Principais conclusões

- A serviços bancários request for proposal rfp is a structured process to compare potential providers objectively across financial institutions.

- A mid-sized bank request for proposal in 2026 typically runs 10 to 14 weeks from planning to contract signing, while many projects take 10 to 12 weeks depending on complexity.

- Clear evaluation criteria, weighting factors, and an evaluation matrix help organisations choose the right banking services provider, not simply the lowest fees.

- European and Swiss solutions such as InvestGlass help banks, wealth managers, foundations, and public bodies protect client sovereignty and avoid dependence on American or Chinese technology ecosystems.

- This article focuses on practical governance, documentation, decision making, and controls that finance, treasury, procurement, IT, legal, risk management, and human resources teams can apply immediately.

Introduction: Why Banking RFPs Matter in 2026

Public bodies, corporates, a nonprofit organization, pension schemes, and wealth managers usually review banking services every 3 to 5 years. The rfp process helps an organization reduce banking costs by ensuring that service providers offer competitive rates and by identifying the vendor that best matches its culture, atendimento ao cliente, and technology needs.

In 2026, real-time payments, ISO 20022 migration, cyber security, GDPR, PSD2, DORA, and data residency have made the banking services rfp more demanding, especially in Europe and the UK. This guide is written in British English for finance directors, treasurers, operations leaders, board members, and regulated institutions seeking a transparent, auditable selection.

A InvestGlass é uma empresa suíça soberano CRM and automation platform. It supports banks and financial institutions before, during, and after an rfp by centralising communications, documents, scoring, onboarding, KYC, portfólio workflows, and client data in Swiss hosted or on-premise infrastructure.

Banking RFP Basics

A banking request for proposal is a questionnaire xls, word or pdf and formal process issued to prospective vendors by an institutions seeking banking product..

Typical triggers include contract expiry, higher fees, mergers, poor support, new payment rules, multi-currency needs, or cross-border services. A general banking services rfp may cover accounts, payments, liquidity, and cash management. A focused rfp may address FX, custody, merchant acquiring, escrow, trade finance, or digital channels.

For public sector entities and pension funds, an rfp is often required by procurement rules. The RFP process ensures that banks make transparent, fiduciary decisions and creates an audit trail for the board.

What Is an RFP in Banking?

A request for proposal rfp in banking is a structured written invitation sent to selected banks asking for a complete proposal on specified banking services.

It typically asks for:

- Pricing schedules and fee structure

- Implementation plans and service level agreements

- Technology architecture, APIs, host-to-host connectivity, and ISO 20022 readiness

- Online banking, security, data privacy, and compliance history

- Relationship management structure, qualifications, and escalation support

An RFP improves comparability because respondents answer the same questions, using the same assumptions, deadlines, and formats. An RFI is used to explore the market, while an RFQ is narrower and price-led.

Why Organisations Issue Banking RFPs

The RFP process is essential for organisations to periodically evaluate their current banking service provider and ensure they receive the best value and services available in the marketplace.

The motives are usually mixed:

- Financial: reduce transaction charges, benchmark fees, improve yield, and consolidate accounts.

- Risk and compliance: evaluate capital strength, resilience, cyber controls, security certifications, and regulatory conduct.

- Strategic: improve digitisation, straight-through processing, CRM integration, ERP links, and gerenciamento de portfólio.

- Governance: document decision making for audit, public money, pension assets, client funds, and investment committees.

Financial institutions also use RFPs to select correspondent banks, custodians, technology partners, and qualified investment service providers.

Planning a Bank Request for Proposal

Careful planning in the 3 to 4 weeks before issue reduces unclear responses and rework. Interview stakeholders who regularly interact with banking service providers to gather insights and define the scope and priorities for the RFP.

Create a steering team from treasury, finance, procurement, IT, legal, risk, operations, and relevant front-office users. Decide whether the request covers all services in one lot or separates payments, deposits, lending, FX, and specialist services.

Defining Scope, Objectives, and Budget

A comprehensive banking RFP requires information on the current banking environment, including existing relationships and transaction volumes. Include the number of accounts, currencies, average balances, annual fees paid, transaction types, and pain points.

A well-structured finance RFP includes defined organisational financial goals and detailed specifications for candidate institutions. Set measurable objectives, such as a target fee reduction, credit rating threshold, maximum implementation period, or digital capability by 2027. Define the contract term, usually 3 to 5 years, options for extension, budget caps, subsidiaries in scope, and ESG priorities.

Governance, Roles, and Responsibilities

Appoint one project lead, often a treasury manager or operations head, to manage the project, calendar, document control, clarification register, and all communications.

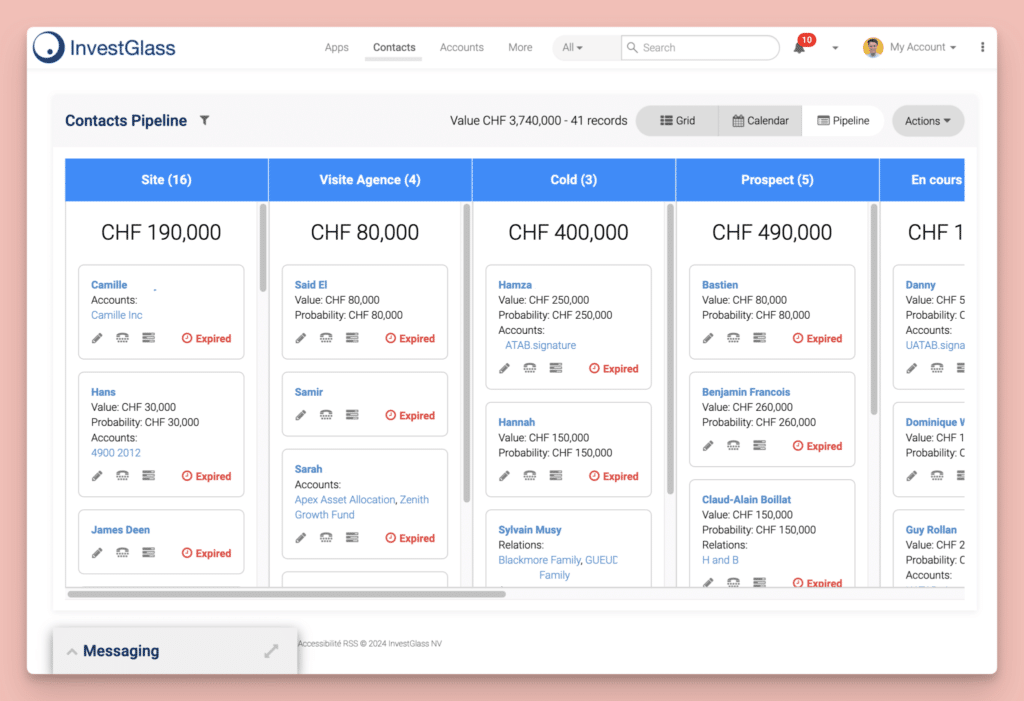

The evaluation committee should include people with expertise in finance, IT, legal, procurement, risk, and daily bank operations. Establish conflict rules, decision rights, escalation paths, and who will present the final decision to the board. A secure, access-controlled platform such as InvestGlass is preferable to scattered email threads.

How to Draft a Banking Services RFP Document

Most value is created when drafting the document. A typical 2026 banking services rfp is 25 to 60 pages plus appendices, with plain British English, numbered questions, pricing spreadsheets, and clear submission guidelines.

RFPs provide a project overview, which is a brief description of the organisation and the primary goals of the RFP. The RFP should provide information about the organisation, including its mission, structure, long-term goals, and any relevant policies or performance reports to help potential providers understand its needs.

Essential Sections of the Banking RFP

Incluir:

- Executive summary: purpose, dates, objectives, and contact person.

- Organisational overview: legal structure, history, locations, clients, turnover, assets, and priorities.

- Current banking environment: existing banks, accounts, transaction volumes, and issues.

- Services requested: current accounts, payments, liquidity, FX, cards, trade finance, or escrow.

- Proposal instructions: confidentiality, formatting rules, number of required copies, submission portal, deadlines, and answer format.

Technical, Security, and Integration Requirements

The financial industry is heavily regulated, necessitating vendors to detail their security postures, data privacy policies, and compliance history in RFPs. Security and compliance protocols are critical elements that banks need to address in RFP submissions.

Ask about multifactor authentication, user controls, audit trails, APIs, cut-off times, file formats, SEPA, UK Faster Payments, ISO 20022 pain and camt messages, disaster recovery, data processing locations, and cloud subcontractors. In Europe, include DORA expectations on ICT risk and third-party oversight, guided by the European Banking Authority’s DORA information.

Pricing, Service Levels, and Implementation

Request a detailed pricing template by account type, transaction type, channel, ancillary service, and one-off implementation costs. This supports like-for-like comparison and helps determine total cost.

Define service levels for system availability, payment processing, support response, incident handling, and file cut-offs. Ask each respondent to provide an implementation plan with milestones, resources, testing, training, documentation, named contacts, and a go-live window, por exemplo Q4 2026 to Q2 2027.

Running the Banking RFP Process

Typical steps are issue, Q&A, response receipt, completeness review, longlist, shortlist, finalist presentations, negotiation, and recommendation. Allow at least 4 weeks for banks to respond and 2 to 3 weeks for internal evaluation.

Issuing the RFP and Managing Q&A

Invite 4 to 8 suitable institutions based on credit strength, geography, capabilities, and whether a US bidder is member fdic where applicable. Send the rfp through a secure portal or encrypted channel.

Set a clarification deadline about 10 days after issue. Publish consolidated questions and answers to all interested banks. Avoid side conversations and keep a single register of all responses.

Evaluating Responses and Scoring

Perform a completeness check first. Establishing clear evaluation criteria and weighting for proposals is crucial in the RFP process, as it allows organisations to score and compare responses objectively, ensuring a fair selection of banking services providers.

An RFP for banking services should include an evaluation matrix with specific weighting criteria for scoring proposals. When developing benchmarks for evaluating RFP responses, organisations should start with criteria that can be scored objectively and applied consistently to each proposing bank. Establishing weighting for each evaluation criterion is crucial, as it allows organisations to prioritise what matters most to them, such as cost, service quality, or specific capabilities.

Score cost, service quality, technology, security, relationship support, implementation, and resilience. InvestGlass CRM can store scores, comments, attachments, and audit records securely.

Selecting Finalists and Conducting Interviews

Shortlist 2 to 4 finalists. Finalist interviews are an important part of the vendor selection process, allowing organisations to assess the expertise of potential service provider teams and their fit with the organisation.

Use the same agenda for every banking services provider. Evaluate culture, contingency planning, escalation paths, and case studies for similar clients. Site visits can be helpful for large mandates.

Choosing and Onboarding the Banking Services Provider

This stage turns analysis into mandate. The committee should recommend a preferred partner and explain why others were rejected. That record protects the organisation if the decision is challenged.

Final Recommendation and Governance Approval

Prepare a board paper covering the process, evaluation, criteria, scores, risks, costs, and rationale. Attach scoring matrices and key response extracts. Public bodies may need formal resolutions, while private companies record approval in minutes.

Contracting, Migration, and Performance Monitoring

Negotiate fees, SLAs, indemnities, termination rights, data protection, and audit clauses. Build a migration plan covering account opening, payment file tests, user training, phased volumes, and client communications.

Track KPIs such as availability, payment rejection rates, response times, incidents, and satisfaction. Review performance quarterly and formally after 12 months.

Technology, Data Sovereignty, and the Role of InvestGlass

Modern banking services are inseparable from data, workflow, and technology platforms. Many European institutions now question reliance on American or Chinese cloud and CRM providers for sensitive financial data.

InvestGlass is not a banking services provider. It is a Swiss sovereign CRM and automation platform that helps regulated organisations manage the RFP lifecycle, client data, onboarding, compliance workflows, portfolio management, and secure portals while protecting sovereignty.

Protecting Client Data Sovereignty in Banking RFPs

RFPs increasingly ask where client and transaction data is stored, processed, and backed up. InvestGlass offers Swiss hosting and on-premise deployment, helping organisations maintain control over CRM and client interaction data.

Include questions about foreign cloud reliance, encryption keys, subcontractors, data residency, and extraterritorial access. This is especially relevant for private banks, asset managers, insurers, public bodies, and any institution managing sensitive client records.

Using InvestGlass to Support the Banking RFP Lifecycle

InvestGlass can store bidding bank contacts, track communications, manage evaluation scores, preserve documents, and provide a secure audit trail. After selection, it can support integração digital KYC, portfolio management, client communications, and integrations with the selected bank.

For organisations seeking a non-American and non-Chinese solution, InvestGlass provides a sovereign technology foundation that protects the sovereignty of the client and keeps strategic data under controlled infrastructure.

PERGUNTAS FREQUENTES

How often should an organisation run a banking services RFP?

Many organisations review core banking services every 3 to 5 years, or sooner after a merger, regulatory change, fee increase, service failure, or major technology shift.

How many banks should be invited to a banking RFP?

Inviting 4 to 8 financial institutions is usually sufficient. Too many respondents can stretch internal resources and weaken engagement with the strongest providers.

What internal resources are needed to manage a banking RFP?

You need an RFP project lead, finance or treasury specialists, IT integration expertise, legal counsel, risk or compliance officers, and daily bank users. A medium-complexity project may require 60 to 100 combined staff hours.

Can smaller organisations run a banking RFP without external consultants?

Yes. Many mid-sized companies, charities, and wealth managers can manage the process internally with templates, governance, clear scope, and disciplined evaluation. Advisers are helpful for complex, multi-country, or highly technical mandates.

Why should we consider a sovereign platform like InvestGlass alongside our banking RFP?

A sovereign CRM and automation platform helps keep client and portfolio data in Swiss or self-controlled infrastructure, independent of American or Chinese software providers. This improves resilience, regulatory confidence, and flexibility in future RFP cycles.

Artigos relacionados

Swiss Sovereign CRM: Construído com IA.

Pronto para agir.