer information processing have become increasingly complex as ai systems require access to vast amounts of personal and financial data to function effectively. Banks must balance the need for comprehensive data analysis with customer privacy expectations, data security, and regulatory requirements for data protection. The challenge is particularly acute given the sensitive nature of financial information and the potential consequences of data breaches.

Black box decision-making creates transparency issues that can undermine customer trust and regulatory compliance. Many ai models, particularly deep learning systems, operate in ways that are difficult to explain or interpret. ChatGPT may also struggle with understanding financial terminology, which can affect accuracy in sensitive banking contexts. When an ai system denies a loan application or flags a transaction as suspicious, customers and regulators may demand explanations that the technology cannot easily provide.

Regulatory compliance challenges across different jurisdictions add complexity to ai implementation, as banks operating internationally must navigate varying requirements for ai governance, data protection, and algorithmic transparency. These challenges also impact financial firms more broadly, as implementing ai tools requires alignment with financial regulations, and ai models must comply with federal regulations to avoid bias. The rapidly evolving regulatory landscape means that compliance frameworks must be continuously updated to address new requirements and guidance.

تخلق ثغرات الأمن السيبراني في أنظمة الذكاء الاصطناعي نواقل هجوم جديدة قد تستغلها الجهات الخبيثة، حيث يمكن التلاعب بنماذج الذكاء الاصطناعي من خلال هجمات عدائية تجعلها تتخذ قرارات غير صحيحة، كما أن الطبيعة المركزية للعديد من أنظمة الذكاء الاصطناعي تخلق أهدافًا عالية القيمة لمجرمي الإنترنت. يجب على البنوك تنفيذ تدابير أمنية قوية مصممة خصيصًا لحماية البنية التحتية للذكاء الاصطناعي مع الحفاظ على أداء النظام وتوافره.

تتطلب مخاوف الإزاحة الوظيفية بالنسبة للأدوار المصرفية التقليدية إدارة التغيير بعناية حيث تعمل أنظمة الذكاء الاصطناعي على أتمتة المهام التي كان يؤديها الموظفون البشريون في السابق. في حين أن الذكاء الاصطناعي غالبًا ما يعزز القدرات البشرية بدلاً من أن يحل محلها، إلا أن بعض الأدوار قد تصبح متقادمة، مما يخلق تحديات لتخطيط القوى العاملة وإعادة التدريب والحفاظ على معنويات الموظفين خلال فترات التحول.

الإطار التنظيمي ومتطلبات الامتثال

تتطور البيئة التنظيمية للذكاء الاصطناعي في القطاع المصرفي بسرعة، مع ظهور أطر عمل جديدة لمواجهة التحديات الفريدة التي تفرضها أنظمة الذكاء الاصطناعي. تضع متطلبات تنفيذ قانون الاتحاد الأوروبي للذكاء الاصطناعي للمؤسسات المالية قواعد شاملة لتطوير أنظمة الذكاء الاصطناعي ونشرها ومراقبتها. يجب على البنوك العاملة في أوروبا التأكد من أن أنظمة الذكاء الاصطناعي الخاصة بها تفي بالمتطلبات الصارمة لتقييم المخاطر والتوثيق والإشراف البشري. ويُعد دمج الذكاء الاصطناعي في أطر الامتثال أمرًا ضروريًا للبنوك لتلبية هذه المتطلبات التنظيمية بفعالية وتبسيط العمليات وتعزيز إدارة المخاطر.

تشدد المبادئ التوجيهية للأمر التنفيذي الأمريكي الخاص بالذكاء الاصطناعي في القطاع المصرفي على الحاجة إلى تطوير الذكاء الاصطناعي المسؤول مع الحفاظ على زخم الابتكار. تتطلب هذه المبادئ التوجيهية من البنوك تقييم تأثيرات نظام الذكاء الاصطناعي على العدالة والسلامة والفعالية مع تنفيذ هياكل الحوكمة المناسبة للإشراف على نشر الذكاء الاصطناعي وتشغيله.

تتطلب معايير التوثيق وقابلية التدقيق في عملية اتخاذ القرارات المتعلقة بالذكاء الاصطناعي أن تحتفظ البنوك بسجلات شاملة لكيفية اتخاذ أنظمة الذكاء الاصطناعي للقرارات، بما في ذلك مصادر بيانات التدريب وبنى النماذج وإجراءات التحقق من الصحة ومراقبة الأداء المستمرة. يجب أن تكون هذه الوثائق كافية لتمكين الفحص والتدقيق التنظيمي مع دعم عمليات الحوكمة الداخلية.

تُلزم تدابير حماية المستهلك ومتطلبات الذكاء الاصطناعي القابلة للتفسير البنوك بتقديم تفسيرات واضحة للقرارات التي يتخذها الذكاء الاصطناعي والتي تؤثر على العملاء. عندما يرفض نظام الذكاء الاصطناعي الائتمان أو يضع علامة على معاملة، يحق للعملاء فهم الأسباب الكامنة وراء القرار وطلب مراجعة بشرية للنتيجة.

اتجاهات الاستثمار ونمو السوق في الخدمات المصرفية القائمة على الذكاء الاصطناعي

The financial commitment to ai technologies across the banking sector reflects the strategic importance of these innovations for competitive positioning and operational excellence. Total ai investment in financial services reached $35 billion during 2023, with major banks allocating 15-20% of their entire IT budgets specifically to ai initiatives. This level of investment demonstrates that ai adoption has moved beyond experimental projects to become a core component of digital transformation strategies, a view reinforced by the 66% of banking executives who believe new technologies will drive banking over the next five years.

Financial institutions are increasingly forming strategic partnerships with fintech companies to accelerate ai innovation and access specialized expertise. These collaborations enable traditional banks to leverage cutting-edge ai capabilities developed by technology-focused startups while providing fintechs with access to established customer bases and regulatory expertise. The partnership model has proven particularly effective for deploying generative ai applications, including developing digital advisors, and new customer-facing ai services.

إن العوائد المتوقعة على استثمارات الذكاء الاصطناعي كبيرة، حيث تشير التوقعات إلى أن الخدمات المالية التي تعمل بالذكاء الاصطناعي يمكن أن تساهم بمبلغ $2 تريليون دولار في الاقتصاد العالمي من خلال تحسين الكفاءة وتوسيع نطاق الوصول إلى الخدمات المالية وتعزيز قدرات إدارة المخاطر. وتشير توقعات عائدات الاستثمار في البنوك الفردية إلى أن عائدات الاستثمار في استثمارات الذكاء الاصطناعي تبلغ 3001 تريليون تيرابايت في غضون 3 سنوات، مدفوعة في المقام الأول بتخفيض التكاليف التشغيلية وتحسين إدارة المخاطر وتعزيز اكتساب العملاء والاحتفاظ بهم.

The investment landscape reveals particular focus areas where banks expect the highest returns. In investment banking, AI is enhancing research, financial modeling, and advisory services, supporting deal-making, market analysis, and client engagement. Dedicated platforms like an AI-ready CRM for private banks help operationalize these capabilities across front and middle office teams. Fraud detection and prevention systems typically demonstrate ROI within 12-18 months due to direct loss reduction and improved operational efficiency. Customer service automation delivers returns through reduced staffing costs and improved customer satisfaction scores. Credit risk assessment improvements generate value through better loan performance and expanded lending opportunities.

Venture capital investment in banking ai startups has accelerated dramatically, with specialized funds emerging to focus exclusively on financial technology innovations. All-in-one platforms such as InvestGlass for sales automation exemplify how this ecosystem development ensures continued innovation flow from startups to established banks while creating competitive pressure to deploy ai capabilities more rapidly and effectively.

The geographic distribution of ai banking investments shows concentration in major financial centers, with New York, London, Singapore, and Hong Kong leading in both investment volume and innovation deployment. However, emerging markets are rapidly adopting ai banking solutions and specialized CRM systems for financial institutions, often leapfrogging traditional banking infrastructure to deploy mobile-first, ai-powered financial services.

التوقعات المستقبلية: الاتجاهات المصرفية للذكاء الاصطناعي لعام 2025 وما بعده

The trajectory of ai development in banking points toward even more transformative changes across the broader financial industry in the coming years. Embedded finance integration through ai-powered APIs will enable non-financial companies to seamlessly incorporate banking services into their products and platforms. This trend will blur traditional industry boundaries as retailers, healthcare providers, and technology companies offer banking services powered by ai infrastructure, while central banks themselves explore AI for monetary policy and digital currencies.

تمثل تطبيقات الحوسبة الكمية للنمذجة المالية المعقدة نقلة نوعية يمكن أن تحدث ثورة في تقييم المخاطر وتحسين المحافظ الاستثمارية وكشف الاحتيال. وعلى الرغم من أن أنظمة الذكاء الاصطناعي المعززة كمياً لا تزال في مراحل التطوير المبكرة، إلا أنها تعد بحل المشاكل الحسابية المستعصية حالياً، مما يتيح أساليب جديدة للتنبؤ بالسوق وأمن التشفير وتحليل المخاطر في الوقت الحقيقي.

generative ai for automated financial reporting and analysis will transform how banks create regulatory reports, investment research, and customer communications. Integrating AI technology into bank workflows and reporting systems will help these tools fit existing operations more effectively. These systems can generate comprehensive financial analyses, create personalized investment reports, and draft regulatory filings with minimal human intervention while maintaining accuracy and compliance with reporting standards.

يعد التقارب بين تقنيات سلسلة الكتل والذكاء الاصطناعي بتعزيز الأمن والشفافية في المعاملات المالية. يمكن للعقود الذكية المدعومة بالذكاء الاصطناعي تنفيذ الاتفاقيات المالية المعقدة تلقائيًا استنادًا إلى تحليل البيانات في الوقت الفعلي، بينما توفر تقنية سلسلة الكتل سجلات معاملات غير قابلة للتغيير يمكن لأنظمة الذكاء الاصطناعي تحليلها للكشف عن الاحتيال ومراقبة الامتثال.

Sustainable finance optimization through ai-driven ESG (Environmental, Social, and Governance) analysis will become increasingly important as regulatory requirements for sustainability reporting expand. ai systems can analyze vast amounts of ESG data to help banks assess the sustainability impact of their investments and lending decisions while identifying opportunities in green finance.

الخدمات المصرفية المفتوحة evolution with ai-powered data aggregation will create new possibilities for personalized financial services that span multiple institutions. ai platforms will analyze data from various financial sources to provide comprehensive financial insights, automated money management, and optimized product recommendations across the entire financial ecosystem. As these technologies mature, digital banking supercharges personalization, speed, and resilience.

Looking ahead, banks must remain adaptable, continuously learning and adjusting their strategies to harness ai’s full potential. Integrating ai technologies will be essential for fostering innovation and delivering secure services for a more resilient and agile banking sector in the future.

التقنيات الناشئة التي تشكل مستقبل الذكاء الاصطناعي في القطاع المصرفي

تتقدم عملية معالجة اللغة الطبيعية لتحليل العقود ومراجعة المستندات القانونية بشكل سريع، حيث أصبحت الأنظمة الآن قادرة على تحليل الاتفاقيات المالية المعقدة، وتحديد المصطلحات والمخاطر الرئيسية، والإشارة إلى مشكلات الامتثال المحتملة. ستعمل هذه القدرات على تقليل الوقت والتكلفة المرتبطين بعمليات المراجعة القانونية بشكل كبير مع تحسين الدقة والاتساق.

تمتد تطبيقات الرؤية الحاسوبية في الأعمال المصرفية إلى ما هو أبعد من معالجة الشيكات التقليدية لتشمل التحقق من الهوية, والمصادقة على المستندات وأمن الفروع. يمكن للأنظمة المتقدمة التحقق من هوية العميل من خلال تحليل عوامل بيومترية متعددة في وقت واحد مع الكشف عن المستندات المزورة من خلال تحليل مفصل للصور يتجاوز القدرات البشرية.

تمثل حوسبة الحافة التي تتيح معالجة الذكاء الاصطناعي في الوقت الفعلي في مواقع الفروع تحولاً كبيراً نحو بنى الذكاء الاصطناعي الموزعة. من خلال معالجة أعباء عمل الذكاء الاصطناعي محلياً بدلاً من الاعتماد على الأنظمة السحابية المركزية، يمكن للبنوك تقليل زمن الاستجابة وتحسين حماية الخصوصية والحفاظ على توافر الخدمة حتى عندما يكون الاتصال بالشبكة محدوداً. هذه التطورات مؤثرة بشكل خاص في الخدمات المصرفية للأفراد، حيث يعد تحسين تجربة العملاء وتبسيط سير العمل التشغيلي أمرًا ضروريًا للحفاظ على الميزة التنافسية.

تعمل تكنولوجيا التوأم الرقمي لمحاكاة العمليات المصرفية وتحسينها على إنشاء نسخ افتراضية متماثلة من العمليات المصرفية التي يمكن أن تستخدمها أنظمة الذكاء الاصطناعي لاختبار الاستراتيجيات الجديدة وتحسين سير العمل والتنبؤ بتأثير التغييرات التشغيلية قبل تنفيذها في بيئات الإنتاج. تتيح هذه الإمكانية التحسين المستمر للعمليات المصرفية من خلال التجريب والتحسين القائم على البيانات.

التنفيذ الاستراتيجي: أفضل الممارسات لاعتماد الذكاء الاصطناعي في القطاع المصرفي

Successful ai transformation in banking requires balancing ai automation with human oversight across technology deployment, organizational change, and risk management. Developing comprehensive ai governance frameworks represents the foundation of responsible ai adoption, establishing clear policies for ai system development, deployment, monitoring, and maintenance.

لقد أصبح بناء المواهب في مجال الذكاء الاصطناعي من خلال برامج التدريب والتوظيف الاستراتيجي عامل نجاح حاسم للبنوك التي تسعى إلى تعظيم استثماراتها في مجال الذكاء الاصطناعي. يجب على المؤسسات أن توازن بين توظيف الخبرات الخارجية وتطوير القدرات الداخلية، وإنشاء مسارات وظيفية تجذب أفضل المواهب في مجال الذكاء الاصطناعي مع ضمان نقل المعرفة إلى الموظفين الحاليين. عادةً ما تجمع البرامج الناجحة بين التدريب الرسمي على تقنيات الذكاء الاصطناعي والخبرة العملية في المشاريع التي تسمح للموظفين بتطبيق المهارات الجديدة في سياقات مصرفية حقيقية.

تتطلب استراتيجيات تكامل الأنظمة القديمة من أجل النشر السلس للذكاء الاصطناعي تخطيطًا دقيقًا لضمان إمكانية وصول قدرات الذكاء الاصطناعي الجديدة إلى البيانات الضرورية والتكامل مع العمليات التجارية الحالية. تحتفظ العديد من البنوك بأنظمة أساسية عمرها عقود من الزمن لم يتم تصميمها أبدًا لتكامل الذكاء الاصطناعي، مما يخلق تحديات تقنية يجب معالجتها من خلال حلول البرمجيات الوسيطة وتطوير واجهة برمجة التطبيقات والتحديث التدريجي للنظام.

Customer education initiatives for ai-powered services adoption play a crucial role in realizing the full value of ai investments. Customers must understand how ai enhances their banking experience while feeling confident that their data is protected and that they retain control over important financial decisions. Successful education programs use multiple channels to explain ai benefits in clear, non-technical language, help users understand generative ai tools used in banking services, and address common concerns about privacy and algorithm bias.

تضمن عمليات المراقبة المستمرة للنموذج وعمليات تحسين الأداء أن تحافظ أنظمة الذكاء الاصطناعي على الدقة والفعالية بمرور الوقت. تتغير البيئات المصرفية باستمرار بسبب ظروف السوق والتحديثات التنظيمية واحتياجات العملاء المتطورة، مما يتطلب إعادة تدريب نماذج الذكاء الاصطناعي والتحقق من صحتها بانتظام. تقوم البنوك الرائدة بتطبيق أنظمة المراقبة الآلية التي تتعقب أداء النماذج في الوقت الفعلي وتحدد المشكلات المحتملة قبل أن تؤثر على تجربة العملاء أو نتائج الأعمال.

عادةً ما تمتد الجداول الزمنية لتنفيذ المشاريع المصرفية للذكاء الاصطناعي من 12 إلى 24 شهرًا للمبادرات الرئيسية، مع إطلاق برامج تجريبية غالبًا في غضون 3-6 أشهر للتحقق من صحة المفاهيم وبناء الثقة التنظيمية. تقترح توصيات تخصيص الميزانية تخصيص 601 تيرابايت-3 تيرابايت من استثمارات الذكاء الاصطناعي للبنية التحتية للتكنولوجيا، و251 تيرابايت-3 تيرابايت لتطوير المواهب وإدارة التغيير، و151 تيرابايت-3 تيرابايت لأنشطة المراقبة والتحسين المستمر.

تتبع أكثر تطبيقات الذكاء الاصطناعي نجاحاً نهجاً مرحلياً يبدأ بالتطبيقات منخفضة المخاطر مثل روبوتات الدردشة واكتشاف الاحتيال قبل الانتقال إلى حالات الاستخدام الأكثر تعقيداً مثل الاكتتاب الآلي والمشورة الاستثمارية. يسمح هذا التدرج للمؤسسات ببناء الخبرات وتطوير عمليات الحوكمة وإثبات القيمة أثناء إدارة مخاطر التنفيذ.

تتضمن استراتيجيات التخفيف من المخاطر طوال دورة حياة تطوير الذكاء الاصطناعي بروتوكولات اختبار شاملة، وإجراءات الكشف عن التحيزات وتصحيحها، وآليات احتياطية تضمن استمرارية الخدمة إذا واجهت أنظمة الذكاء الاصطناعي حالات غير متوقعة. تساعد عمليات التدقيق المنتظمة لأداء نظام الذكاء الاصطناعي، الداخلية والخارجية على حد سواء، في تحديد المشكلات المحتملة قبل أن تؤثر على العملاء أو العمليات التجارية.

The transformation of banking through ai technologies represents more than technological change it’s a fundamental reimagining of how financial institutions operate, compete, and serve customers. Banks that successfully navigate this transformation will leverage ai to create sustainable competitive advantages, improve risk management, and deliver exceptional customer experiences that drive business value and support financial stability.

مع استمرار تطور قدرات الذكاء الاصطناعي في التطور، يجب أن تظل البنوك قادرة على التكيف والتعلم المستمر وتعديل استراتيجياتها لتسخير إمكانات الذكاء الاصطناعي الكاملة مع الحفاظ على الثقة التي يضعها العملاء في مؤسساتهم المالية. ستشكل المؤسسات التي تتبنى هذا التحدي مستقبل الخدمات المصرفية والمالية لعقود قادمة.

الأسئلة الشائعة (FAQs)

Q1: How does ChatGPT enhance personalized customer service in banking?

ChatGPT leverages advanced natural language processing to provide 24/7 personalized customer support, handling over 80% of basic inquiries. It tailors responses based on individual account history and preferences, creating a conversational banking experience that improves customer satisfaction and loyalty.

Q2: What significant improvements can banks expect by integrating ChatGPT?

Banks can achieve significant improvements in operational efficiency by automating routine tasks, reducing fraud losses by up to 40%, and accelerating credit risk assessments. ChatGPT also enhances customer engagement through personalized financial advice and faster response times.

Q3: Are there challenges in implementing ChatGPT in banking?

Yes, challenges include ensuring data privacy and security, integrating ChatGPT with existing legacy systems, training customers and staff for adoption, and complying with evolving financial regulations. Banks must also address potential AI biases and maintain human oversight.

Q4: Can ChatGPT assist with loan applications and account management?

Absolutely. ChatGPT-powered chatbots can guide users through loan applications, monitor credit scores, and assist with account management tasks like automatic payments and updating personal information, making banking more accessible and convenient.

Q5: What are the future prospects of AI and ChatGPT in banking?

The future holds even more incredible prospects, including deeper integration with embedded finance, quantum computing for risk modeling, generative AI for automated reporting, and enhanced ESG analysis. These advancements will further personalize services and optimize banking operations.

الخاتمة

ChatGPT is revolutionizing the banking industry by enabling personalized customer service, driving significant improvements in operational efficiency, and transforming the conversational banking experience. By automating routine tasks and enhancing risk management, banks can focus on building stronger client relationships and delivering tailored financial solutions. While challenges such as data privacy, regulatory compliance, and customer adoption remain, the integration of ChatGPT and AI technologies offers even more incredible prospects for the future of banking. Financial institutions that embrace these innovations strategically will not only improve customer satisfaction but also secure a competitive advantage in the rapidly evolving financial landscape.

مقالات ذات صلة

سويس سوفرين سي آر إم: مبني على الذكاء الاصطناعي.

جاهز للتصرف.