Introduction: Scope, Audience, and Importance

Enhanced due diligence is usually required for high-risk customers, transactions, and jurisdictions. This article is designed for compliance professionals and financial institutions seeking to understand exactly when Enhanced Due Diligence (EDD) is required, who it applies to, and why recognizing EDD triggers is essential for anti-money laundering (AML) compliance. Knowing when to apply EDD ensures that organizations can identify and mitigate risks related to money laundering, terrorist financing, and other financial crimes, while meeting regulatory expectations and avoiding penalties.

Czego się dowiesz

- What enhanced due diligence (EDD) entails and how it differs from standard customer due diligence

- The specific circumstances and types of customers that require EDD

- The role of EDD in managing high-risk customers and ensuring AML compliance

- How comprehensive risk assessment informs the application of EDD

- Best practices for implementing EDD within financial institutions

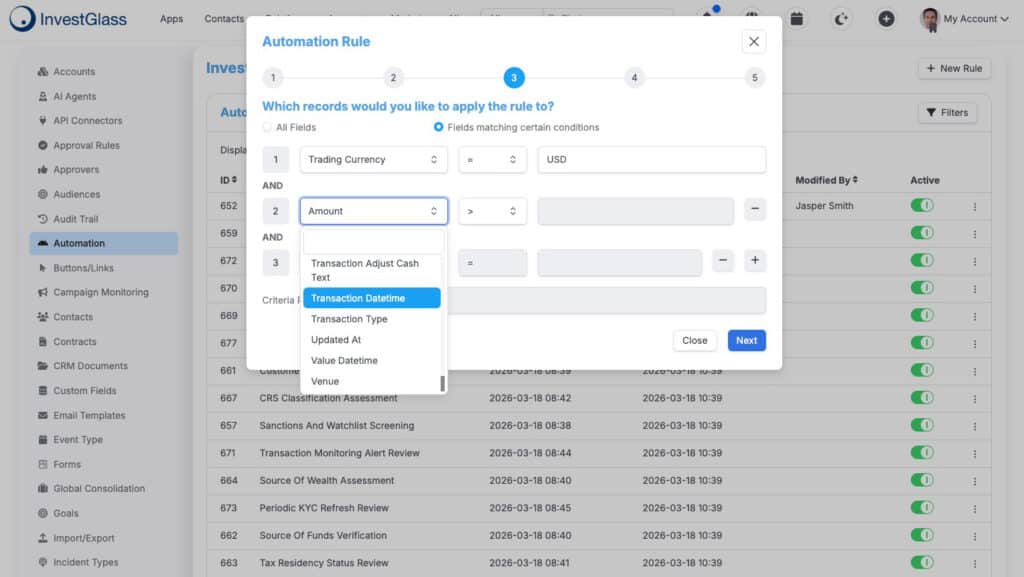

Visual overview of the enhanced due diligence (EDD) process workflow

Czym jest rozszerzona analiza due diligence (EDD)?

Enhanced Due Diligence (EDD) is a more rigorous and detailed process of verifying and assessing a customer’s identity, financial activities, and risk profile compared to standard customer due diligence (CDD). EDD is a risk-based extension of the Know Your Customer (KYC) process, involving deeper investigation for high-risk customers or transactions. It is primarily designed to mitigate the higher risks associated with certain customers, transactions, or jurisdictions that could potentially facilitate money laundering, terrorist financing, or other financial crimes.

EDD is guided by a risk-based approach to assess and mitigate associated risks and is mandated by regulatory requirements. While CDD applies to all clients, EDD is specifically mandated for high-risk customers or situations identified through a detailed risk assessment. Regulatory frameworks such as the Financial Action Task Force (FATF) and local authorities emphasize EDD as a key defense mechanism in the global fight against financial crime.

Key Differences Between CDD and EDD

- Scope and Depth: Standard CDD verifies basic identity information and risk profile, whereas EDD involves an exhaustive examination of customer background, financial behavior, and source of wealth.

- Documentation: EDD requires collecting additional documents such as proof of income, business ownership records, or detailed transaction histories.

- Monitoring: Customers subject to EDD are monitored more frequently and with greater scrutiny to detect unusual or suspicious activities promptly.

In our experience at InvestGlass, a Swiss-sovereign CRM and cyfrowy onboarding platform, EDD is a critical component for ensuring stringent AML compliance. It involves gathering additional information, scrutinizing sources of funds, and closely monitoring ongoing customer relationships. Enhanced customer due diligence includes additional checks like source-of-funds analysis, adverse media review, and ongoing monitoring compared to standard CDD. This elevated level of scrutiny helps firms manage and reduce risk exposure effectively.

By understanding the foundational concept of enhanced due diligence, financial institutions can better prepare to identify when it is necessary and implement appropriate measures to safeguard their operations. The following sections will explore the specific scenarios and customer profiles where EDD is usually required.

Czego się dowiesz

- The specific scenarios that mandate enhanced due diligence

- Why EDD is critical for managing high-risk customers

- How AML compliance drives the need for enhanced checks

- The role of risk assessment in determining EDD requirements

- Practical insights from InvestGlass on implementing effective EDD

When is Enhanced Due Diligence Required?

Enhanced Due Diligence (EDD) is required primarily when dealing with high-risk customers or transactions that pose a greater threat to financial institutions’ integrity and regulatory compliance. At its core, EDD is a more stringent form of customer due diligence (CDD) designed to provide deeper insight into potential risks and mitigate the possibility of money laundering, terrorism financing, or fraud.

Summary List: Main Triggers for EDD

- When a customer or transaction poses a higher risk of money laundering or sanctions exposure

- High-risk factors including Politically Exposed Persons (PEPs), high-risk jurisdictions, and complex ownership structures

- Unusual transactions that deviate from a customer’s normal behavior, such as large cash deposits

- When a customer provides altered or stolen documents during onboarding

- When a customer is located in a country on the FATF’s blacklist or greylist

- For high-value transactions that pose a higher risk of money laundering or financial crime

- When there is insufficient information from standard CDD to assess risk

High-Risk Customers and Jurisdictions

EDD is mandated when a customer or transaction is classified as high risk. This includes individuals or entities from countries identified by regulatory bodies as having inadequate anti-money laundering (AML) controls or high levels of corruption. High-Risk Jurisdictions are countries with weak anti-money laundering controls or that are sanctioned, linked to higher-risk clients or transactions. For example, customers from jurisdictions on the Financial Action Task Force (FATF) grey or blacklists, commonly referred to as high-risk countries, require enhanced scrutiny. Customer identification and verification of legal entities are crucial steps in this process, especially when dealing with high-risk countries to ensure legitimacy and compliance.

Our expertise at InvestGlass highlights that risk assessment frameworks should prioritize geographic risk as a key factor. Incorporating sovereign risk intelligence into your System CRM enables automated triggers for enhanced measures when onboarding clients from these high-risk zones.

Politically Exposed Persons (PEPs)

Politically Exposed Persons (PEPs) are individuals holding prominent public positions, their family members, and close associates considered higher risk for corruption and money laundering. Due to their position, PEPs present a higher risk of involvement in bribery or corruption. Regulators universally require firms to apply EDD when onboarding or conducting transactions with PEPs. High-risk individuals, such as PEPs, require a tailored diligence checklist as part of the EDD process to ensure thorough verification and ongoing monitoring.

InvestGlass’s Swiss-sovereign CRM platform integrates comprehensive PEP screening tools, ensuring organizations can efficiently identify and manage these high-risk profiles.

Complex Ownership Structures and Beneficial Ownership Transparency

Complex Ownership Structures refer to entities with non-transparent ownership that obscure the ultimate beneficial owner (UBO). When customers use complex corporate structures to conceal their true beneficjenci rzeczywiści, firms must perform enhanced due diligence to uncover these details. This is vital to prevent misuse of shell companies for illicit purposes. Reviewing the customer’s transaction history and financial transactions is essential to detect suspicious activity and assess the legitimacy of the ownership structure.

In our experience at InvestGlass, enhanced due diligence processes must include verification of ultimate beneficial ownership (UBO) information and ongoing monitoring of changes in ownership or control.

Unusual or High-Value Transactions

Unusual or High-Value Transactions involve patterns of activity that are complex, large, or without an obvious economic purpose, triggering EDD. Any transactions that are unusually large, or complex with the investor’s known business profile often trigger enhanced due diligence. Such transactions may indicate attempts to launder money or finance terrorism.

AML compliance demands that firms implement automated alerts within their digital onboarding platforms to flag these transactions for enhanced investigation.

Non-Face-to-Face Relationships

Remote onboarding or transactions conducted without direct physical interaction increase the risk of identity fraud. Enhanced due diligence helps verify the authenticity of customers through additional documentation, biometric verification, or third-party data sources.

InvestGlass’s digital onboarding solutions streamline these processes, making EDD practical and scalable while maintaining compliance.

Other EDD Triggers

- When a customer provides altered or stolen documents during onboarding

- When there is insufficient information from standard CDD to assess risk

EDD is essential for onboarding high-risk customers and minimizing the risk of existing relationships. It is particularly important for financial institutions due to the high stakes involved in managing large transactions and high-risk clients.

Why is Enhanced Due Diligence Necessary?

Regulatory Expectations and AML Compliance

Regulators worldwide mandate that financial institutions and certain non-financial businesses implement risk-based approaches to customer due diligence. Enhanced due diligence is a fundamental component of this approach, particularly for mitigating higher risks. EDD provides reasonable assurance that regulatory requirements are met by verifying customer legitimacy and supporting ongoing monitoring.

Failure to conduct EDD appropriately can lead to severe penalties, reputational damage, and loss of licenses. Our expertise at InvestGlass shows that comprehensive EDD frameworks safeguard organizations against regulatory breaches and build trust with stakeholders.

Protecting the Financial System

EDD serves as a crucial barrier against the infiltration of illicit funds into the financial system. By scrutinizing high-risk customers more intensively, institutions can detect and prevent money laundering, terrorist financing, and other financial crimes.

Risk Mitigation and Reputation Management

High-risk customers can expose firms to operational, legal, and reputational risks. Enhanced due diligence reduces these risks by ensuring that only legitimate clients are onboarded and monitored continuously. An effective ongoing monitoring strategy, tailored to the customer’s risk profile, is essential for detecting suspicious activities and responding to changes in risk.

InvestGlass’s CRM platform supports continuous risk assessment by integrating real-time data feeds, allowing firms to update risk profiles and trigger EDD when new risk indicators emerge.

Facilitating Informed Risk-Based Decisions

EDD enables firms to make informed decisions about whether to accept, continue, or terminate business relationships. It provides deeper insights into customers’ backgrounds, source of funds, and intended transaction patterns. Assigning a risk score to each customer helps guide the application of EDD measures and ensures that resources are focused on higher-risk relationships.

This intelligence is critical for effective risk management and compliance, aligning with international standards such as those set by the FATF.

In summary, enhanced due diligence is required whenever there is an elevated risk associated with a customer or transaction. Whether due to geographic location, political exposure, ownership complexity, transaction size, or remote onboarding, EDD ensures a thorough understanding of risks and protects firms from financial crime and regulatory sanctions. At InvestGlass, our Swiss-based sovereign CRM and digital onboarding platform empowers businesses to implement effective, scalable EDD processes aligned with global AML compliance standards.

EDD helps financial institutions manage high-risk relationships responsibly and ensures compliance with AML/KYC regulations. Its importance lies in helping institutions comply with regulatory requirements and avoid reputational damage.

For more insights on optimizing your risk assessment and customer due diligence workflows, explore our AML Compliance Solutions and discover how InvestGlass can support your enhanced due diligence requirements.

Transition: Now that we’ve covered when and why EDD is required, let’s examine the specific customer profiles that trigger enhanced due diligence.

Who Does Enhanced Due Diligence Apply To? (PEPs, High-Risk Jurisdictions, Complex Ownership Structures)

Meta Description:

Discover who Enhanced Due Diligence (EDD) applies to, including Politically Exposed Persons (PEPs), customers from high-risk jurisdictions, and those with complex ownership structures. Learn how EDD strengthens AML compliance and risk assessment.

Czego się dowiesz

- The specific customer profiles that require Enhanced Due Diligence

- Why PEPs and individuals from high-risk jurisdictions demand additional scrutiny

- The challenges posed by complex ownership structures in customer due diligence

- How applying EDD supports robust AML compliance and risk management

Enhanced Due Diligence Customer Profiles

Enhanced Due Diligence (EDD) primarily applies to customers who present an elevated risk of money laundering or terrorist financing. These include:

- Politically Exposed Persons (PEPs): Politically Exposed Persons (PEPs) are individuals holding prominent public positions, their family members, and close associates considered higher risk for corruption and money laundering.

- High-Risk Jurisdictions: High-Risk Jurisdictions are countries with weak anti-money laundering controls or that are sanctioned, linked to higher-risk clients or transactions.

- Complex Ownership Structures: Complex Ownership Structures refer to entities with non-transparent ownership that obscure the ultimate beneficial owner (UBO).

Identifying high-risk customers and applying tailored diligence procedures is essential for effective risk assessment and regulatory compliance. In our experience at InvestGlass, understanding these categories is crucial to maintaining effective AML compliance and conducting thorough risk assessments.

Enhanced customer due diligence is especially relevant for high-risk industries. Certain sectors such as banking, cryptocurrency exchanges, and gambling face higher regulatory scrutiny due to vulnerability to financial crime. High-risk industries include sectors inherently more vulnerable to financial crime, such as gambling, virtual assets, and correspondent banking.

Politically Exposed Persons (PEPs)

PEPs are individuals who hold or have held prominent public positions, such as heads of state, senior government officials, or high-ranking military officers. Due to their influence and access to public funds, PEPs are inherently at a higher risk of involvement in corruption or bribery schemes. Consequently, regulators worldwide mandate that financial institutions and service providers apply Enhanced Due Diligence when onboarding or monitoring PEPs.

EDD for PEPs involves deeper scrutiny, such as verifying the sources of wealth and funds, ongoing monitoring of transactions, and obtaining senior management approval before establishing a business relationship. The goal is to mitigate the risk of facilitating illicit financial activities unknowingly. At InvestGlass, our Swiss-sovereign CRM platform integrates automated alerts and customized risk profiles, enabling seamless identification and monitoring of PEPs as part of a robust customer due diligence process.

Customers from High-Risk Jurisdictions

Another key group requiring Enhanced Due Diligence are customers linked to jurisdictions with elevated risks of money laundering, corruption, or terrorism financing. These regions may be subject to international sanctions, have weak regulatory frameworks, or exhibit significant levels of financial secrecy.

EDD procedures for customers from these high-risk jurisdictions typically include verifying the legitimacy of business operations, enhanced source of funds checks, and closer transaction monitoring. This ensures compliance with international and local regulations, reducing reputational and financial risks for the institution.

Our expertise in Swiss-sovereign CRM solutions at InvestGlass demonstrates that integrating jurisdictional risk data directly into onboarding workflows allows for dynamic application of EDD measures. This approach enhances compliance efficiency and ensures that no high-risk customer bypasses critical safeguards.

Customers with Complex Ownership Structures

Entities with complex ownership or control structures often present heightened risks because they can obscure the true beneficial owners. Such complexity can be due to multiple layers of ownership, the use of trusts, nominee shareholders, or offshore companies.

Applying Enhanced Due Diligence in these cases involves performing detailed investigations to identify and verify the ultimate beneficial owners (UBOs). This includes gathering comprehensive documentation, conducting background checks, and understanding the purpose and nature of the business relationship. Financial institutions must also assess whether the structure is designed to evade regulatory scrutiny or conceal illicit activities.

In our experience at InvestGlass, digital onboarding platforms equipped with advanced due diligence tools simplify the verification of complex ownership structures. By automating data collection and cross-referencing with global databases, our CRM solution empowers compliance teams to perform thorough risk assessments without compromising operational efficiency.

Other High-Risk Customer Categories

While PEPs, high-risk jurisdictions, and complex ownership structures are the most common triggers for Enhanced Due Diligence, other customer categories may also warrant EDD, including:

- Customers with unusual or suspicious transaction patterns

- Businesses operating in high-risk industries such as casinos, arms trade, or cryptocurrencies

- Non-resident customers or those unwilling to provide complete information

Applying EDD to these groups helps maintain a robust customer due diligence framework, ensuring that all potential risks are adequately managed.

The Importance of Enhanced Due Diligence in AML Compliance

Applying Enhanced Due Diligence to these high-risk customers is not just a regulatory requirement but a critical component of a mature AML compliance program. EDD provides a more granular understanding of customer risk profiles, which is essential for effective risk assessment and decision-making.

At InvestGlass, we advocate for embedding EDD workflows into CRM and digital onboarding processes. This integration allows financial institutions to maintain continuous compliance, adapt to evolving regulatory expectations, and safeguard against financial crime effectively.

By recognizing who requires Enhanced Due Diligence and implementing targeted procedures, organizations can significantly reduce exposure to financial crime risks while streamlining compliance efforts. Our Swiss-based sovereign CRM platform at InvestGlass offers tailored solutions to facilitate these complex due diligence processes, ensuring your institution stays ahead in an ever-changing regulatory landscape.

Transition: Understanding who requires EDD sets the stage for exploring the regulatory frameworks that govern these requirements.

Regulatory Frameworks Governing Enhanced Due Diligence (FATF, EU AMLD, FinCEN)

Meta Description:

Explore the key regulatory frameworks governing Enhanced Due Diligence (EDD), including FATF recommendations, the EU’s AML Directive, and FinCEN guidelines. Understand how these regulations shape AML compliance and risk assessment for high-risk customers.

Czego się dowiesz

- The role of FATF in setting global standards for EDD

- How the European Union’s AML Directive mandates EDD implementation

- The importance of FinCEN regulations in the United States

- The impact of these frameworks on customer due diligence processes

- Best practices for compliance and risk management with EDD

Regulatory Frameworks Governing Enhanced Due Diligence

Enhanced Due Diligence (EDD) is a critical component of anti-money laundering (AML) compliance. It is mandated by several international and national regulatory bodies to mitigate risks posed by high-risk customers and complex transactions. In our experience at InvestGlass, understanding the regulatory landscape that governs EDD is essential for financial institutions and businesses aiming to maintain compliance and protect their operations.

FATF: The Global Standard-Setter for EDD

The Financial Action Task Force (FATF) is an intergovernmental organization that sets global standards to combat money laundering, terrorist financing, and other related threats. FATF’s recommendations form the foundation of AML compliance frameworks worldwide.

FATF explicitly mandates the application of Enhanced Due Diligence for customers and transactions that present a higher risk. This includes politically exposed persons (PEPs), correspondent relacje bankowe, and jurisdictions with strategic deficiencies in AML controls. FATF Recommendation 10 outlines the need for increased scrutiny and ongoing monitoring of such high-risk customers.

In practice, FATF requires institutions to perform a comprehensive risk assessment to identify situations necessitating EDD. This assessment involves gathering detailed information about the customer’s identity, source of funds, and the nature of the business relationship. The goal is to ensure no illicit activity is concealed under legitimate transactions.

At InvestGlass, our Swiss-sovereign CRM platform incorporates FATF’s principles, enabling seamless integration of EDD workflows that align with the highest international compliance standards. This helps firms conduct detailed customer due diligence while managing risks effectively.

European Union AML Directive: Strengthening EDD Across Member States

The European Union’s Anti-Money Laundering Directives (AMLD) are crucial regulatory instruments that enforce AML compliance within its member states. The latest iteration, AMLD 6 and AMLD 5, place a significant emphasis on the implementation of Enhanced Due Diligence measures for high-risk customers.

Under the EU AMLD, financial institutions must identify and verify customers’ identities, conduct a thorough risk assessment, and apply EDD when dealing with politically exposed persons, high-value transactions, and customers from high-risk third countries. The directives also require continuous monitoring of business relationships to detect suspicious activities promptly.

A notable feature of the EU AMLD is the obligation to maintain beneficial ownership registers and perform due diligence on trusts and corporate structures. This transparency is pivotal in applying EDD effectively, as it helps uncover hidden ownership that could pose money laundering risks.

Our expertise in Swiss-sovereign CRM systems at InvestGlass shows that automating compliance with the EU AMLD’s EDD requirements can drastically reduce manual errors and improve regulatory reporting. Through tailored risk scoring models, institutions can ensure consistent application of EDD across all customer segments.

FinCEN: U.S. Regulatory Expectations for Enhanced Due Diligence

In the United States, the Financial Crimes Enforcement Network (FinCEN) is the key regulatory body overseeing AML compliance. FinCEN issues detailed guidance on when and how to apply Enhanced Due Diligence, particularly under the Bank Secrecy Act (BSA).

FinCEN regulations require financial institutions to implement robust customer due diligence programs that include verifying customer identities, understanding ownership structures, and monitoring transactions. For accounts deemed high risk such as correspondent accounts, non-resident alien accounts, or customers operating in high-risk industries FinCEN mandates enhanced scrutiny.

One critical aspect emphasized by FinCEN is the ongoing monitoring of high-risk customers to identify suspicious activity promptly. Institutions must document their risk assessment methodologies and maintain records demonstrating compliance with EDD standards.

InvestGlass’s platform supports compliance with FinCEN’s EDD requirements by providing a comprehensive digital onboarding process and risk assessment tools. This simplifies the gathering of customer information and ensures consistent application of AML controls, mitigating regulatory risks.

The Combined Impact of These Regulatory Frameworks

Together, FATF, the EU AMLD, and FinCEN form a robust regulatory framework that compels institutions to adopt Enhanced Due Diligence as a vital part of their AML compliance programs. These frameworks share common principles:

- Identification and verification of high-risk customers

- Detailed risk assessments to tailor due diligence efforts

- Continuous monitoring of business relationships

- Documentation and record-keeping for regulatory audits

For businesses operating internationally or dealing with cross-border clients, aligning with these regulations can be complex. However, leveraging advanced CRM and digital onboarding solutions like those offered by InvestGlass allows seamless compliance integration, facilitating efficient risk assessment and AML adherence.

Wnioski

In summary, Enhanced Due Diligence is not just a best practice but a regulatory requirement enforced by leading global authorities such as FATF, the EU AMLD, and FinCEN. These frameworks ensure financial institutions implement rigorous controls to identify and mitigate risks posed by high-risk customers. By understanding and integrating these regulatory standards into customer due diligence processes, organizations can enhance their AML compliance and safeguard their operations against financial crime.

For firms aiming to streamline their EDD workflows while remaining compliant, InvestGlass offers tailored solutions designed to meet the stringent demands of these regulatory frameworks, ensuring a secure and compliant onboarding experience.

Transition: With a clear understanding of the regulatory context, let’s explore the step-by-step process for conducting Enhanced Due Diligence.

The Step-by-Step Enhanced Due Diligence Process

Meta Description:

Discover the comprehensive step-by-step Enhanced Due Diligence (EDD) process essential for managing high-risk customers and ensuring robust AML compliance. Learn how to conduct thorough risk assessments and implement effective customer due diligence with insights from InvestGlass.

Czego się dowiesz

- The detailed steps of the Enhanced Due Diligence process

- Why EDD is critical for managing high-risk customers

- How to conduct a thorough risk assessment during customer due diligence

- Best practices for maintaining AML compliance

- Practical insights based on InvestGlass’s expertise

Enhanced Due Diligence (EDD) is a critical component of any robust anti-money laundering (AML) framework, especially when dealing with high-risk customers. The process involves a series of meticulous steps designed to provide deeper insights into a customer’s profile, source of funds, and transactional behavior. In this section, we break down the step-by-step process of EDD, highlighting best practices and how firms like InvestGlass leverage technology to streamline compliance.

Step 1: Identification and Verification of Customer Identity

- Identification and Verification of Customer Identity

- Set process in InvestGlass

- Verify the customer’s identity with a higher degree of scrutiny than standard customer due diligence.

- Obtain and authenticate official documents such as passports, national ID cards, or corporate registration certificates.

- For high-risk customers, go beyond basic document verification, including cross-referencing multiple identification sources and using biometric verification where possible.

- Financial institutions must conduct Enhanced Due Diligence when a customer provides altered or stolen documents during onboarding.

- Integrating such verification tools within a Swiss-sovereign CRM platform significantly reduces risks associated with identity fraud.

Step 2: Detailed Risk Assessment and Customer Profiling

- Detailed Risk Assessment and Customer Profiling

- Set process in InvestGlass

- Evaluate the customer’s risk profile based on several factors:

- Set process in InvestGlass

- Geographic location

- Nature of business activities

- Source of wealth and funds

- Politically Exposed Person (PEP) status

- Previous financial behavior and reputational risks

- Establish the customer’s risk profile and assign a risk score to guide the level of due diligence required.

- Automating risk assessment through advanced algorithms embedded in CRM platforms improves accuracy and efficiency.

Step 3: Understanding the Source of Funds and Wealth

- Understanding the Source of Funds and Wealth

- Set process in InvestGlass

- Gain a clear understanding of the customer’s source of funds and wealth.

- Customers must provide detailed information about how their funds were accumulated, including supporting documentation such as bank statements, tax returns, financial statements, or evidence of business profits.

- Verify the customer’s real assets, such as physical property, alongside financial statements, to ensure transparency and legitimacy regarding ownership and the true value of assets.

Step 4: Enhanced Monitoring and Transaction Scrutiny

- Enhanced Monitoring and Transaction Scrutiny

- Set process in InvestGlass

- EDD extends beyond initial onboarding and requires continuous monitoring of the customer’s transactions and behavior to detect any suspicious activities.

- High-risk customers are subject to more frequent and detailed reviews compared to standard clients.

- Adverse media screening is essential for identifying potential reputational or compliance risks associated with clients or transactions.

- Transaction monitoring includes setting thresholds for unusual activity, verifying the legitimacy of transactions, reviewing the customer’s transaction history for suspicious patterns, and conducting periodic reviews of customer profiles.

Step 5: Conducting Senior Management Approval

- Conducting Senior Management Approval

- Set process in InvestGlass

- Many regulatory frameworks mandate that senior management reviews and approves the onboarding of high-risk customers following Enhanced Due Diligence.

- Senior management must evaluate whether the potential business relationship aligns with the firm’s risk appetite and compliance policies.

- Workflow tools that document this proces zatwierdzania ensure a transparent and auditable trail.

Step 6: Documentation and Record-Keeping

- Dokumentacja i prowadzenie rejestrów

- Set process in InvestGlass

- Proper documentation is fundamental throughout the EDD process.

- All steps from weryfikacja tożsamości and risk assessment to source of funds and senior management approval must be meticulously recorded and securely stored.

- Regulatory authorities often require firms to retain these records for extended periods, typically five to ten years.

Step 7: Periodic Review and Reassessment

- Periodic Review and Reassessment

- Set process in InvestGlass

- High-risk customers require ongoing periodic reviews to reassess their risk profiles and ensure continued compliance with AML regulations.

- This may involve refreshing documentation, re-evaluating sources of wealth, and updating transaction monitoring parameters.

- Automating reminders and workflows for these periodic reviews reduces the risk of oversight.

Step 8: Escalation and Reporting of Suspicious Activities

- Escalation and Reporting of Suspicious Activities

- Set process in InvestGlass

- If any suspicious activity or discrepancies arise during the EDD process or subsequent monitoring, firms must escalate the findings internally and potentially report to relevant authorities such as Financial Intelligence Units (FIUs).

- Suspicious activity should be reported directly to the jurisdiction’s financial intelligence unit (FIU) to ensure proper oversight and compliance with AML regulations.

- Writing a report detailing the investigation findings is a crucial step in the EDD process.

In conclusion, the Enhanced Due Diligence process is a detailed, multi-step approach designed to mitigate the risks associated with high-risk customers. By following these steps diligently, financial institutions can strengthen their AML compliance frameworks and protect themselves from regulatory penalties. Our expertise at InvestGlass underlines the value of leveraging technology-driven solutions to streamline and enhance every phase of this critical process.

For more insights on customer due diligence and risk assessment, explore our Blog InvestGlass and discover how our Swiss-sovereign CRM platform can support your compliance journey.

Transition: Having explored the EDD process, let’s see how automation can further enhance compliance and efficiency.

How InvestGlass Automates EDD Workflows, Conclusion, and 10 FAQs

How InvestGlass Automates EDD Workflows

Enhanced Due Diligence (EDD) is a critical component of effective AML compliance and risk management, particularly when dealing with high-risk customers. In our experience at InvestGlass, manual EDD processes can be time-consuming, error-prone, and costly, often resulting in compliance gaps or operational inefficiencies.

That is why InvestGlass has developed an intelligent CRM and digital onboarding platform designed to automate and streamline EDD workflows without compromising regulatory standards. RegTech solutions are increasingly used to automate Enhanced Due Diligence tasks, improving efficiency and compliance. AI and machine learning tools are also being adopted to detect risks faster and more accurately in EDD processes. Automated EDD processes help reduce false positives and allow compliance teams to focus on genuine risks.

Our Swiss-sovereign CRM platform integrates advanced risk assessment tools to automatically flag clients that require enhanced due diligence based on predefined criteria such as geographic risk, politically exposed persons (PEPs), transaction patterns, and source of funds. Once flagged, the system triggers tailored workflows that guide compliance officers through the necessary steps, including in-depth identity verification, documentation collection, and ongoing monitoring.

The automation extends to robust customer due diligence (CDD) data collection, where InvestGlass employs dynamic questionnaires and document upload portals that adapt to risk profiles in real time. This ensures that the right level of scrutiny is applied according to the risk, reducing unnecessary friction for low-risk customers while focusing resources on high-risk cases.

Automated alerts and task management features help compliance teams stay on top of deadlines and regulatory changes, fostering a culture of proactive risk management. Additionally, InvestGlass’s audit-ready reporting functionality simplifies regulatory reporting and internal reviews, providing transparent evidence of AML compliance efforts.

Our expertise in Swiss-sovereign CRM shows that automating EDD workflows not only reduces operational costs but also significantly enhances accuracy and regulatory adherence. This positions financial institutions to better manage risk and maintain trust with regulators and customers alike.

Wnioski

In conclusion, enhanced due diligence is an indispensable process for managing high-risk customers and ensuring strict AML compliance. It requires a thorough risk assessment and detailed customer due diligence that goes beyond standard verification procedures. While the complexity of EDD can pose challenges, automating these workflows through platforms like InvestGlass offers a powerful solution.

Our experience demonstrates that integrating intelligent automation reduces human error, accelerates onboarding, and ensures continuous monitoring: all essential for effective compliance management. As regulatory expectations evolve, leveraging a sophisticated CRM and digital onboarding platform ensures financial institutions remain resilient and compliant.

For organizations committed to maintaining the highest standards of due diligence, InvestGlass provides a comprehensive, scalable platform designed to meet and exceed regulatory demands seamlessly.

Często zadawane pytania (FAQ)

1. What is enhanced due diligence (EDD)?

Enhanced due diligence is a more detailed and rigorous process of verifying a customer’s identity and risk profile, especially for those deemed high risk. It involves additional checks and ongoing monitoring to comply with AML regulations.

2. When is EDD usually required?

EDD is typically required for high-risk customers such as politically exposed persons (PEPs), clients from high-risk jurisdictions, or those with complex ownership structures. It is also necessary when transactions appear suspicious or unusually large.

3. How does InvestGlass help with EDD?

InvestGlass automates EDD workflows by integrating risk assessment tools, dynamic data collection, and automated alerts, streamlining the entire process while maintaining compliance with regulatory standards.

4. What types of customers are considered high risk?

High-risk customers include those linked to politically exposed persons, clients from countries with weak AML laws, businesses with complex ownership, and individuals engaged in high-value or cross-border transactions.

5. How does EDD differ from standard customer due diligence?

Standard customer due diligence (CDD) involves basic identity verification and risk assessment, whereas EDD requires deeper investigation, including source of funds verification, enhanced monitoring, and more comprehensive documentation.

6. Can EDD be fully automated?

While some aspects of EDD require human judgment, many procedural tasks such as data collection, risk scoring, and alert generation can be effectively automated using platforms like InvestGlass.

7. Why is ongoing monitoring important in EDD?

Ongoing monitoring ensures that any changes in a customer’s risk profile or suspicious activities are detected promptly, allowing institutions to take timely action to mitigate risks.

8. How does InvestGlass support AML compliance?

InvestGlass supports AML compliance by providing a secure, scalable platform that automates due diligence processes, maintains audit trails, and generates regulatory reports, reducing compliance risks.

9. What role does risk assessment play in EDD?

Risk assessment identifies customers who pose higher risks, allowing institutions to apply the appropriate level of due diligence, ensuring resources focus on the most critical areas.

10. Is InvestGlass suitable for all types of financial institutions?

Yes, InvestGlass is designed to be flexible and scalable, making it suitable for a wide range of financial institutions, from wealth managers to banks, seeking robust AML compliance and digital onboarding solutions.

For organizations seeking to optimize their compliance programs and simplify complex due diligence processes, InvestGlass offers a cutting-edge solution tailored to the demands of modern financial regulation. Discover how our platform can transform your enhanced due diligence workflows today. Visit InvestGlass to learn more.

Powiązane artykuły

Szwajcarski CRM suwerenny: Oparty na sztucznej inteligencji.

Gotowy do działania.