Fake IDs have evolved far beyond laminated cards passed between college students. In 2024, they encompass physical documents like altered driver’s licence cards and fully digital forgeries such as manipulated passport scans or synthetic profiles built to bypass Know Your Customer protocols. Whether the goal is to purchase alcohol before turning 21 on a US campus or to open fraudulent Bank accounts using forged European national IDs, the threat touches every regulated business.

High-quality fake IDs often closely mimic the appearance and feel of genuine documents, making detection significantly more challenging for businesses.

For banks, wealth managers and insurers, detecting fake IDs during client onboarding is not optional. InvestGlass works with regulated finansielle institutioner that must verify identity documents while protecting client data sovereignty. This article provides informational guidance in British English and does not constitute legal advice.

Why fake IDs matter to financial institutions:

- Enable money laundering and sanctions evasion

- Expose firms to regulatory penalties under AML frameworks

- Create operational losses from undetected forgeries

- Undermine trust in digital onboarding processes

What is a fake ID

A fake ID is any identification document or credential used to misrepresent a person’s identity, age or legal status. This definition covers physical alterations, complete counterfeits and even genuine documents belonging to another person. In Pennsylvania bars, borrowed student IDs regularly appear at the door. In London during 2023, forged passports enabled fraudulent bank account openings.

In finance, fake IDs extend beyond government cards. Tampered utility bills showing adhesive residue from photo swaps, doctored bank statements with font mismatches and synthetic identities combining real data with fabricated details all qualify.

When a document becomes a fake ID:

- Using someone else’s genuine licence with a mismatched photo

- Altering a birth date by removing and re laminated sections

- Presenting edited scans during online onboarding

- Creating fictitious identities from scratch

Legally Acceptable Forms of Identification

When verifying age or identity for activities such as purchasing alcohol or entering age-restricted venues, it is essential to recognise which forms of identification are legally acceptable. In many jurisdictions, including Pennsylvania, a valid driver’s license, state-issued ID card, or passport are the primary documents accepted for these purposes. Businesses must ensure that the ID presented is current, unexpired, and issued by a recognised government agency.

To avoid the risk of inadvertently serving minors or accepting false identification, staff should be trained to use systematic methods for ID verification. The “F.E.A.R.” method, recommended by the Responsible Alcohol Management Program (RAMP), is a practical approach:

- Feel the ID to check for authenticity, ensuring the card is not flimsy or altered.

- Examine the ID closely for signs of tampering, such as mismatched fonts, uneven lamination, or altered birth dates.

- Ask the individual questions about their age, address, or other details to confirm the information matches the ID.

- Return the ID only after completing these checks and being satisfied it is valid.

By consistently applying these steps, businesses can better verify the age and identity of anyone attempting to purchase alcohol or access restricted services, reducing the risk of legal penalties and protecting their reputation.

Typical uses and motives for fake IDs

The gap between student misuse and organised crime is vast. College students attempting to enter a bar or club before legal age represent one end of the spectrum. Criminals purchasing stolen French passports on the dark web to access EU banking portals represent the other.

Offline motives include alcohol purchases before age 21 in US states like Iowa or Nevada casino entry. Financially, fake IDs facilitate opening accounts for money laundering, evading sanctions, accessing loans under a false name and creating unverified investment accounts.

Typical motives:

- Underage alcohol access (primary for over 1 million scanned fakes)

- Nightclub and casino entry

- Facilitating the illegal sale or purchase of alcohol and other age-restricted items

- Financial fraud and laundering

- Identity theft for portal access

Legal and regulatory consequences of fake IDs

Penalties vary by jurisdiction but carry consistently serious consequences. In Iowa, a fake ID offense can result in the suspension or revocation of a person’s driver’s license for 30 days to one year. The individual may receive an official notice of suspension or revocation by mail from the relevant government agency, such as the Illinois Secretary of State, which sends these notices to the address on file. Illinois classifies possession as a Class 4 felony with up to three years jail time. Florida imposes third-degree felony penalties including five years imprisonment, probation and $5,000 fines even for possessing a fictitious document without use. The licensee, such as a bar owner or business, is legally responsible for verifying IDs and may be subject to penalties if they fail to detect a fake ID during a sale.

Collateral effects extend beyond criminal defense concerns. Universities expel students in college towns like Champaign. Professional licensing bodies bar finance workers with convictions from practice.

For institutions, EU AML Directives, UK Money Laundering Regulations 2017 and Swiss FINMA circulars mandate robust verification. Failures risk regulatory fines, audit failures and fraud losses.

Consequences for individuals:

- Imprisonment and fines

- Driver’s license suspension or revocation, with the subject receiving notice by mail and being subject to administrative procedures and legal consequences following a fake ID offense

- University expulsion

Consequences for institutions:

- Regulatory penalties

- Audit failures

- Fraud losses from undetected synthetics

Common types of fake IDs and fraud techniques

Fraud methods have evolved dramatically with better printing and digital editing tools. The 311% surge in synthetic identity document fraud between 2024 and 2025 reported by Sumsub demonstrates the scale.

Borrowed IDs involve a person presenting a friend’s genuine card, common across US university towns. Altered IDs start as authentic documents but feature modified expiration date fields, swapped photos or peeled laminates revealing tampering. Presenting an expired ID is another common tactic; expired IDs are considered invalid for verification purposes and are frequently detected during checks. Forged IDs are fabricated entirely, with simulated holograms that fail rotation tests and off-spec cardstock.

Digital manipulation now includes high-resolution scans edited with image software, deepfake video used during video-KYC calls and screenshots of manipulated e-wallet identity cards.

Fake ID categories:

- Borrowed genuine IDs (face mismatch)

- Altered documents (modified details)

- Fully forged counterfeits

- Digital scan manipulation

- Synthetic identities

- Deepfake video submissions

Physical security features used to detect fake IDs

Government-issued documents rely on layered security techniques. Holograms on US licences display state emblems or names when tilted under light. EU biometric residence permits feature similar rotating imagery.

Laser perforation creates microscopic holes forming shapes or numbers, visible on Kansas and Swiss licences. UV imagery reveals hidden portraits under blacklight on California licences and many EU passports. Tactile elements include raised lettering, embossed birth date fields and laser-engraved signatures on cards from states like North Carolina.

Material quality matters. Genuine IDs tolerate being bent into a U shape without bubbling, while fakes with bumpy surfaces often show laminate separation.

Physical checks to perform:

- Tilt card to verify hologram shifts

- Inspect under UV for hidden images

- Feel for raised text and embossing

- Flex card to test laminate integrity

- Examine microprinting under magnification

- Compare photo alignment with hologram placement

- Check edge smoothness and card stiffness

Material Integrity

The material integrity of an identification document is a key indicator of its authenticity. Genuine IDs are produced using high-quality materials and advanced manufacturing techniques, making them difficult to alter or replicate. Features such as embedded holograms, laser perforations, and UV imagery are standard on official documents and should be present and intact.

When examining an ID, pay close attention to the following:

- Expiration date: Ensure the ID is still valid and has not passed its expiration date.

- Birth date and physical description: Confirm these details match the person presenting the ID.

- Surface quality: Genuine IDs have smooth, even surfaces, while counterfeit cards may display bumpy surfaces, peeling laminate, or uneven edges, signs of tampering or re-lamination.

- Sikkerhedsfunktioner: Look for microprinting, holograms, and other embedded features that are difficult to forge.

By carefully checking these aspects, staff can more effectively identify altered or fake IDs and prevent fraudulent activity.

Digital signals and behavioural red flags

Many fakes are detected through user behaviour rather than the document itself. Nervousness, hesitation about address or date details, frequent story changes and eye avoidance all signal potential misuse.

Online, red flags include IP addresses from high-risk countries, device fingerprints appearing across multiple identities and metadata conflicts on uploaded images. Identity theft patterns emerge when the same passport number appears across different platforms.

Behavioural indicators:

- Inconsistent personal details when questioned

- Physical description mismatch with photo

- Multiple applications using identical document numbers

- Device fingerprints linked to other suspicious accounts

State and country specific ID features

Every jurisdiction uses different design standards. US states like Virginia issue vertical licences for people under 21 versus horizontal for those over. Unique backgrounds feature state flowers or capitol buildings.

European identity cards use country-specific themes and machine-readable zones. German, French and Swiss documents each carry distinct visual elements. Canadian provinces vary layouts significantly.

Best practices for staying informed:

- Subscribe to government agency updates

- Use an id checking guide updated annually

- Train staff on document type variations

- Maintain reference materials for frequently seen formats

- Review official government resources regularly

How businesses traditionally check for fake IDs

Manual checking methods remain common in pubs, off-licences and campus venues. Staff follow routines like feel, examine, ask and return. They verify the cardholder matches the photo, calculate age from the birth date and cross-check with a second form of identification when doubts arise.

Limitations of manual inspection:

- Human error under time pressure

- Inconsistent training across staff members

- Difficulty recognising dozens of document formats

- Limited ability to verify machine-readable data

From manual checks to automated identity verification

Automatiseret Identitetsbekræftelse became widespread between 2018 and 2024, particularly in banking and fintech. Modern solutions use OCR for data extraction, tampering detection via edge analysis, template matching against over 100 formats and MRZ validation.

Biometric comparison through selfie or video verification adds another layer. IDScan.net reports 95% detection rates with advanced tools.

Advantages of automated verification:

- Faster onboarding times

- Lower fraud losses

- Evidence logs for auditors

- Consistent policy application

- Valid document confirmation

- Liveness detection capabilities

Institutions have observed a significant dropping in fraud detection rates and compliance cases after implementing automated identity verification solutions.

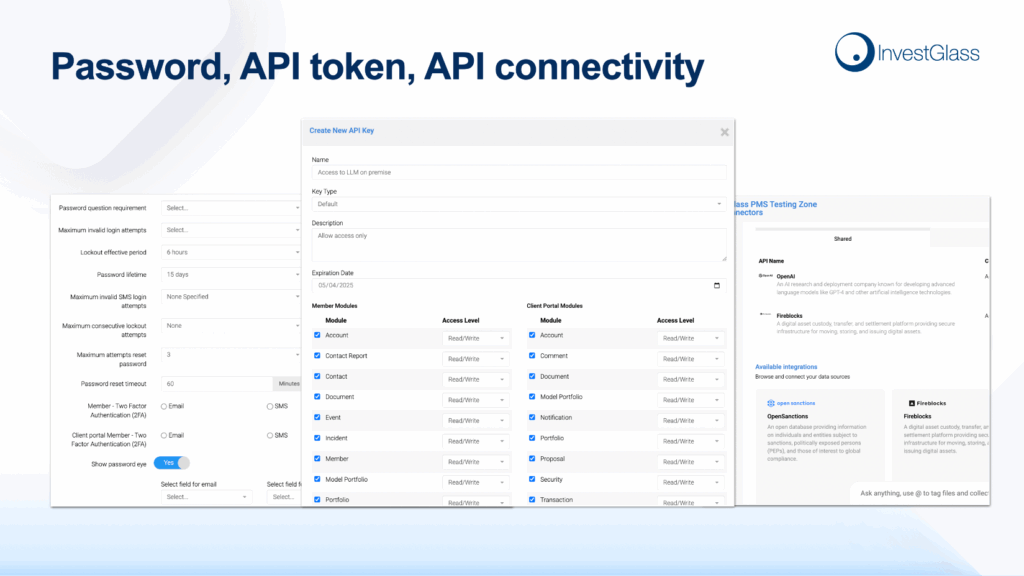

How InvestGlass helps detect fake IDs and protect sovereignty

InvestGlass er et schweizisk suveræn CRM and onboarding platform for financial institutions requiring strong ID verification controls. The platform integrates digital onboarding and KYC workflows, allowing banks, wealth managers and insurers to collect documents, verify them and store results centrally.

Features include configurable KYC forms, automated approval rules, complete audit trails and alerts when information appears inconsistent. InvestGlass offers hosting in Switzerland or on-premise deployment, keeping client identity data under European or local control rather than on American or Chinese public clouds.

How InvestGlass reduces fake ID risk:

- Integrated document verification workflows

- Configurable rules for automatic flagging

- Swiss-hosted or on-premise data residency

- Complete audit trails for regulatory review

- Protection from extraterritorial data access

For additional ID verification resources or to check reinstatement requirements after a licence suspension, individuals can visit the relevant DMV or government website.

Compliance, audit trails and regulator expectations

Regulators like FINMA, the FCA and EU supervisors expect institutions to demonstrate robust identity verification through documented records. Using a sovereign platform helps institutions prove they verified IDs, retained evidence and reacted to red flags.

What a complete KYC audit trail should include:

- Timestamps for each verification step

- Results of automated checks

- Secure copies of identity documents

- Notes from compliance officers

- Escalation records for suspicious cases

Prevention and Collaboration

Preventing the use of fake IDs and combating identity theft requires a collaborative approach. Businesses, government agencies, and law enforcement must work together to share information, develop best practices, and educate vulnerable groups such as college students about the risks and consequences of using or possessing fake identification.

Educational initiatives can help college students understand that using a fake ID or someone else’s ID card is not only a violation of the law but can also lead to serious consequences, including criminal charges and long-term impacts on their record. Businesses can support prevention by providing regular training for staff on how to identify fake IDs and by staying informed about the latest fraud techniques.

Collaboration between organisations and government bodies enables the sharing of intelligence on new types of fake IDs and identity theft trends. By working together, stakeholders can develop more effective strategies to prevent fake ID use and protect both individuals and businesses from the consequences of identity theft.

Balancing user experience with fraud prevention

Strong controls must not drive legitimate clients to abandon onboarding. InvestGlass allows firms to design streamlined journeys with progressive disclosure, mobile-friendly forms and instant feedback when uploads are unclear.

Workflows adapt by risk level. Low-risk clients receive simplified due diligence while higher-risk profiles face enhanced checks.

UX improvements:

- Pre-validation of data fields

- Instant feedback on unclear uploads

- Risk-tiered verification depth

Why sovereign infrastructure matters when handling IDs

Identity documents and biometric data carry extreme sensitivity, particularly for high-net-worth clients. Swiss and on-premise hosting contrasts sharply with reliance on American or Chinese cloud ecosystems where extraterritorial access concerns persist.

InvestGlass enables institutions to retain legal and technical control over identity records, including data residency, encryption keys and access management.

Why sovereign platforms are safer:

- Data residency under European law

- Control over encryption keys

- No exposure to foreign government access requests

- Compliance with GDPR and banking secrecy requirements

- Protection of client data sovereignty

Practical checklist for frontline staff and compliance teams

Physical venue checks:

- Calculate age from birth date using correct math

- Inspect holograms, UV features and tactile elements

- Compare face to photo for match

- Ask control questions about address and details

- Refuse service at discretion if unsure

Financial institution checks:

- Verify document type and issuing country

- Confirm MRZ and machine-readable data

- Run automated verification in InvestGlass

- Escalate suspicious cases to compliance

- Document all steps with timestamps

Ongoing requirements:

- Train staff at least annually

- Update procedures when new formats release

- Monitor fraud pattern changes by state or country

Resources and Support

A range of resources and support services are available to help individuals and businesses address the challenges posed by fake IDs and identity theft. The ID Checking Guide, published by the Drivers License Guide Co., is a comprehensive reference that assists businesses in identifying genuine and fake IDs across different states and countries. This guide can be ordered online or by phone and is an invaluable tool for anyone responsible for checking identification.

Government agencies, such as the Pennsylvania Liquor Control Board, provide guidance and support to help businesses comply with ID checking laws and regulations. These agencies often offer training materials, updates on new document types, and advice on best practices for verifying IDs.

For individuals who have been affected by identity theft, resources such as the Federal Trade Commission’s Identity Theft website offer step-by-step guidance on how to recover and protect personal information. By utilising these resources and fostering a supportive network, both businesses and individuals can take proactive steps to prevent fake ID use and mitigate the impact of identity theft.

Conclusion and next steps

Fake IDs remain a persistent threat demanding both physical vigilance and digital sophistication. Regulated firms must protect compliance status and client data simultaneously. InvestGlass offers a sovereign Schweizisk CRM and onboarding platform that helps institutions verify identities without sending data to American or Chinese providers.

Næste skridt:

- Review current ID checking procedures against this guide

- Map regulatory requirements for your jurisdiction

- Evaluate sovereign solutions like InvestGlass for digital onboarding

- Contact InvestGlass to discuss deployment options

Relaterede artikler

Swiss Sovereign CRM: Bygget på AI.

Klar til at handle.