Institutions financières operate in an increasingly connected world where a single security incident can quickly damage customer trust and lead to multi-million dollar penalties. In the financial sector, such breaches can significantly harm client confidence and tarnish the reputation of these institutions. Protecting client data requires a combination of governance, technology, and organisational culture rather than relying on any single tool or policy. These organisations have a legal duty to protect customer information as a core regulatory and trust obligation. Sensitive client data includes personal identification details, transaction records, and bank account information, all highly susceptible to cyber threats. Regulations like the Gramm-Leach-Bliley Act (GLBA) require organisations to disclose their information-sharing practices and implement comprehensive security programmes to safeguard customer data. Industry regulations play a vital role in shaping data protection practices and ensuring secure data management. Swiss data sovereignty and options for on-premise hosting offer strategic advantages for institutions serving privacy-conscious clients.

A contemporary CRM tailored for regulated sectors, such as InvestGlass, can centralise onboarding, portfolio data, and communications while enforcing consistent protection measures. These systems are crucial for protecting financial data and safeguarding sensitive information in line with regulatory requirements. This article offers a practical framework for CISOs, COOs, and compliance officers to advance their data protection maturity in 2024 and beyond.

Introduction

In 2019, Capital One suffered one of the largest data breaches in the financial industry when a misconfigured cloud environment exposed approximately 100 million customer records. The aftermath included $190 million in fines and class action settlements, significant reputational damage that took years to repair, and a stark reminder that even well-resourced financial institutions can fail to protect sensitive financial data. This incident was not unique. Banks, wealth managers, and insurers hold decades of transaction histories, identity documents, and suitability data for every client, making their CRM and core banking systems prime targets for attackers.

Sensitive financial client data extends far beyond payment card information. It includes KYC documents, passport scans, tax reports, portfolio holdings, bank account details, communication histories amassed over long-term relationships, and financial transactions. To protect this data, financial institutions must implement strong privacy measures such as encryption, strict access controls, and ongoing regulatory compliance. It is vital to safeguard sensitive data during financial transactions and to prevent unauthorized transmission of client information through tools like Data Loss Prevention (DLP) systems. When attackers access this information, they gain everything needed for identity theft, financial fraud, and exposure of sensitive details that can devastate individuals and families.

This article provides a structured guide from the perspective of InvestGlass, a CRM suisse and automation platform serving regulated financial institutions, expanding on how InvestGlass is tailored for private banks and financial services. The focus is on practical measures that small and mid-sized institutions can realistically adopt, not just large banks with unlimited security budgets.

Comprendre les données financières sensibles des clients

Sensitive financial client data includes any non-public personal and financial information that regulators require to be protected with enhanced measures. This covers personally identifiable information like names, addresses, and Social Security numbers, as well as financial details such as account numbers, IBANs, bank account data, portfolio positions, performance reports, and suitability assessments.

Moderne CRM et portefeuille platforms consolidate this sensitive client data into a single client profile. While this consolidation improves service quality and enables personalised advice, it also concentrates risk. A breach of one system can expose all the information an institution holds about a client.

Financial institutions must also manage long data retention periods. MiFID II requires certain records to be kept for five to seven years, while FINMA circulars and AML regulations may extend this to ten years or more. This extended timeframe means the volume of data requiring protection continues to grow.

Catégories de données communes dans les institutions financières :

- Catégorie

- Exemples

- Documents d'identité

- Passeports, permis de conduire, justificatifs de domicile

- Registres financiers

- Relevés de compte, données du titulaire de la carte, historique des transactions

- Évaluations des risques

- Questionnaires d'adéquation, profils de tolérance au risque

- Informations fiscales

- Déclarations de résidence fiscale, formulaires W8/W9

- Communications

- Courriels, notes de réunion, recommandations consultatives

- A clear data classification scheme with labels such as public, internal, confidential, and strictly confidential forms the foundation of any protection strategy. The measures outlined in this article assume such a scheme is already established.

- Applying data minimisation, collecting and retaining only the data strictly necessary for operations or AI model training, helps reduce exposure and risk. This principle limits the amount of sensitive information, such as bank account details, that could be compromised in the event of a breach.

Principales menaces pesant sur les données des clients financiers

In 2024, threat actors targeting financial infrastructure include financially motivated cybercriminals, insiders, and state-sponsored groups. IBM research indicates that the average cost of a data breach in the financial services sector reached $5.9 million, notably higher than the cross-industry average of $4.88 million. The financial sector has accounted for approximately 25 per cent of all reported breaches in recent years.

Cybermenaces externes represent the most apparent risks and consist of:

- Phishing campaigns designed to steal credentials. Phishing attacks trick individuals into disclosing sensitive information through deceptive emails, messages, or counterfeit websites.

- Credential stuffing attacks leveraging leaked password databases

- API exploitation targeting online banking and wealth management portals

- Account takeover schemes exploiting weak authentication mechanisms

- Ransomware attacks that encrypt systems and demand ransom payments. Notably, in 2023, 64 per cent of financial organisations globally reported ransomware incidents, underscoring the importance of robust, layered security controls.

- Malicious software aimed at extracting sensitive information

Antivirus software plays a crucial role in cybersecurity by defending against malware, viruses, and unauthorised access, and is a requirement for compliance with standards such as PCI DSS.

Alongside API abuse and account takeover, cybercriminals also use brute force attacks, SQL injection, and distributed denial-of-service (DDoS) attacks to infiltrate financial systems.

Menaces d'initiés are a significant concern as well. Disgruntled employees might export customer records prior to departure. Relationship managers occasionally circumvent controls by using personal mobile devices for client communications. Even well-meaning staff can mishandle spreadsheets containing customer data, resulting in unauthorised copies outside secure systems. Protecting physical devices like laptops and smartphones is vital, as theft or loss can lead to unauthorised data access.

Third-party risks have grown due to financial institutions’ reliance on cloud services, outsourced KYC providers, third-party vendors, and regtech tools connected via APIs. The SolarWinds incident illustrated how a single compromised vendor affected 18,000 organisations worldwide. Continuous evaluation and access restrictions are essential to mitigate risks from third-party vendors and ensure external partners do not have excessive access to sensitive data.

A newer issue involves generative AI tools. Staff who input client information into consumer chatbots risk inadvertently leaking data. Financial institutions must set clear policies on AI usage to prevent unauthorised disclosure of sensitive information. Data Loss Prevention (DLP) systems are critical for monitoring, detecting, and blocking unauthorised transmission of sensitive data, helping prevent breaches or leaks. Exploring Agentic AI for fraud detection and customer experience in banking illustrates how advanced AI can be harnessed securely rather than through uncontrolled consumer tools. Advanced cyber attacks such as prompt injection and jailbreaking are not addressed by traditional security measures and require novel approaches.

Pourquoi les institutions financières collectent-elles et centralisent-elles les données relatives à leurs clients ?

Regulatory requirements largely drive data collection. KYC and AML mandates under EU AML directives, the Swiss AML Act, and FATF guidelines require capturing identity documents and source of funds information. Leveraging automated KYC verification to streamline this process helps institutions satisfy regulators’ demands for comprehensive documentation while reducing manual workload.

Business needs also promote centralisation. Consolidated portfolio reporting enables relationship managers to offer holistic advice. Client segmentation supports personalised investment proposals and marketing campaigns. Comprehensive customer data allows institutions to anticipate needs and deliver financial products aligned with client objectives, particularly when using a Swiss financial-sector CRM with digital onboarding and portfolio management.

CRM platforms like InvestGlass consolidate onboarding data, risk profiles, product documents, and communication histories into a single system. This centralisation is vital for regulated firms that must maintain audit trails and consistent advice across channels.

This makes the CRM a critical system, containing all information necessary to understand, serve, and potentially harm clients. The controls discussed later must be applied with equal rigor.

Principes de base pour la protection des données financières des clients

Before applying specific controls, institutions should embrace overarching principles guiding their decisions:

Le moindre privilège ensures relationship managers, compliance officers, and external partners access only what is essential. Junior assistants do not need access to all client portfolios, and external auditors do not require real-time trading permissions.

Minimisation des données advocates collecting only data necessary for regulatory compliance and service quality. Avoid storing unnecessary copies in spreadsheets, email archives, or personal drives, as each additional copy increases exposure.

La protection de la vie privée dès la conception integrates data protection considerations into every new onboarding process, mobile app feature, or client portal module from the outset. Security cannot be an afterthought.

Sécurité par défaut means systems come pre-configured with protective settings enabled. Users must deliberately disable these safeguards rather than relying on memory to activate them.

InvestGlass embodies these principles by offering detailed permission settings, flexible data retention options, and audited workflows that automatically enforce compliance policies, even in specialised deployments such as privacy-focused CRM for Swiss dental practices.

Contrôles techniques pour la sécurisation des données financières des clients

Technical controls are essential to any protection strategy but must be tailored to the financial sector’s risk profile. These controls ensure that only authorised individuals can access sensitive financial client data using robust access management and security measures. The primary objective is to protect sensitive data from internal and external threats while maintaining compliance and customer trust.

Cryptage des données

Data encryption secures information both at rest and in transit. AES 256 encryption applied to databases, file storage, and backups ensures stolen media is unreadable without decryption keys. TLS 1.2 or higher encrypts communications between client devices, APIs, and servers.

Advanced encryption standards must anticipate emerging threats. Post-quantum cryptography using lattice-based algorithms like Kyber is expected to become necessary as quantum computing approaches viability around 2030.

Authentification forte

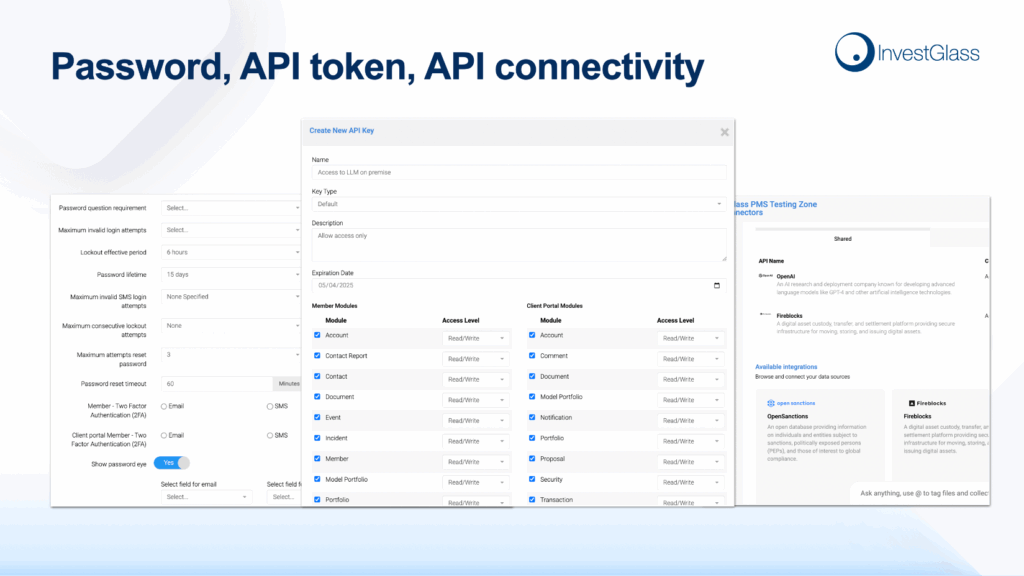

Multi-factor authentication (MFA) should be compulsory for all access to CRM and portfolio tools. Options include hardware tokens, authenticator apps, and biometric logins. The goal is to ensure only authorised users gain access, even if passwords are compromised.

Contrôles d'accès granulaires

Role-based and attribute-based access control enable institutions to define precisely what each user can view. A wealth manager might access portfolio details for assigned clients while an assistant sees only contact information. Access controls apply detailed permissions to ensure only authorised individuals can view or modify sensitive information, including within AI systems. Role-Based Access Control (RBAC) restricts access rights based on roles, ensuring employees see only what their job requires. Strict access controls on the same household enable compliance officers to access different data than relationship managers. Granular access controls limit who can access specific financial data based on roles or permissions, reducing internal leak risks. Implementing strict access controls, including strong password policies and MFA, is vital to protect sensitive financial data.

Contrôle continu

Centralised log collection, anomaly detection, and audit log retention for at least five years support security investigations and regulatory compliance. Security systems should alert on unusual activities such as bulk downloads, access outside business hours, or connections from unexpected locations.

Configuration sécurisée et gestion des correctifs

Application servers, mobile apps, and database clusters require regular security audits and documented change management. Establish regular patch windows and test updates before production deployment, particularly when supporting sensitive use cases like a Swiss CRM platform tailored for therapists.

InvestGlass deployments in Swiss data centres or on-premise include full encryption, MFA enforcement, and IP restrictions for back-office users. This architecture ensures data integrity while providing necessary flexibility.

Articles connexes

Swiss Sovereign CRM : Construit sur l'IA.

Prêt à agir.