Principaux enseignements

- Regulatory compliance means following binding laws and compliance regulations such as GDPR, MiFID II, FINMA circulars, the FCA Handbook, SEC rules and local AML laws.

- The consequences of non compliance now routinely include financial penalties in the tens or hundreds of millions, criminal liability for executives, operational restrictions and long term reputational damage.

- Companies ensure regulatory compliance most effectively through an integrated compliance program that combines policies, training, monitoring, internal controls and technology such as InvestGlass compliance workflow software.

- InvestGlass offers a Swiss sovereign CRM and compliance management platform for financial institutions seeking a non American or Chinese solution that protects data security and client sovereignty.

- In 2026, regulatory compliance management must be continuous, measurable and embedded into daily business processes, not stored in static policy manuals.

Regulatory expectations are becoming stricter, faster and more operational. For banks, wealth managers, insurers and fintechs, regulatory compliance important decisions now affect onboarding, client communication, portfolio advice, cyber security, outsourcing and board reporting.

What is regulatory compliance in financial services?

Regulatory compliance refers to adherence to external laws, rules and compliance standards set by regulatory bodies such as FINMA, the FCA, ESMA, the SEC, central banks and other major regulatory agencies. A practical regulatory compliance definition is this: regulatory compliance is the process of adhering to laws, regulations, policies, and procedures established by governments and regulatory bodies relevant to an organization’s industry.

In financial services, regulatory compliance describes the way firms meet binding external legal mandates across anti money laundering and counter financing of terrorism, KYC, customer due diligence, data security, privacy, conduct of business, capital adequacy and reporting. Compliance regulations in 2026 include the EU’s MiFID II and MiFIR, the UK Senior Managers and Certification Regime, the general data protection regulation, the Swiss Anti Money Laundering Act and Basel III capital standards.

Regulatory compliance is different from corporate compliance. Regulatory compliance requirements come from applicable regulations, government agencies and supervisory authorities. Corporate compliance covers internal codes, ethical values, governance processes and internal policies that translate those external obligations into daily behaviour.

InvestGlass is built to help regulated institutions embed regulatory compliance into client lifecycle management, digital onboarding, KYC, portfolio monitoring and audit ready record keeping as part of an all in one platform for sales automation and CRM.

Core compliance regulations and standards financial firms must know

Financial firms in Europe, the UK, Switzerland, the Middle East and global hubs face overlapping compliance laws and industry specific regulations. The most relevant compliance frameworks include:

- Financial markets regulation: MiFID II and MiFIR for investor protection, suitability, transparency and reporting; Basel III for capital and liquidity; EMIR for derivatives; PRIIPs for packaged investment products.

- Data privacy and data security: GDPR, UK GDPR, Switzerland’s revised FADP, and the digital operational resilience act for ICT risk and incident reporting. The EU’s GDPR applies to any organisation that processes data of EU citizens, regardless of the organisation’s location.

- AML and KYC: the EU AML package, the 5th and 6th AML Directives, FATF recommendations, the UK Money Laundering Regulations 2017 and Swiss FINMA AML ordinances, as well as French LCB FT frameworks for anti money laundering and terrorism financing.

- Security and assurance standards: PCI DSS for payment card data, ISO 27001 for information security management systems, SOC 2 reporting and local conduct rules from regulators such as the FCA and SFC in Hong Kong.

- US and cross sector laws: In the US, the financial industry is governed by legislation including the Dodd-Frank Act and the sarbanes oxley act, which impose strict compliance requirements to enhance transparency and accountability. The federal trade commission is also a federal regulatory agency relevant to privacy, consumer protection and unfair practices.

- Other regulated industries: The health insurance portability and accountability act regulates the protection of health information. The portability and accountability act is often referenced through hipaa regulations, and healthcare organizations must protect patient data. The phrase insurance portability and accountability is central to that framework, while the accountability act element highlights the need for documented controls. The california consumer privacy act also shows how privacy obligations extend beyond Europe. Outside finance, the national institute of standards and technology, occupational safety, workplace safety, occupational health, health administration and safety administration obligations shape compliance in other sectors, and even specialised domains such as Swiss CRM solutions for dental practices et practice management platforms for therapists in Switzerland must embed privacy and compliance by design.

Many regulations exist specifically to protect sensitive information. Adhering to standards helps organizations secure personally identifiable information and financial records from cyber threats, security breaches and operational misuse.

InvestGlass supports the mapping of regulatory compliance requirements to concrete controls, including KYC checklists, suitability questionnaires, risk scoring, automated approvals and sovereign Swiss hosted records.

Regulatory compliance in Europe, the UK and Switzerland

Companies operating in or serving clients in Europe face layered compliance obligations at EU, regional and national levels. Cross border firms must identify applicable regulations by client domicile, booking centre, legal entity and product type.

- European Union: MiFID II, GDPR, DORA and the Markets in Crypto Assets Regulation apply across member states. MiCA is phased in from 2024 to 2026, with crypto asset service providers under transitional provisions needing authorisation by 1 July 2026, according to European regulatory deadline analysis. Full application of the revised AML package is expected on 10 July 2026.

- United Kingdom: The FCA and PRA supervise financial institutions under a post Brexit regime. SMCR imposes individual accountability, Consumer Duty has applied since July 2023, and UK GDPR governs personal data.

- Switzerland: FINMA supervises banks, insurers, asset managers and other regulated firms. FinSA and FinIA came fully into force in 2020, while the revised FADP, effective since 2023, strengthens Swiss data protection. Local hosting is increasingly important for financial data and sensitive data.

Cross border firms benefit from centralised compliance management that records which laws and regulations apply to each client relationship. InvestGlass’s Swiss hosting and optional on premise deployment help institutions meet EU and Swiss data residency expectations while avoiding dependence on American or Chinese cloud infrastructure.

Compliance obligations across key financial sectors

Compliance requirements vary significantly by sector. Different industries face distinct regulatory obligations based on their risk exposure, data handling requirements, and societal impact, with specific regulations such as HIPAA for healthcare and GDPR for data protection in the EU.

- Retail and private banking: Banks must manage KYC, transaction monitoring for AML, sanctions screening against EU, OFAC and UN lists, suitability and appropriateness tests, and periodic client reviews.

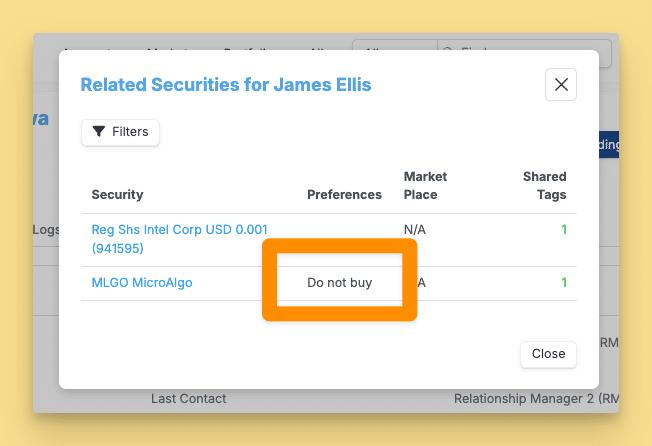

- Wealth and asset management: Firms need MiFID II suitability assessments, product governance, ESG disclosures under SFDR and best execution policies. Detailed client profiling in the CRM is essential, particularly for private banks using specialised CRM platforms.

- Insurance and bancassurance: Firms must comply with IDD, conduct rules, disclosure obligations and documentation of client advice and consent.

- Fintechs and neobanks: Platforms must address PSD2, open banking, strong customer authentication, ISO 27001, SOC 2, cloud outsourcing rules and, where relevant, MiCA, often relying on automated KYC verification in digital onboarding and robust KYC compliance frameworks for crypto businesses in Switzerland.

InvestGlass can be configured by sector so each business line sees customised onboarding journeys, risk scoring models, approval routes and checklists that reflect specific regulatory compliance requirements, supported by a Swiss CRM for financial sales and marketing teams.

Why regulatory compliance matters in 2026

Since the global financial crisis and multiple high profile data breaches, regulators have increased both the volume and intensity of compliance expectations. Anti-money laundering laws and the Sarbanes-Oxley Act prevent fraud and ensure financial transparency, while modern privacy and resilience rules require firms to prove control over systems and data.

- Legal and financial consequences: Non-compliance can lead to severe penalties, including monetary fines that can reach up to €20 million or 4% of annual global turnover under GDPR for serious violations. Non-compliance can lead to severe monetary penalties, with fines under regulations like GDPR reaching up to €20 million or 4% of annual global turnover, whichever is greater. In 2025, the FCA levied over £124 million in fines for AML and financial crime control failures, according to FinTech Global. BaFin also fined J.P. Morgan SE €45 million for delayed suspicious transaction reporting.

- Reputation and trust: Regulatory compliance is crucial for maintaining trust and goodwill among clients and business partners, as it ensures that businesses operate fairly and ethically. Reputation losses are a significant consequence of non-compliance, as negative publicity can erode customer trust and lead to long-term revenue declines.

- Operational disruption: Organizations that fail to comply with regulations may face business disruptions, including suspension of operations, legal actions, and increased scrutiny from regulatory bodies. Non-compliance can result in operational restrictions, such as being barred from bidding on government contracts or serving customers in certain markets, leading to loss of business.

- Cyber and remediation costs: The average cost of a data breach in 2021 was approximately USD 4.24 million, highlighting the financial implications of non-compliance with regulatory standards. Non-compliance can also trigger costly remediation efforts or long-term auditing processes that drain corporate resources, prompting many banks to explore agentic AI for fraud detection and operational resilience.

- Business quality: Effective compliance programs help prevent legal sanctions, financial losses, and reputational damage while improving operational efficiency. Organizations that maintain regulatory compliance can experience increased profitability due to streamlined workflows, improved employee efficiency, and reduced exposure to fines and legal issues.

Regulators increasingly expect compliance audit evidence, board reporting and continuous risk based monitoring. InvestGlass was designed to turn compliance from a manual burden into a controlled operating model that supports faster, safer onboarding.

Role of the compliance officer and compliance function

The compliance officer, often the Chief Compliance Officer, is responsible for setting up and implementing the regulatory compliance policy or program within an organization. Regulatory compliance impacts multiple roles across an organization, not just compliance teams, and is essential for protecting stakeholders and maintaining operational integrity.

- The compliance officer often implements best practices to ensure compliance and minimize the risk of fines and penalties for non-compliance by developing and publishing the organization’s regulatory compliance policy.

- The compliance officer interprets regulatory changes, drafts and updates policies, runs compliance programs and advises the board and senior management.

- Day to day compliance activities include approvals for high risk clients, review of marketing materials, suspicious activity reporting, sanctions escalation and responses to regulator enquiries.

- The compliance officer is tasked with performing periodic internal audits to assess the organization’s compliance status and ensure adherence to regulatory requirements.

- Compliance officers are responsible for training employees in regulatory compliance to ensure they understand their responsibilities and can act accordingly during security incidents.

Compliance management is increasingly collaborative. Legal, risk management, IT security, data protection officers and front office managers must work together through cross functional committees.

InvestGlass gives compliance officers dashboards, automated alerts, time stamped approvals and audit ready records, reducing reliance on spreadsheets and fragmented systems. For smaller firms without large compliance teams, InvestGlass embeds compliance tasks into adviser and relationship manager routines.

Building an effective regulatory compliance program

A compliance program is the structured set of policies, controls, training and monitoring activities used to ensure regulatory compliance. An effective regulatory compliance program typically follows a structured approach that helps organizations move from reactive compliance to proactive risk management.

- Appoint ownership: To implement a compliance program, organizations should appoint a compliance officer, identify applicable regulations, conduct a gap analysis, and train employees on compliance requirements.

- Approve policy: A written regulatory compliance policy should be approved by the board and explain compliance obligations, roles, escalation routes and consequences of non compliance.

- Assess risk: Conduct risk assessments at least annually by product, geography and client segment. Regularly assess the organization’s operations to identify potential compliance gaps and risks.

- Implement controls: Standardised onboarding, four eyes approval, transaction monitoring, stringent data security controls and clear exception handling help firms achieve regulatory compliance.

- Train employees: Conduct ongoing training to ensure staff understand compliance policies, ethical values, and specific guidelines that govern their roles.

- Monitor and test: Implement monitoring systems to ensure that compliance procedures are followed. Continuous monitoring and internal audits are essential components of a compliance program, helping organizations assess their adherence to regulatory requirements and identify areas for improvement.

To ensure regulatory compliance, a company must actively identify its legal obligations, establish clear internal policies, implement controls, and continuously monitor operations. Maintaining compliance helps organizations avoid unnecessary legal issues, as regulatory frameworks ensure that all necessary legal obligations are met, significantly reducing the risk of costly penalties.

InvestGlass can host policies, training acknowledgements, control workflows and evidence in one environment, making the compliance program measurable rather than static.

How companies ensure regulatory compliance in daily operations

Policies only work when translated into daily business operations. Companies ensure regulatory compliance by embedding compliance processes into the systems used by advisers, relationship managers, operations teams and compliance staff.

- Digital onboarding: KYC and suitability questionnaires should be built into onboarding so accounts cannot open before mandatory compliance data is captured and approved.

- Screening: Automated checks should cover sanctions, PEP lists and adverse media, with outcomes recorded for future compliance audits.

- Workflow automation: Tasks, exceptions, maker checker rules and escalations should be handled through workflow logic, not informal email chains.

- Quality assurance: Regular internal compliance audits should include random file reviews and thematic checks on cross border rules, data security practices and product suitability.

- Continuous improvement: Maintaining compliance requires review of incidents, complaints, monitoring alerts and audit findings.

InvestGlass compliance management features include configurable approval flows, time stamped logs, Swiss hosted document storage and centralised client records. These functions help firms prove they follow their compliance programs consistently.

Data security, privacy and sovereignty as pillars of compliance

Data security and privacy are now central to regulatory compliance laws, particularly under GDPR, FADP and sector specific rules in finance and insurance. The phrase data protection regulation gdpr is often used in operational discussions because privacy obligations now affect marketing, onboarding, retention, outsourcing and reporting.

- Core controls: Least privilege access, encryption in transit and at rest, strong authentication, monitoring of access logs and review of unusual activity are essential data security controls.

- Privacy by design: Firms need data minimisation, consent capture, retention policies and robust responses to data subject access requests within legal deadlines.

- Sovereignty: Regulators and clients increasingly expect sensitive data, financial data and personal information to remain within trusted jurisdictions.

- Incident readiness: Firms must plan for data breach response, escalation and notification. Poorly managed security breaches create legal consequences, financial penalties and client distrust.

InvestGlass is a Swiss sovereign CRM and automation platform that can be hosted entirely in Switzerland or deployed on premise. It is an attractive alternative for organisations that wish to avoid American or Chinese hosting and retain control over client data.

By consolidating CRM, onboarding, portfolio management and client portal activity in InvestGlass, firms reduce data fragmentation and apply consistent privacy and security controls across the full client lifecycle.

Using technology and automation to reduce compliance risk

Compliance risk increases when processes are manual, fragmented or undocumented. Technology can reduce errors, lower costs and improve audit readiness, provided governance remains clear.

- Modern RegTech and CRM platforms can collect and validate client data, trigger risk scoring and maintain an immutable audit trail of every change and approval.

- Real time dashboards show outstanding tasks, expiring KYC reviews, missing documents and high risk clients requiring attention.

- AI assisted monitoring can identify anomalies in behaviour, transaction patterns or documentation. Human oversight remains essential, especially as EU AI Act requirements apply to high risk systems from 2 August 2026.

- Integrated systems reduce transfer risks between CRM, onboarding, document storage, portfolio management and client portals.

InvestGlass integrates CRM, digital onboarding, portfolio management and compliance workflow software in one sovereign environment. This avoids many integration and data transfer risks common with multi vendor, cloud hosted American or Chinese solutions.

Because InvestGlass can be tailored to local rules and languages, institutions operating across several jurisdictions can run one sovereign platform while configuring different compliance programs by country, entity or booking centre.

Measuring the effectiveness of your compliance program

Regulators increasingly expect firms to prove their compliance program is effective, not merely documented. Strong metrics show whether controls are working.

Typical regulatory compliance KPIs include:

Zone | Example metric |

|---|---|

KYC | Percentage of up to date KYC files |

Formation | Completion rates for mandatory training |

Contrôle | Number and severity of internal breaches |

Audit | Time to remediate audit findings |

Risque | Number of overdue high risk client reviews |

Formal reporting to the board and senior management should occur at least quarterly and cover compliance risk trends, open issues, regulatory developments, resource needs and remediation status. |

External assurance through compliance audits and regulatory examinations requires organised evidence. System logs, document histories, approval records and exception reports reduce disruption during reviews.

Regulatory compliance fosters healthy competition by eliminating unfair monopolies, encouraging innovation, and motivating organizations to offer superior products and services. Adhering to regulatory compliance requirements can enhance an organization’s branding and public relations, as it increases stakeholder confidence and demonstrates a commitment to ethical practices.

InvestGlass can generate structured reports, export audit trails and surface KPI dashboards for boards and compliance committees, making ongoing compliance easier to demonstrate.

Why a Swiss sovereign platform like InvestGlass is ideal for regulatory compliance

Institutions subject to strict compliance regulations increasingly seek technology partners aligned with their sovereignty expectations, risk appetite and regulatory requirements.

- Swiss hosting and on premise control: InvestGlass gives organisations control over where and how client data is stored, supporting European, Swiss and Middle Eastern privacy and outsourcing expectations.

- Compliance ready modules: InvestGlass includes digital onboarding and KYC workflows, CRM for banks and wealth managers, portfolio management with suitability checks and a secure client portal for document delivery.

- European alternative: InvestGlass is a European alternative to large American and Chinese platforms, designed for regulated industries that do not want sensitive client data exposed to foreign jurisdictions.

- Reduced complexity: By consolidating compliance programs, client interactions and portfolio data, InvestGlass improves data security and supports a more robust corporate compliance framework.

- Audit readiness: Time stamped records, configurable workflows, approval trails and dashboards help firms show that compliance obligations are understood and controlled.

Organisations reviewing their compliance management tools in 2026 should ask whether their current providers align with their data sovereignty, resilience and regulatory expectations. InvestGlass offers a future proof, sovereign option for regulated institutions that want control, security and operational efficiency.

Frequently asked questions about regulatory compliance

What is regulatory compliance in simple terms?

Regulatory compliance means following the laws and rules that apply to your business. In financial services, this includes how firms onboard clients, prevent money laundering, protect data, communicate risks and treat customers fairly.

It is not enough to have written policies. Financial institutions must show that AML, KYC, data security, transparency and fair treatment controls work in practice.

A well implemented compliance program helps avoid fines, protects clients and staff, and gives owners and directors greater confidence in daily operations.

Is regulatory compliance only a concern for large banks?

No. Regulatory compliance applies to organisations of all sizes, from independent wealth managers to global banks and fintech start ups.

A small advisory firm may still face GDPR obligations if it processes personal data, and AML obligations if it handles client funds or provides regulated financial services.

Smaller firms often rely on platforms such as InvestGlass to achieve stronger compliance management with lean teams, using structured workflows rather than large manual departments.

How often should a financial firm perform a compliance audit?

Internal compliance audits are typically performed at least annually. Higher risk areas, such as AML monitoring, high risk clients, cross border activity and cyber security, may need quarterly or semi annual review.

Regulators can also conduct inspections on a multi year cycle or in response to incidents. Firms should therefore remain audit ready at all times.

InvestGlass centralises records, time stamped workflows and document evidence, helping teams respond quickly to audit requests.

What are typical consequences of non compliance in finance?

Consequences of non compliance include warning letters, remediation programmes, restrictions on new business, substantial monetary fines, loss of licence and, in severe cases, criminal charges for individuals.

Recent AML enforcement across Europe and the UK shows that fines can reach tens or hundreds of millions. GDPR penalties for poor privacy controls can reach €20 million or 4% of annual global turnover.

Beyond headline fines, long term reputational damage, client outflows and increased supervisory scrutiny can be even more costly.

How does InvestGlass help with regulatory compliance specifically?

InvestGlass embeds compliance requirements directly into CRM, onboarding and portfolio processes. It supports configurable KYC forms, suitability questionnaires, approval workflows, document collection and client review cycles.

The platform provides Swiss data hosting, optional on premise deployment, audit trails and dashboards for compliance officers and senior management.

For institutions seeking sovereign control over client data while using advanced automation and AI for compliance management, InvestGlass offers a secure European alternative to American and Chinese platforms.

Articles connexes

Swiss Sovereign CRM : Construit sur l'IA.

Prêt à agir.