Introduction to Banking Compliance

What does compliance mean for banks today? In short, it represents the continuous effort to meet legal, regulatory, and internal obligations across every function of a fi̇nansal kurum. This article provides a practical overview of banking compliance, covering financial crime prevention, data privacy, conduct rules, prudential regulation, and ESG mandates for banks of all sizes.

The stakes have never been higher. Global AML and sanctions fines reached record levels in 2023 and 2024, with enforcement actions against major institutions totalling hundreds of millions. Regulators now share information more aggressively across borders, leading to joint investigations and penalties that transcend national boundaries.

InvestGlass, İsviçreli bir egemen CRM and automation platform, is built specifically to help financial institutions operationalise these obligations. The platform combines dijital işe alım, KYC workflows, portföy yöneti̇mi̇, and compliance automation within Swiss or on-premise infrastructure.

This content is written in British English and focuses on institutions seeking a non-American, non-Chinese, sovereignty-preserving technology stack that korur client data and institutional independence.

What Is Compliance for the Banking Sector?

Banking compliance refers to adherence to the laws, regulations, and internal policies governing all banking activities. This spans customer onboarding, transaction execution, lending, investment advice, and data handling.

Practical expectations differ significantly by business model and jurisdiction:

Business Model | Primary Compliance Focus |

|---|---|

Retail banks | Consumer protection laws, fair lending practices, deposit insurance |

Özel bankalar | Cross-border KYC, tax transparency, suitability assessments |

Investment banks | MiFID II investor safeguards, market abuse prevention |

Fintech-bank partnerships | Licensing requirements, operational resilience |

Landmark frameworks anchor this landscape. Basel III enforces capital and liquidity ratios. FATF sets global AML standards mandating customer due diligence and suspicious activity reporting. The General Data Protection Regulation imposes stringent data protection duties with fines up to 4% of global turnover.

Compliance in banking is now continuous and data-driven rather than a periodic documentation exercise. InvestGlass modules for CRM, digital onboarding, KYC, and compliance workflows help systematise these expectations with full audit trails.

Why Banking Compliance Matters

Regulatory compliance underpins financial stability, consumer protection, and broader economic confidence. The 2008 global crisis demonstrated how lax prudential oversight can precipitate systemic collapse. Recent enforcement waves in 2023 and 2024 show that supervisors continue to pursue institutions with inadequate controls.

Direct consequences of non-compliance include:

- Fines totalling hundreds of millions for deficient transaction monitoring

- Licence restrictions or revocations

- Criminal prosecution of senior management in severe cases

Indirect costs compound these penalties:

- Severed correspondent banking relationships critical for cross-border flows

- Elevated funding costs due to heightened risk perceptions

- Intensified supervisory scrutiny and costlier examinations

Reputational impacts can be devastating. Institutions have lost market share, experienced client exodus, or surrendered licences entirely after major compliance violations. Data breaches and sanctions evasion cases have ended careers and damaged brands permanently.

Conversely, a mature compliance framework delivers competitive advantage. Strong controls foster client trust, particularly among cross-border high-net-worth individuals wary of sovereignty risks. This trust supports acquisition and retention in wealth management and private banking.

Key Regulatory Themes Affecting Banks

Banks must manage overlapping regulatory regimes simultaneously. The five core pillars are prudential rules, conduct standards, financial crime prevention, data protection, and ESG obligations.

Financial Crime Regulation

AML, KYC, CDD, sanctions screening, and transaction monitoring dominate compliance efforts. Key frameworks include:

- FATF recommendations requiring risk-based customer due diligence

- EU AML Directives mandating ongoing monitoring and suspicious activity reporting

- Bank Secrecy Act and PATRIOT Act in the US, requiring documentation to the Financial Crimes Enforcement Network

- Sanctions lists maintained by OFAC, EU, and UN

Banks must conduct regular risk assessments of their exposure to money laundering, terrorist financing, and other financial crimes.

Consumer and Investor Protection

Consumer protection rules vary by jurisdiction:

- US: Truth in Lending Act, Real Estate Settlement Procedures Act, Fair Credit Reporting Act, Electronic Fund Transfer Act

- UK: FCA conduct rules curbing mis-selling and predatory lending practices

- EU: MiFID II mandating suitability assessments and product governance

The Consumer Protection Act and similar legislation require clear disclosures and fair treatment of retail customers.

Data Privacy and Cybersecurity

The General Data Protection Regulation and California Consumer Privacy Act establish baseline data security requirements. Banking-specific standards include:

- DORA (effective 2025) requiring strong authentication

- NIS2 expanding cybersecurity duties with fines up to €10 million

These frameworks demand MFA, supply chain audits, and incident reporting for data breaches.

Prudential Requirements

Basel III dictates capital adequacy ratios and liquidity coverage. The Prudential Regulation Authority and European Central Bank supervise compliance with these standards. Banks must maintain CET1 ratios and submit regular financial reporting.

ESG and Climate Disclosure

EU sustainable finance rules, TCFD-style climate disclosures, and supervisor-mandated climate stress tests are expanding. ESG intersects with conduct regulation through sustainable investment product governance.

Regional and Cross-Border Compliance Considerations

Multi-jurisdictional banks must reconcile differing local rules while maintaining consistent group standards.

Regional priorities differ:

Yargı Yetkisi | Primary Focus |

|---|---|

Birleşik Krallık | Conduct, operational resilience, FCA supervision |

Avrupa Birliği | Harmonised AMLDs, GDPR, DORA |

İsviçre | Data sovereignty, FINMA-supervised wealth management |

Birleşik Devletler | BSA/PATRIOT Act, CFPB oversight, Federal Reserve System supervision |

Emerging markets | Local licensing (e.g., Nigeria’s BOFIA), capital requirements |

Regulators increasingly share information through mechanisms like FinCEN’s 314(b) recertifications and joint investigations. Cross-border penalties amplify consequences for regulatory bodies acting in concert.

Data residency and localisation rules make technology stack choices strategically important. Cloud concentration risk and exposure to extraterritorial surveillance under the US CLOUD Act or Chinese data laws create vulnerabilities.

InvestGlass offers a Swiss sovereign alternative. Institutions can host client data within Europe or on-premise, avoiding dependency on American or Chinese hyperscalers while meeting more stringent compliance requirements.

Core Components of an Effective Bank Compliance Framework

An effective compliance framework embeds into risk governance and aligns with the three lines of defence model:

- First line: Business units own and execute compliance procedures

- Second line: Compliance team monitors, advises, and tests

- Third line: Internal audit provides independent assurance

Policy Architecture

Board-approved policies map to specific regulations. Standards define KYC periodicity, escalation thresholds, and documentation requirements. Operating procedures guide day-to-day execution.

Yönetişim Yapıları

The Chief Compliance Officer leads the compliance team, advises the board, and liaises with supervisors. Compliance committees provide oversight and escalation channels. Audit committees receive regular compliance issues reporting.

Risk Değerlendirmeleri

Conduct regular risk assessments to identify inherent and residual exposure across products, geographies, and channels. Quantify operational risk and prioritise remediation based on impact.

Monitoring and Testing

Ongoing monitoring provides early warning of control failures. Testing programmes verify that compliance procedures operate effectively. Internal audit tracks remediations and validates sustained improvement.

Training and Culture

Compliance training programs must go beyond annual e-learning. Effective programmes embed compliance risk management into everyday decision-making through scenario-based exercises, team discussions, and leadership reinforcement.

Typical Compliance Risks in the Banking Sector

Compliance risk is the risk of legal penalties, regulatory sanctions, financial loss, or reputational damage from non-adherence to rules.

Main risk categories include:

- AML/CTF risk: Inadequate screening, monitoring, or reporting to prevent money laundering

- Sanctions risk: Processing prohibited transactions amid geopolitical tensions

- Data protection and cyber risk: Breaches under GDPR or NIS2

- Conduct and mis-selling risk: Unsuitable product recommendations under MiFID or FCA rules

- Market abuse risk: Insider trading or manipulation

- Third-party and outsourcing risk: Failures in vendor controls

Enforcement actions in 2023 and 2024 targeted banks for deficient AML controls, sanctions compliance banks failed to maintain, and data breaches affecting millions of customers.

Digital transformation amplifies these risks. Remote onboarding, instant payments, and automated processes can accelerate failures if not properly controlled. Human error remains a significant factor in compliance violations.

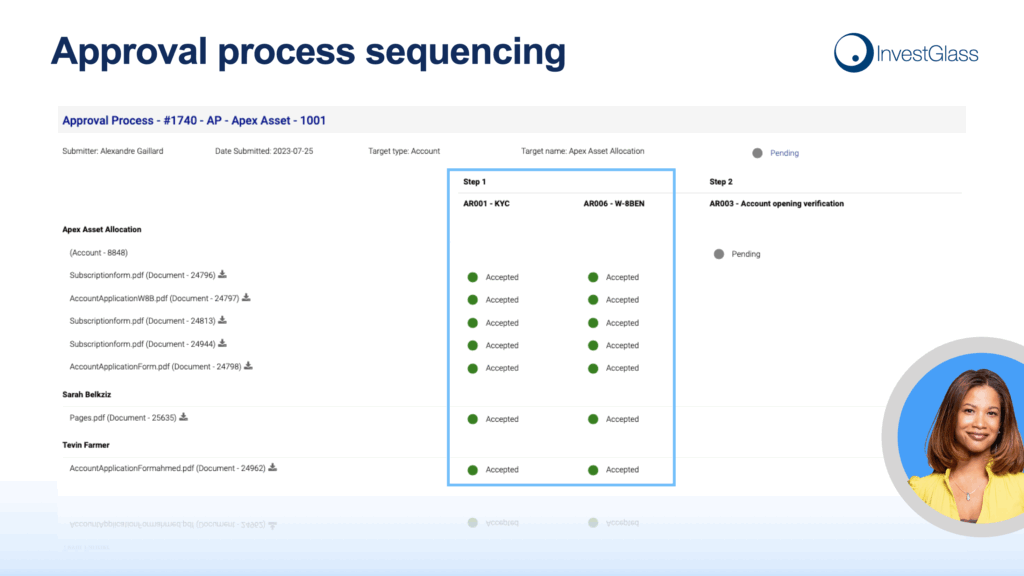

Centralised systems like InvestGlass CRM and onboarding improve visibility, create audit trails, and consolidate documentation across all compliance responsibilities. This reduces fragmentation and supports evidence gathering for regulators.

Roles and Responsibilities in Bank Compliance

Compliance is a shared responsibility distributed across the organisation.

Board and Executive Committee

- Set risk appetite and approve policies

- Receive regular compliance reporting

- Establish tone from the top

- Ensure adequate compliance costs budgeting

Chief Compliance Officer and Compliance Teams

- Own policy development and maintenance

- Provide advisory support to business lines

- Monitor regulatory changes and assess impact

- Liaise with regulatory bodies during examinations

- Coordinate compliance training programs

First Line Business Operations

- Execute KYC checks and ongoing monitoring

- Conduct transaction monitoring and escalate suspicious activity

- Maintain client records and documentation

- Complete mortgage lending and fair lending compliance checks

Specialist Roles

Larger institutions require dedicated compliance officers for specific domains:

- MLROs for suspicious activity reporting

- Data Protection Officers for GDPR and legal compliance

- Sanctions Officers for screening and escalation

Senior management bears ultimate accountability for maintaining regulatory compliance across all functions.

How Technology Transforms Banking Compliance

The banking industry has shifted from manual, spreadsheet-driven compliance to integrated RegTech and automation. This transformation addresses the increasingly complex regulatory environment while reducing operational risk.

Dijital Onboarding ve e-KYC

Digital onboarding reduces client acquisition time from weeks to hours while maintaining strong identification controls. Biometric verification, document scanning, and risk scoring happen within unified workflows. This supports ongoing compliance with ki̇mli̇k doğrulama requirements.

Workflow Automation and Rules Engines

Automated rules engines handle transaction monitoring, flagging suspicious financial transactions for human review. Case management systems track investigations through to resolution. AI supports anomaly detection and prioritisation.

Integrated CRM and Compliance Tooling

A single client view consolidates communications, documentation, approvals, and risk indicators. This improves auditability and reduces the fragmentation that creates compliance issues.

InvestGlass delivers these capabilities within Swiss or on-premise infrastructure. Banks maintain compliance while protecting client sovereignty and limiting exposure to extraterritorial surveillance.

InvestGlass for Banking Compliance and Data Sovereignty

InvestGlass is a Swiss sovereign CRM and automation platform Bankalar için üretildi and regulated institutions seeking to maintain regulatory compliance without compromising data sovereignty.

Digital Onboarding and KYC Workflows

Structure identity verification, risk scoring, and periodic reviews with full audit trails. Automated workflows ensure consistency across ilişki yöneticileri and branches. Documentation remains linked to client records for supervisor reviews.

CRM ve Müşteri Portalı

Consolidate communications, approvals, and documentation in one system. The client portal provides secure access for customers while maintaining compliance procedures for record-keeping. This supports evidence gathering for internal audits and regulatory examinations.

Portfolio Management and Advisory Features

Link suitability assessments, product governance, and investment decisions in a traceable workflow. Document ESG preferences and disclosure requirements for sustainable finance compliance.

Sovereign Hosting

Hosting in Switzerland or on-premise allows banks to avoid reliance on American or Chinese platforms. This preserves data sovereignty and client trust while meeting data localisation requirements.

Example use cases:

- A private bank reduced cross-border KYC review times by implementing structured workflows with full audit trails, improving regulatory reporting capabilities

- An asset manager strengthened ESG disclosure documentation by linking TCFD requirements directly to portfolio holdings and client communications

Implementing and Improving a Bank’s Compliance Programme

Compliance transformation should be phased and risk-based rather than attempting to address everything simultaneously.

Practical Implementation Steps

- Gap analysis: Assess current controls against regulatory requirements and industry standards

- Prioritisation: Focus on high-risk areas including AML, data protection, and conduct

- Roadmap: Create a multi-year remediation plan with clear milestones

- Ownership: Assign executive sponsors and budget holders for each initiative

- Execution: Implement changes with proper change management and staff training

Success Factors

- Data quality: Clean, consistent client data enables effective monitoring

- System integration: Connected platforms reduce manual handoffs and human error

- Change management: Updated compliance procedures require training and reinforcement

- Measurement: Track key risk indicators and regulatory demands to demonstrate progress

InvestGlass can be rolled out module by module. Start with onboarding and CRM to establish the client data foundation, then extend to workflow automation, regulatory reporting, and portfolio management.

Future Trends in Banking Compliance

Several developments will shape compliance strategies in coming years.

Anticipated regulatory changes:

- Stricter ESG disclosure requirements and climate stress testing

- AI governance rules under frameworks like the EU AI Act

- Instant-payment fraud controls and liability shifts

- Crypto-asset regulation under FATF travel rule expansions

- Enhanced third-party risk management and cloud concentration scrutiny

The financial sector will see increased use of Yapay zeka ajanları and machine learning for continuous monitoring, anomaly detection, and regulatory scrutiny responses. Compliance teams must build data-centric architectures that adapt quickly to new obligations.

Flexible, sovereign platforms position banks to maintain compliance while protecting client data and institutional independence. As regulatory demands intensify, institutions that invest in robust compliance efforts and technology infrastructure will gain competitive advantage.

InvestGlass offers banks and other financial institutions a path forward. Swiss hosting, integrated workflows, and modular deployment support compliance strategies that ensure regulatory compliance today while preparing for tomorrow’s requirements.

Önemli Çıkarımlar

- Banking regulatory compliance spans financial crime, data privacy, conduct, prudential rules, and ESG obligations

- Non-compliance leads to legal penalties, reputational damage, and loss of correspondent banking relationships

- Effective compliance risk management requires clear governance, risk assessments, and embedded culture

- Technology transforms compliance through automation, integrated CRM, and improved auditability

- Sovereign platforms like InvestGlass protect data sovereignty while supporting regulatory requirements

Building a sovereign, data-driven compliance infrastructure positions your institution for regulatory confidence and client trust. Consider how InvestGlass can help your bank maintain compliance while protecting the sovereignty of client data within European or on-premise infrastructure.

İlgili makaleler

İsviçre Egemen CRM: Yapay Zeka Üzerine Kurulu.

Hareket etmeye hazır.