소개

To start a development bank, you need more than a banking licence and capital: you need a clear developmental mandate, rigorous market and regulatory research, a detailed business plan and governance structure, robust operating and technology systems, and the compliance framework to support long-term lending at scale. Unlike traditional commercial banks driven primarily by profit motives, development banks are established to provide long-term financing for projects aligned with national or regional priorities. Their purpose is to expand access to finance, drive economic growth, and support development goals that conventional lenders often overlook, especially in sectors such as infrastructure, renewable energy, and small and medium-sized enterprises (SMEs).

For financial innovators, institutions, and entrepreneurs seeking to build a bank with measurable economic and social impact, understanding how a development bank is structured, licensed, funded, and operated is essential. These institutions help close funding gaps where private capital is limited or risk-averse, which makes them central to financial inclusion, economic resilience, and sustainable development. This comprehensive guide, brought to you by InvestGlass, a leading Swiss-based CRM and automation platform for financial services, explains the market role of development banks, the step-by-step establishment process, the global regulatory mosaic from the Financial Conduct Authority (FCA) in the UK to the Monetary Authority of Singapore (MAS), and the operational infrastructure required to launch and scale effectively.

It also examines capitalisation and funding strategies, governance, compliance and risk management, and the technology backbone needed to run a modern development bank, including how platforms like InvestGlass support these requirements. With the right vision, tools, and execution, founders can create institutions that not only operate soundly but also finance national priorities and catalyse long-term economic progress.

학습 내용

The fundamental definition and market role of development banks.

Key regulatory bodies and frameworks across Europe, Asia, and the Middle East.

A step-by-step guide to the establishment process, from conception to launch.

The critical role of technology and operational infrastructure, with a focus on InvestGlass solutions.

The unique advantages of Swiss data sovereignty and InvestGlass’s commitment to compliance.

Strategies for capitalisation, funding, compliance, risk management, and sustainable growth.

개발 은행의 이해 정의 및 시장 개요

개발 금융 기관(DFI)이라고도 불리는 개발 은행은 경제 개발 프로젝트에 장기 자본을 제공하기 위해 국가 또는 다자간 조직에 의해 설립된 전문 금융 기관입니다. 주로 단기 대출과 수익 극대화에 중점을 두는 상업 은행과 달리 개발은행은 시장 실패를 해결하고 지속 가능한 성장을 촉진하며 전략적 국가 우선순위를 지원해야 하는 공공의 의무에 따라 운영됩니다. 개발은행의 핵심 기능은 경제 발전에 필수적이지만 높은 위험, 긴 소요 기간, 낮은 즉각적인 수익률로 인해 충분한 민간 투자를 유치하지 못하는 부문에 자금을 공급하는 것입니다. 이러한 분야에는 일반적으로 인프라(교통, 에너지, 통신), 농업, 교육, 의료, 중소기업(SME)이 포함됩니다.

개발은행의 역사적 맥락은 제2차 세계대전 이후 많은 정부가 경제 재건과 산업화 촉진을 위한 전담 기관의 필요성을 인식한 시기로 거슬러 올라갑니다. 인도 산업 개발 은행과 같은 초기 개발 은행은 초기 산업에 자본과 전문성을 동원하는 데 중추적인 역할을 했습니다. 시간이 지나면서 개발은행의 임무는 빈곤 감소, 환경 지속 가능성, 사회적 형평성 등 보다 광범위한 개발 목표를 포괄하도록 발전해 왔습니다. 오늘날 개발은행은 국가, 지역, 국제 등 다양한 수준에서 운영되고 있습니다. 선진국에서는 이러한 은행이 더 많은 재정 자원과 성숙한 제도를 활용하여 혁신과 첨단 인프라에 중점을 두는 반면, 개발도상국에서는 제한된 자원과 덜 확립된 프레임워크로 인해 보다 근본적인 필요를 해결하고 더 큰 도전에 직면하는 경우가 많습니다. 세계은행 그룹, 유럽투자은행(EIB), 독일의 KfW와 같은 국가개발은행 등이 그 예입니다.

The market overview for development banking reveals a diverse landscape. Some development banks operate as wholesale lenders, providing funds to commercial banks or other financial intermediaries, which then on-lend to target beneficiaries. Others engage in direct lending, equity investments, guarantees, and technical assistance. A key characteristic is their ability to undertake higher risks and accept lower returns than commercial banks, often leveraging their public backing to attract funding from international capital markets, government budgets, and bilateral/multilateral donors. This unique positioning allows them to finance projects that are vital for long-term economic health but might otherwise remain unfunded. The operational efficiency and strategic focus of these institutions are increasingly supported by advanced CRM and automation platforms, such as InvestGlass’s all-in-one sales and automation platform, which enable streamlined client management, project tracking, and compliance adherence, thereby enhancing their overall impact and reach in complex financial ecosystems. In fact, evidence-based insights and reliable data are essential for assessing the effectiveness and credibility of development banks in achieving their objectives.

완전 유연한 CRM InvestGlass

글로벌 규제 환경: 국제 규정 준수 탐색

개발 은행을 설립하려면 여러 관할권의 금융 기관에 적용되는 다양하고 복잡한 규제 프레임워크를 철저히 이해하고 세심하게 준수해야 합니다. 규제 기관은 공식 승인을 받은 은행만 영업할 수 있도록 하고 있으며, 공식 승인 단계를 통과하는 것이 중요하다는 점을 강조하고 있습니다. 이러한 규제 환경은 금융 안정성을 보장하고 소비자를 보호하며 자금 세탁 및 테러 자금 조달과 같은 불법 활동을 방지하기 위해 고안되었습니다. 개발은행의 경우, 이러한 글로벌 모자이크를 헤쳐 나가기 위해서는 일반적인 은행 규정뿐만 아니라 고유한 권한 및 자금 조달 메커니즘과 관련된 특정 조항을 준수해야 합니다. 규제 프로세스는 일반적으로 프로젝트 및 기관의 성공을 보장하기 위해 계획 및 자원 할당부터 승인 및 평가에 이르기까지 특정 순서를 따릅니다. 아래는 특정 지역의 주요 규제 기관과 그 역할에 대한 개요입니다.

유럽

유럽은 정교하고 조화롭지만 지역적으로 미묘한 차이가 있는 규제 환경을 제공합니다. 야심찬 개발 은행은 스위스와 같은 비유럽연합 국가에서도 국가 당국과 중요한 유럽연합 지침을 모두 준수해야 합니다.

United Kingdom (UK): Financial Conduct Authority (FCA)

FCA는 영국의 금융 서비스 회사에 대한 건전성 및 행동 규제 기관입니다. PRA(건전성 규제 당국)가 은행에 대한 건전성 규제를 담당하는 반면, FCA는 소비자 보호와 시장 건전성에 중점을 둡니다. 개발 은행의 경우 이는 금융 상품의 설계, 마케팅 및 판매 방식에 대한 엄격한 규칙을 준수하고 고객을 공정하게 대우하는 것을 의미합니다. FCA의 인가 절차는 엄격하여 상세한 사업 계획, 견고한 지배구조, 적절한 재정 자원에 대한 증거를 요구합니다. [1]

Germany: Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin)

BaFin은 독일의 통합 금융 감독 기관으로 은행, 금융 서비스 제공업체, 보험 사업, 증권 거래를 감독하는 역할을 담당합니다. 금융 기관의 지급 능력을 보장하고 독일 금융 시스템의 무결성과 안정성을 유지하는 것이 이 기관의 임무입니다. 독일의 개발은행은 BaFin의 엄격한 라이선스 요건, 자본 적정성 규정, 지속적인 감독 의무를 준수해야 하며, 이는 종종 주요 기관에 대한 유럽중앙은행(ECB)의 가이드라인의 영향을 받습니다. [2]

France: Autorité des Marchés Financiers (AMF)

프랑스에서는 AMF가 금융 시장을 규제하고 투자자 보호를 보장하며, 금융감독청(Autorité de Contrôle Prudentiel et de Résolution, ACPR)이 은행과 보험회사의 건전성 감독을 담당하고 있습니다. 개발은행은 자본 요건, 리스크 관리 프레임워크, 거버넌스 표준을 준수하는지 확인하는 라이선스 및 건전성 감독을 위해 주로 ACPR과 협력하게 됩니다. 개발은행이 증권 발행이나 공개 시장 운영에 관여하는 경우 AMF의 역할이 중요해질 수 있습니다. [3]

Switzerland: Swiss Financial Market Supervisory Authority (FINMA)

FINMA는 스위스의 독립적인 금융 시장 감독 기관입니다. 은행, 보험사, 증권 거래소, 증권 딜러 및 기타 금융 기관을 감독하는 업무를 담당합니다. FINMA의 규제 접근 방식은 안정성, 투자자 보호, 금융 범죄 척결에 중점을 두는 것으로 잘 알려져 있습니다. 스위스에서 영업하고자 하는 개발 은행의 경우 FINMA의 인가 절차는 포괄적이며, 엄격한 자본, 유동성 및 조직 요건과 함께 강력한 리스크 관리 및 규정 준수 프레임워크를 준수해야 합니다. 스위스의 강력한 데이터 보호법(스위스 데이터 보호에 관한 연방법(FADP))도 중요한 역할을 합니다. [4]

Luxembourg: Commission de Surveillance du Secteur Financier (CSSF)

룩셈부르크 금융감독청은 은행, 투자회사 및 기타 금융 전문가를 포함한 룩셈부르크의 금융 부문에 대한 건전성 감독 기관입니다. 룩셈부르크는 특히 투자 펀드와 국경 간 금융 서비스의 핵심 금융 허브입니다. 이곳에 설립되는 개발은행은 강력한 거버넌스, 리스크 관리 및 자본화에 초점을 맞춘 유럽 지침에 따른 CSSF의 승인 절차를 거쳐야 합니다. 또한 자금세탁방지(AML) 및 테러자금조달방지(CTF) 감독에 있어서도 CSSF는 중요한 역할을 담당합니다. [5]

Ireland: Central Bank of Ireland (CBI)

아일랜드 중앙은행은 중앙은행 기능과 금융 서비스 제공업체에 대한 규제를 모두 담당합니다. 은행, 투자 회사 및 기타 금융 기관을 감독하며 건전성 및 소비자 보호에 중점을 두고 있습니다. 개발 은행의 경우 CBI의 인가 절차에는 유럽 은행 감독의 맥락에서 자본 요건, 지배구조, 리스크 관리 프레임워크의 준수 여부를 입증하는 것이 포함됩니다.

아시아

아시아의 금융 시장은 역동적이고 다양하며, 규제 당국은 빠른 경제 성장과 기술 발전에 적응하고 있습니다.

· Singapore: Monetary Authority of Singapore (MAS)

MAS는 싱가포르의 중앙은행이자 통합 금융 규제 기관의 역할을 합니다. 은행, 보험사, 자본시장 중개기관 등 싱가포르의 모든 금융기관을 감독합니다. MAS는 특히 핀테크 및 지속 가능한 금융과 같은 분야에서 미래 지향적이고 강력한 규제 접근 방식을 취하는 것으로 유명합니다. 싱가포르의 개발은행은 기업 지배구조와 기술적 복원력에 중점을 두고 MAS의 엄격한 라이선스 기준, 자본 적정성 비율, 포괄적인 리스크 관리 가이드라인을 충족해야 합니다. [6]

· Hong Kong: Securities and Futures Commission (SFC)

홍콩금융관리국은 홍콩 증권 및 선물 시장의 주요 규제 기관입니다. 홍콩금융관리국(HKMA)이 은행을 감독하지만, 채권이나 기타 증권 발행과 같은 자본 시장 활동에 관여하는 개발 은행의 경우 SFC의 역할이 매우 중요합니다. SFC 규정을 준수하면 이러한 벤처기업에서 시장 무결성과 투자자 보호를 보장할 수 있습니다. [7]

· Japan: Financial Services Agency (FSA)

금융청은 은행, 증권, 보험 부문을 감독하는 일본의 통합 금융 규제 기관입니다. 금융 시스템의 안정성을 보장하고 투자자를 보호하는 것을 목표로 합니다. 일본의 개발은행은 건전하고 효율적인 금융 시스템을 유지하기 위해 설계된 인허가, 자본 요건 및 감독 감독을 포함한 FSA의 포괄적인 규제 프레임워크의 적용을 받게 됩니다. [8]

· South Korea: Financial Services Commission (FSC)

금융위원회는 금융 정책, 금융 기관에 대한 감독 및 검사를 담당하는 대한민국 최고 금융 규제 기관입니다. 일상적인 감독을 담당하는 금융감독원(FSS)과 협력하여 업무를 수행합니다. 개발은행은 글로벌 모범 사례와 국내 경제 상황을 반영하여 지속적으로 업데이트되는 금융감독원의 인허가 제도, 자본 적정성 기준, 리스크 관리 가이드라인을 준수해야 합니다.

· India: Securities and Exchange Board of India (SEBI)

SEBI는 인도 증권 시장의 규제 기관입니다. 인도중앙은행(RBI)이 은행의 주요 규제 기관이지만, 공모 발행을 통한 자금 조달이나 증권 상장과 같은 자본 시장 활동에 참여하는 개발 은행의 경우 SEBI의 역할이 매우 중요합니다. SEBI 규정을 준수하면 빠르게 성장하는 인도 금융 시장의 투명성과 투자자 보호를 보장할 수 있습니다.

중동

중동은 기존 금융 규제와 이슬람 금융 규제가 혼재되어 있으며, 금융 자유 구역에는 뚜렷한 프레임워크가 존재합니다.

· United Arab Emirates (UAE): Dubai Financial Services Authority (DFSA) in Dubai International Financial Centre (DIFC) and Abu Dhabi Global Market (ADGM)

UAE는 금융 자유 구역 내에서 국내 규제와 별도의 프레임워크를 갖춘 이중 규제 시스템을 운영하고 있습니다. 금융서비스감독청(DFSA)은 DIFC에서 이루어지는 금융 서비스를 규제하고, 금융서비스규제청(FSRA)은 ADGM에서 이루어지는 금융 서비스를 규제합니다. 두 기관 모두 은행, 투자 및 기타 금융 활동을 포괄하는 포괄적인 규정집을 갖춘 독립 규제 기관입니다. 이러한 자유 구역에서 영업하는 개발 은행은 DFSA 또는 FSRA로부터 라이선스를 취득하고 국제 표준을 벤치마킹한 각각의 건전성 및 행동 규정을 준수해야 합니다. [9]

· Saudi Arabia: Capital Market Authority (CMA)

사우디아라비아에서는 사우디 중앙은행(SAMA)이 은행에 대한 주요 규제 기관이며, CMA는 자본 시장을 규제합니다. 개발은행은 주로 라이선스, 자본 및 유동성 요건 등 은행 운영에 대한 SAMA의 관할권에 속합니다. 은행이 증권 관련 활동을 하는 경우, 선진 자본 시장 발전과 투자자 보호를 목표로 하는 CMA 규정도 준수해야 합니다. [10]

· Bahrain: Central Bank of Bahrain (CBB)

바레인 금융감독청은 기존 은행과 이슬람 은행, 보험회사, 투자회사 등 바레인의 전체 금융 부문에 대한 단일 규제 기관입니다. 바레인은 이슬람 금융의 중요한 허브입니다. 바레인의 개발은행은 라이선스, 자본 적정성, 기업 지배구조, 리스크 관리 등을 다루는 CBB의 포괄적인 규정집의 적용을 받으며, 해당되는 경우 이슬람 금융기관에 대한 특정 조항이 적용됩니다. [11]

· Qatar: Qatar Financial Centre Regulatory Authority (QFCRA)

QFCRA는 금융 자유 구역인 카타르 금융 센터(QFC)에서 수행되는 금융 서비스에 대한 독립 규제 기관입니다. QFCRA의 규제 프레임워크는 국제 모범 사례를 기반으로 하며 국제 금융 기관을 유치하기 위해 설계되었습니다. QFC 내에서 영업하는 개발 은행은 QFCRA의 인가를 받아야 하며 건전성 기준, 사업 수행 및 자금 세탁 방지 요건을 포함하는 규정을 준수해야 합니다.

개발 은행을 시작하기 위한 단계별 가이드

Establishing a development bank is a complex, multi-stage process that demands meticulous planning, significant capital, and a deep understanding of regulatory requirements. While the specifics may vary by jurisdiction, the fundamental steps remain consistent. This guide outlines the critical phases involved in bringing a development bank from conception to operational reality, complementing broader resources on founding your own private bank step by step.

- 개념화 및 타당성 조사:

· Define the Mandate: Clearly articulate the development bank’s mission, target sectors (e.g., infrastructure, SMEs, green finance), geographical focus, and desired impact. This mandate will guide all subsequent decisions.

· Market Analysis: Conduct a comprehensive study to identify market gaps, unmet financing needs, and potential beneficiaries. Assess the economic landscape, including growth prospects, existing financial infrastructure, and the competitive environment.

· Legal and Regulatory Review: Research the specific legal and regulatory requirements in the chosen jurisdiction(s). This includes understanding licensing procedures, capital adequacy rules, governance standards, and anti-money laundering (AML)/counter-terrorist financing (CTF) obligations. Consult with legal and regulatory experts early in this stage.

· Financial Projections: Develop detailed financial models, including start-up costs, operational expenses, revenue streams, and projected profitability. This will inform capital raising strategies and demonstrate long-term viability.

- 사업 계획 개발:

· Comprehensive Business Plan: Create a robust business plan that articulates the bank’s vision, mission, strategic objectives, target markets, products and services, organisational structure, risk management framework, and financial projections. This document will be central to securing regulatory approval and attracting investors.

· Governance Structure: Design a clear and effective governance framework, including the board of directors, management committees, and internal control mechanisms. Emphasise independence, transparency, and accountability.

· Risk Management Framework: Outline a comprehensive risk management strategy covering credit risk, operational risk, market risk, liquidity risk, and reputational risk. This should include policies, procedures, and systems for identification, measurement, monitoring, and control of risks.

- 자본화 및 펀딩:

· Initial Capital: Secure the necessary initial capital, which is often substantial and mandated by regulators. This may come from government allocations, multilateral institutions, private investors, or a combination thereof.

· Funding Strategy: Develop a diversified funding strategy, which could include long-term debt issuance, grants, concessional loans from international financial institutions, and equity participation. For instance, InvestGlass can assist in managing investor relations and capital raising processes through its CRM capabilities.

· In addition to core funding sources, development banks may receive supplementary support such as technical assistance or grants to enhance their capacity and effectiveness.

- 규제 적용 및 라이선스:

· Pre-Application Engagement: Engage in pre-application discussions with the relevant regulatory authorities (e.g., FCA, BaFin, FINMA, MAS) to understand their expectations and address any preliminary concerns. This proactive approach can streamline the formal application process.

· Formal Application Submission: The applicant must prepare and submit a detailed application package, including the business plan, financial projections, governance documents, risk management policies, and fit-and-proper assessments for key personnel. This is a highly scrutinised stage, requiring precision and completeness.

· Applicants must demonstrate that all eligibility criteria have been met before proceeding to the next stage of the licensing process.

· Due Diligence and Interviews: Be prepared for extensive due diligence by regulators, including interviews with prospective board members and senior management. Regulators will assess the robustness of the proposed operations and the competence of the leadership team.

· Licensing Approval: Upon successful completion of the regulatory review, the development bank will be granted a banking license, permitting it to commence operations.

- 운영 설정 및 기술 구현:

· Organisational Structure: Establish the operational structure, including departments for lending, risk management, compliance, finance, and human resources.

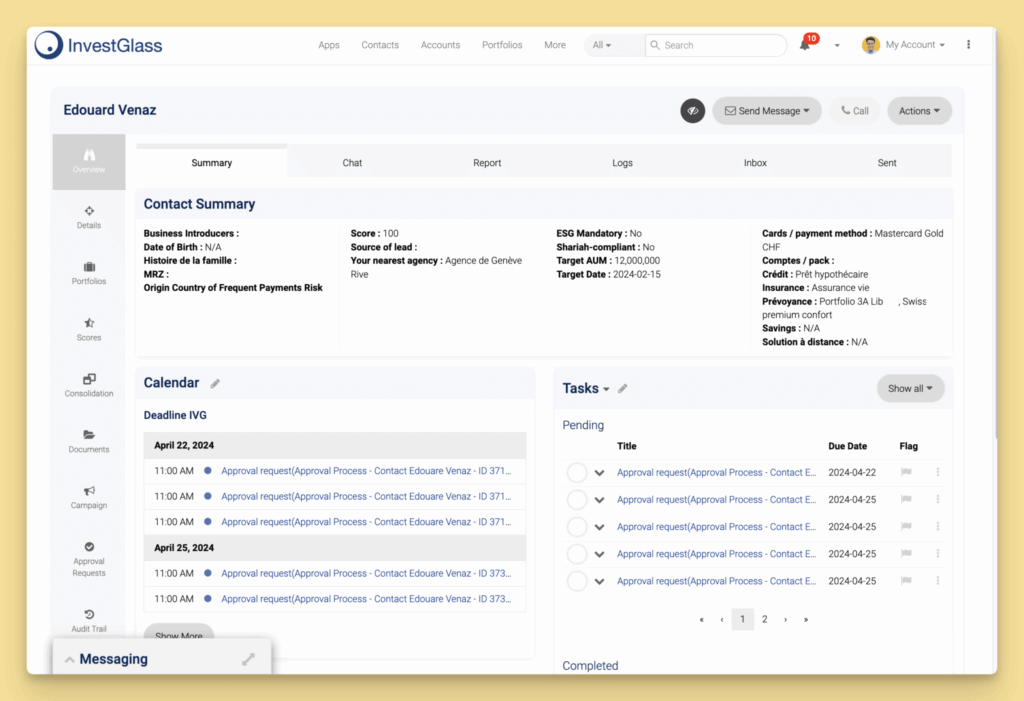

· Technology Infrastructure: Implement robust and scalable technology systems, including core banking platforms, CRM systems, risk management software, and compliance tools. This is where platforms like InvestGlass become invaluable, offering automation for client onboarding, due diligence, portfolio management, and regulatory reporting, ensuring efficiency and compliance from day one.

· Once the technology infrastructure is implemented, ongoing support and training are essential for operational success.

· Policy and Procedure Development: Develop detailed internal policies and procedures for all operational aspects, from loan origination and disbursement to financial reporting and compliance monitoring.

· Staffing and Training: Recruit and train qualified personnel across all functions, ensuring they possess the necessary skills and understand the bank’s mandate and operational protocols.

- 시작 및 진행 중인 작업:

· Phased Launch: Consider a phased launch, starting with a limited range of products or target sectors, and gradually expanding as operational capabilities and market acceptance grow.

· Performance Monitoring: Continuously monitor financial performance, developmental impact, and adherence to regulatory requirements. Regular internal audits and external reviews are crucial.

· Stakeholder Engagement: Maintain active engagement with stakeholders, including government bodies, investors, beneficiaries, and the wider community, to ensure alignment with developmental objectives and foster long-term support. InvestGlass can facilitate this through its comprehensive client relationship management features, enabling effective communication and reporting to all stakeholders.

Technology Infrastructure and Operations: Powering Modern Development Banking and Development Financing

21세기에 성공적인 금융 기관, 특히 고유한 임무를 가진 개발 은행의 운영 중추는 기술 인프라입니다. 현대의 개발 금융은 전통적인 대출을 넘어 정교한 데이터 관리, 원활한 고객 상호 작용, 엄격한 리스크 평가, 투명한 보고를 포함합니다. 강력하고 확장 가능한 기술 스택은 단순한 이점이 아니라 효율성, 규정 준수, 궁극적으로 개발 목표 달성을 위한 근본적인 필수 요소입니다. 바로 이 점에서 InvestGlass와 같은 플랫폼은 필수 불가결한 우위를 제공합니다.

At its core, a development bank requires a comprehensive suite of technological solutions. This includes a Core Banking System (CBS) for managing accounts, transactions, and financial products; a Customer Relationship Management (CRM) system for client onboarding, interaction tracking, and relationship management that supports digital differentiation for banks through automation and AI; and Enterprise Resource Planning (ERP) software for integrating various business processes. Beyond these foundational elements, specialised tools for risk management, compliance (AML/CTF), data analytics, and reporting are crucial. The ability to integrate these systems seamlessly ensures a holistic view of operations and client engagements.

InvestGlass, a Swiss-based CRM and automation platform tailored to financial services, is uniquely positioned to empower development banks with the technological capabilities they need. Its modular architecture allows for tailored implementation, addressing specific requirements from client lifecycle management to complex regulatory reporting. For instance, the InvestGlass platform can automate the client onboarding process, significantly reducing manual effort and enhancing data accuracy. Its advanced workflow automation capabilities streamline loan application processing, due diligence, and approval workflows, ensuring that funds are deployed efficiently and transparently. This automation is critical for development banks that often deal with a high volume of diverse projects and beneficiaries.

Furthermore, InvestGlass provides powerful tools for portfolio management and impact assessment. Development banks need to track not only financial returns but also the social and economic impact of their investments. The platform’s analytical capabilities allow for the aggregation and analysis of project data, enabling AI-enhanced portfolio monitoring and key performance indicators (KPIs) related to developmental objectives. This data-driven approach supports informed decision-making and demonstrates accountability to stakeholders and funders. The CRM functionalities also ensure that client interactions are meticulously recorded, fostering strong relationships with beneficiaries and partners, which is vital for the long-term success of developmental initiatives. The effective management and operation of this technology infrastructure depend on qualified staff, including IT, compliance, and project management personnel, whose expertise ensures systems run smoothly and securely—much as sector-specific CRMs, for example InvestGlass for dental practices, rely on trained teams to fully leverage digital onboarding and automation. By leveraging InvestGlass, development banks can ensure their operations are not only compliant and secure but also agile and effective in driving positive change.

왜 인베스트글래스인가? 금융 기관을 위한 스위스 데이터 주권

금융 기관, 특히 여러 관할권에서 운영되는 개발 은행의 경우 데이터 보안, 개인정보 보호 및 규제 준수는 운영상의 고려 사항일 뿐만 아니라 신뢰와 안정성의 근본적인 요소입니다. 이러한 중요한 환경에서 InvestGlass는 스위스의 데이터 주권과 정치적 중립성에 기반한 매력적인 제안을 통해 민감한 금융 데이터에 대해 비교할 수 없는 수준의 보장을 제공합니다.

스위스는 오랫동안 안정성, 개인정보 보호, 강력한 금융 서비스의 대명사였습니다. 이러한 명성은 전 세계에서 가장 엄격한 데이터 보호법에도 적용됩니다. InvestGlass는 이러한 환경을 활용하여 최고 수준의 데이터 보존 및 보안을 충족하는 솔루션을 제공합니다. 고객은 스위스 데이터 센터의 온프레미스 호스팅 옵션의 유연성을 통해 인프라와 데이터를 완벽하게 제어할 수 있습니다. 또는 클라우드 솔루션을 선호하는 고객을 위해 InvestGlass는 스위스에서 완전한 데이터 상주 기능을 갖춘 클라우드 호스팅을 제공하여 모든 데이터가 스위스 국경 내에 유지되고 스위스 법의 보호를 받으며 미국 클라우드 법과 같은 외국 데이터 액세스 요청의 대상이 되지 않도록 보장합니다.

규정 준수는 인베스트글래스 서비스의 초석입니다. 이 플랫폼은 유럽연합의 GDPR(일반 데이터 보호 규정)과 스위스 연방 데이터 보호법(FADP)을 비롯한 엄격한 데이터 보호 규정을 쉽게 준수할 수 있도록 설계되었습니다. 이러한 이중 규정 준수를 통해 개발 은행은 유럽 및 해외 사업 전반에서 고객 데이터를 자신 있게 관리하여 규제 위험을 완화하고 개인정보 보호에 대한 헌신을 입증할 수 있습니다. InvestGlass의 아키텍처는 은행 수준의 보안 및 암호화 표준을 통합하여 고급 암호화 기술과 다단계 인증을 사용하여 무단 액세스, 침해 및 사이버 위협으로부터 데이터를 보호합니다. 이러한 보안 수준은 민감한 경제 및 개인 정보를 취급하는 금융 기관에 가장 중요합니다.

또한 InvestGlass는 개발 은행이 여러 관할권의 규제를 준수하는 데 중추적인 역할을 합니다. 강력한 CRM 및 자동화 기능을 통해 여러 지역의 특정 규제 요건에 맞게 워크플로우와 보고 메커니즘을 맞춤화할 수 있습니다. 이러한 기능은 여러 국가에 걸쳐 다양한 임무와 고객 기반을 두고 각각 고유한 규칙을 가지고 운영되는 개발 은행에 매우 중요합니다. 스위스의 법적 프레임워크에서 비롯된 InvestGlass의 고유한 데이터 보호 이점은 규제를 받는 금융 기관에 상당한 경쟁 우위를 제공합니다. 또한 고객과 파트너가 데이터를 최대한 주의하고 기밀로 취급하여 신뢰를 강화하고 원활한 국제 협업을 촉진할 수 있도록 보장합니다.

궁극적으로 InvestGlass는 스위스 은행의 기밀 유지 전통을 CRM 데이터에 적용합니다. 현대의 규제는 전통적인 은행 기밀성에서 진화했지만, 고객 기밀성, 데이터 무결성, 개인정보 보호의 기본 원칙은 여전히 스위스 금융 정신에 깊이 내재되어 있습니다. InvestGlass는 이러한 원칙을 디지털 솔루션으로 확장하여 개발 은행이 가장 소중한 자산인 고객 정보를 관리할 수 있는 안전하고 규정을 준수하며 정치적으로 중립적인 플랫폼을 제공합니다. 데이터 주권과 보안에 대한 이러한 노력 덕분에 InvestGlass는 탄력적이고 신뢰할 수 있으며 글로벌 규정을 준수하는 운영을 구축하고자 하는 개발 은행에게 이상적인 파트너가 되었습니다.

자본 요구 사항 및 자금 조달 전략

개발 은행을 설립하고 유지하려면 초기에는 인허가를 위해, 그리고 운영 활동과 대출 의무를 위해 지속적으로 상당한 자본이 필요합니다. 개발은행이 재정적 지속가능성을 확보하고 측정 가능한 개발 영향력을 입증하려면 몇 년이 걸릴 수 있다는 점에 유의하는 것이 중요합니다. 주로 예금에 의존하는 상업은행과 달리 개발은행은 장기적인 투자 기간과 개발 목표를 반영하여 보다 다양하고 복잡한 자금 조달 구조를 가지고 있는 경우가 많습니다. 이러한 자본 요건과 자금 출처를 이해하고 전략적으로 관리하는 것은 은행의 안정성과 사명을 완수하는 데 있어 가장 중요합니다.

초기 자본금 요구 사항

각 관할권의 규제 당국은 신규 은행 기관에 최소 자본금 요건을 부과합니다. 이러한 요건은 은행의 지급 능력과 잠재적 손실을 흡수할 수 있는 능력을 보장하기 위해 마련되었습니다. 개발 은행의 경우 이러한 수치는 운영 범위와 인지된 위험 프로필에 따라 수천만 유로, 파운드 또는 프랑에 이르는 상당한 금액이 될 수 있습니다. 영국 금융감독청(FCA), 독일 금융감독청(BaFin), 프랑스 금융감독청(FINMA), 네덜란드 금융감독청(MAS) 등의 규제 기관은 라이선스 과정에서 초기 자본의 적정성을 꼼꼼하게 평가합니다. 이 자본은 일반적으로 운영 및 신용 위험에 대한 완충 역할을 하며 기관을 지원하려는 설립자의 헌신과 역량을 보여줍니다.

자금 조달 전략

개발 은행은 장기적인 투자와 운영에 필요한 자금을 조달하기 위해 다양한 자금 조달 전략을 사용합니다:

7. Government Allocations and Subsidies: Many development banks are state-owned or state-backed, receiving direct budgetary allocations, grants, or concessional loans from national governments. This funding reflects the government’s commitment to specific developmental goals and provides a stable, often low-cost, capital base.

8. Multilateral and Bilateral Development Institutions: Partnerships with international financial institutions (IFIs) such as the World Bank, International Finance Corporation (IFC), European Investment Bank (EIB), and various bilateral development agencies are crucial. These institutions provide long-term loans, credit lines, and technical assistance, often at favourable terms, enabling the development bank to leverage its capital and expand its reach.

9. Issuance of Bonds and Debt Instruments: Development banks frequently access international and domestic capital markets by issuing bonds. Their public or quasi-sovereign backing often grants them higher credit ratings, allowing them to raise funds at competitive rates. These bonds can be tailored to specific projects (e.g., green bonds for environmental initiatives) or general funding purposes.

10. Equity Investments: Beyond initial capital from founders or governments, development banks may attract equity investments from institutional investors, pension funds, or other financial entities that align with their developmental mandate. This broadens the ownership base and introduces private sector discipline.

11. Loan Repayments and Interest Income: As a bank, a significant portion of its ongoing funding comes from the repayment of loans and the interest generated on its lending portfolio. Effective portfolio management and robust credit assessment are vital to ensure a healthy repayment cycle.

12. Guarantees and Risk-Sharing Mechanisms: Development banks often provide guarantees to commercial banks, encouraging them to lend to riskier developmental projects. They may also engage in risk-sharing agreements, where a portion of the risk is borne by other financial partners or government entities.

13. Deposits (Limited): While not their primary funding source, some development banks may accept deposits, particularly from institutional clients or specific government entities, though this is less common than for commercial banks.

Effective management of these diverse funding sources requires sophisticated financial planning and treasury management. InvestGlass’s private banking-grade CRM capabilities can assist development banks in managing their investor relations, tracking funding commitments, and ensuring transparent reporting to various capital providers, thereby optimising their funding mix and enhancing financial stability.

규정 준수 및 위험 관리

For any financial institution, and particularly for a development bank with its public mandate and often complex funding structures, a robust compliance and risk management framework is not just a regulatory requirement but a cornerstone of its credibility and long-term sustainability. The result of such a framework is enhanced institutional credibility and long-term sustainability. This framework must be comprehensive, proactive, and deeply embedded in the institution’s culture and operations, increasingly relying on automated KYC verification and onboarding workflows. It encompasses a wide range of activities, from adhering to anti-money laundering (AML) and counter-terrorist financing (CTF) regulations to managing credit, operational, and reputational risks.

규정 준수 프레임워크

개발 은행의 규정 준수 프레임워크는 은행이 사업을 운영하는 모든 관할권에서 다양한 법률 및 규제 의무를 다루어야 합니다. 주요 구성 요소는 다음과 같습니다:

· AML/CTF Compliance: This is a critical area, requiring robust systems for customer due diligence (CDD), know-your-customer (KYC) checks, transaction monitoring, and reporting of suspicious activities to relevant authorities. The complexity of development finance, which can involve cross-border transactions and politically exposed persons (PEPs), necessitates a highly sophisticated approach to AML/CTF.

· Regulatory Reporting: Development banks are subject to extensive reporting requirements from regulatory bodies such as the FCA, BaFin, FINMA, and MAS. These reports cover financial performance, capital adequacy, liquidity, risk exposures, and compliance with various regulations. Timely and accurate reporting is essential to maintain a good standing with regulators.

· Data Privacy and Protection: Adherence to data protection laws like GDPR and the Swiss FADP is paramount. This involves implementing policies and procedures for the lawful collection, processing, storage, and transfer of personal data, as well as ensuring that clients’ privacy rights are respected.

· Conduct and Ethics: A strong ethical culture, supported by a code of conduct and policies on conflicts of interest, anti-bribery, and corruption, is vital. This is particularly important for development banks, which are entrusted with public funds and a developmental mission.

위험 관리 프레임워크

개발은행의 리스크 관리 프레임워크는 재무적 리스크와 비재무적 리스크를 모두 포함하는 고유한 리스크 프로필에 맞게 조정되어야 합니다:

· Credit Risk: This is the risk of loss arising from a borrower’s failure to repay a loan or meet its contractual obligations. Development banks often lend to higher-risk sectors or projects, making robust credit risk assessment, portfolio diversification, and effective loan workout strategies essential.

· Operational Risk: This encompasses the risk of loss resulting from inadequate or failed internal processes, people, and systems, or from external events. It includes legal risk, but excludes strategic and reputational risk. For a development bank, this can range from technology failures to internal fraud.

· Market Risk: This is the risk of losses arising from movements in market prices, such as interest rates, foreign exchange rates, and equity prices. Development banks with international operations and diverse funding sources are particularly exposed to market risk.

· Liquidity Risk: This is the risk that the bank will be unable to meet its financial obligations as they fall due. It requires careful management of assets and liabilities to ensure sufficient cash flow.

· Reputational Risk: For a development bank, reputational risk is a significant concern. Any perception of mismanagement, corruption, or failure to achieve developmental impact can undermine public trust and jeopardise funding.

규정 준수 및 리스크 관리에서 기술의 역할

Modern technology platforms like InvestGlass are instrumental in building and maintaining an effective compliance and risk management framework. InvestGlass provides automated tools for KYC/AML checks, client onboarding, and ongoing due diligence, ensuring a consistent and auditable process and supporting AI-driven portfolio management and risk analytics. Its CRM capabilities allow for the systematic tracking of client interactions and risk profiles, while its reporting features can be configured to generate regulatory reports in the required formats. By centralising client and project data, InvestGlass enables a holistic view of risk exposures, facilitating more effective risk management and compliance oversight. This technological support is crucial for development banks to navigate the complexities of the global financial landscape while staying true to their developmental mission.

성장 및 확장 전략

개발 은행이 설립되고 운영되면 지속 가능한 성장과 영향력 확대로 초점을 전환합니다. 개발은행의 확장은 단순히 대출 규모를 늘리는 것이 아니라 개발 영향력을 심화하고, 범위를 넓히고, 재정적 지속가능성을 강화하는 것입니다. 이를 위해서는 재무적 신중함과 핵심 사명 간의 균형을 맞추는 전략적 접근이 필요합니다.

영향력 측정 및 커뮤니케이션

지속적인 효과를 보장하기 위해 개발 은행은 그 영향을 엄격하게 측정하고 전달해야 합니다. 공식적인 평가는 프로젝트가 의도한 결과를 달성하고 주목할 만한 긍정적인 영향을 미쳤는지 평가하기 위해 실시됩니다. 이러한 평가는 책임성을 입증하고 향후 전략을 수립하는 데 도움이 됩니다.

전략적 확장

14. Geographical Expansion: Depending on the initial mandate, a development bank might consider expanding its operations to new regions or countries. This requires thorough market research, understanding new regulatory environments, and building local partnerships. For instance, a national development bank might evolve into a regional one, or a regional bank might target specific sub-regions with high developmental needs.

15. Product and Service Diversification: Expanding the range of financial products and services can cater to a broader spectrum of developmental needs. This could include introducing new types of loans (e.g., green loans, social impact bonds), equity investments, guarantees, technical assistance programmes, or advisory services. Diversification should always align with the bank’s core mandate and risk appetite.

16. Sectoral Deepening: Instead of broad expansion, a development bank might choose to deepen its expertise and investment in specific sectors. For example, a bank initially focused on general infrastructure might specialise further in renewable energy projects, developing bespoke financial instruments and technical knowledge in that niche.

운영 효율성 및 영향력 향상

· Leveraging Technology for Scale: Technology is a critical enabler for scaling. Implementing advanced CRM and automation platforms, such as InvestGlass, allows development banks to manage a larger client base, process more transactions, and handle complex data more efficiently without a proportional increase in operational costs. InvestGlass’s capabilities in client onboarding, workflow automation, and regulatory reporting are essential for maintaining efficiency and compliance as the bank grows.

· Partnerships and Collaboration: Strategic alliances with other financial institutions, government agencies, NGOs, and international organisations can significantly amplify a development bank’s reach and impact. Co-financing arrangements, risk-sharing agreements, and knowledge-sharing initiatives can unlock new opportunities and leverage collective resources.

· Talent Development and Organisational Capacity: Scaling requires a corresponding growth in human capital and organisational capacity. Investing in talent acquisition, training, and leadership development is crucial to ensure the bank has the expertise and leadership to manage increased complexity and expanded operations.

영향력 측정 및 커뮤니케이션

개발 은행의 규모가 커질수록 개발 영향력을 엄격하게 측정하고 전달하는 것이 더욱 중요해집니다. 여기에는 명확한 영향력 지표를 설정하고, 강력한 데이터를 수집하고, 결과를 투명하게 보고하는 것이 포함됩니다. InvestGlass와 같은 플랫폼은 영향력 추적 및 보고를 위한 도구를 제공하여 은행이 이해관계자에게 가치를 입증하고 추가 자금을 유치하며 정당성을 강화할 수 있도록 지원함으로써 이를 촉진할 수 있습니다. 영향 평가를 기반으로 한 지속적인 평가와 적응은 성장이 의미 있고 지속 가능한 발전으로 이어지도록 하는 데 있어 핵심입니다.

자주 묻는 질문

Q1: 개발 은행과 상업 은행의 주요 차이점은 무엇인가요?

A1: 가장 큰 차이점은 핵심 업무에 있습니다. 상업 은행은 단기 대출, 예금 수취, 개인과 기업을 위한 광범위한 금융 서비스에 중점을 둔 수익 중심 기관입니다. 반면 개발은행은 시장 실패를 해결하고, 전략적 국가 우선순위를 지원하며, 사회적 또는 환경적 영향을 창출하는 프로젝트에 장기 자금을 제공함으로써 경제 발전을 촉진하기 위해 설립된 미션 중심 기관으로, 종종 상업 대출 기관이 너무 위험하다고 간주되는 분야에서 활동합니다.

Q2: 개발 은행은 일반적으로 어떤 유형의 프로젝트에 자금을 지원하나요?

A2: 개발은행은 일반적으로 지속 가능한 경제 성장과 사회 복지에 기여하는 프로젝트에 자금을 지원합니다. 여기에는 대규모 인프라 프로젝트(예: 도로, 교량, 발전소, 통신), 농업 개발, 재생 에너지 이니셔티브, 교육, 의료 시설, 기존 금융에 접근하기 어려운 중소기업(SME) 지원 등이 포함됩니다.

Q3: 개발 은행은 어떻게 자금을 조달하나요?

A3: 개발은행은 다양한 자금원을 가지고 있습니다. 여기에는 종종 정부의 직접 할당, 보조금, 국가 예산의 양허성 대출이 포함됩니다. 또한 세계은행이나 지역개발은행과 같은 다자개발기구로부터 자금을 확보하고, 자본 시장에서 채권을 발행하며(종종 국가의 지원을 받기도 합니다), 기관 파트너로부터 지분 투자를 받을 수도 있습니다. 대출 상환과 포트폴리오에서 발생하는 이자 수입도 지속적인 자금 조달에 크게 기여합니다.

Q4: 유럽의 개발 은행에 대한 주요 규제 기관은 무엇인가요?

A4: 유럽의 주요 규제 기관으로는 영국의 금융행위감독청(FCA) 및 건전성규제청(PRA), 독일의 금융감독청(BaFin), 프랑스의 금융감독청(ACPR), 스위스의 금융시장감독청(FINMA), 룩셈부르크의 금융감독위원회(CSSF) 및 아일랜드 중앙은행(CBI) 등이 있습니다. 각 기관은 건전성 및 행동 감독에 대한 구체적인 권한을 가지고 있습니다.

Q5: 인베스트글래스는 개발도상국 은행의 규정 준수를 어떻게 지원하나요?

A5: 스위스에 본사를 둔 CRM 및 자동화 플랫폼인 InvestGlass는 자동화된 KYC/AML 확인 및 실사 등 강력한 고객 라이프사이클 관리를 위한 도구를 제공하여 개발 은행을 지원합니다. 맞춤형 워크플로우를 통해 여러 관할권의 다양한 규제 보고 요건을 쉽게 준수할 수 있습니다. 또한 스위스의 데이터 주권에 대한 헌신적인 노력으로 GDPR 및 FADP와 같은 엄격한 데이터 보호법을 준수하여 민감한 금융 데이터에 은행 수준의 보안을 제공합니다.

Q6: 스위스 데이터 주권이 금융 기관에 중요한 이유는 무엇인가요?

A6: 스위스의 데이터 주권은 금융 기관에 매우 중요한데, 이는 고객 데이터가 스위스 내에서 저장 및 처리되고 세계에서 가장 엄격한 데이터 보호법(예: FADP)에 의해 보호되기 때문입니다. 이는 높은 수준의 개인정보 보호, 기밀성 및 보안을 제공하여 외국의 액세스 요청으로부터 데이터를 보호하고 특히 국제적으로 운영되고 민감한 금융 정보를 취급하는 기관의 신뢰를 강화합니다.

Q7: 개발 은행이 직면하는 주요 리스크는 무엇인가요?

A7: 개발은행은 신용 위험(차입자의 채무 불이행), 운영 위험(내부 프로세스 또는 시스템의 장애), 시장 위험(금리 또는 환율 변동), 유동성 위험(금융 의무 불이행), 평판 위험(대외 신뢰 손상) 등 여러 위험에 직면해 있습니다. 이러한 문제를 완화하기 위해서는 효과적인 리스크 관리 프레임워크가 필수적입니다.

Q8: 개발 은행은 개발 영향력을 어떻게 측정할 수 있나요?

A8: 개발 영향력을 측정하려면 은행의 미션에 부합하는 명확하고 정량화 가능한 지표를 설정해야 합니다. 여기에는 일자리 창출, 빈곤 감소, 필수 서비스(예: 깨끗한 물, 전기)에 대한 접근성, 대상 지역의 경제 성장, 환경적 혜택 등을 추적하는 것이 포함됩니다. InvestGlass와 같은 플랫폼은 이러한 영향력 지표를 수집, 분석 및 보고하여 책임과 전략적 조정을 위한 데이터 기반 인사이트를 제공할 수 있습니다.

Q9: 개발 은행의 운영 효율성에서 기술은 어떤 역할을 하나요?

A9: 기술은 현대 개발 은행의 운영 효율성을 위해 필수적입니다. 자동화를 통해 고객 온보딩, 대출 신청 처리, 포트폴리오 관리와 같은 프로세스를 간소화할 수 있습니다. InvestGlass와 같은 강력한 CRM 시스템은 고객과의 상호 작용과 데이터 관리를 개선하고, 통합 리스크 및 규정 준수 도구는 규제 요건을 준수하고 운영에 대한 전체적인 관점을 제공하여 궁극적으로 속도, 정확성, 투명성을 향상시킵니다.

Q10: 개발 은행이 개발 목표를 추구하면서 재정적으로 지속가능할 수 있나요?

A10: 예, 가능하며 종종 핵심 목표이기도 합니다. 개발은행은 상업은행보다 높은 위험과 낮은 수익을 감수할 수 있지만, 장기적인 생존력과 독립성을 보장하기 위해 재정적 지속 가능성을 목표로 합니다. 이는 다각화된 자금 조달 전략, 신중한 재무 관리, 효과적인 대출 회수, 개발 프로젝트이면서 재무 수익 또는 비용 회수의 합리적인 전망이 있는 프로젝트에 집중함으로써 달성할 수 있습니다. 재정적 지속 가능성과 개발 영향 사이의 균형은 지속적인 전략적 과제입니다.

결론

개발은행 설립은 경제 회복력과 지속 가능한 성장을 촉진할 수 있는 독특한 경로를 제공하는 야심차고 영향력 있는 사업입니다. 이 가이드에서 설명한 바와 같이, 구상부터 운영까지의 여정은 복잡한 규제 환경, 상당한 자본 요건, 강력한 기술 인프라의 필요성 등으로 가득 차 있습니다. FCA, BaFin, FINMA, MAS와 같은 기관의 엄격한 승인 절차를 탐색하는 것부터 포괄적인 사업 계획을 세심하게 수립하고 다양한 자금을 확보하는 것까지, 각 단계마다 전략적 선견지명과 확고한 헌신이 필요합니다.

현대의 개발 은행은 시장 실패를 해결하고 공익을 추구한다는 사명에 뿌리를 두고 있지만, 주요 금융 기관의 효율성, 보안 및 규정 준수에 따라 운영되어야 합니다. 바로 이 점에서 InvestGlass와 같은 플랫폼과의 전략적 파트너십이 매우 중요합니다. 개발 은행은 스위스에 기반을 둔 InvestGlass의 CRM 및 자동화 기능을 활용하여 은행 수준의 보안을 보장하고, GDPR 및 FADP와 같은 글로벌 데이터 보호 표준을 준수하며, 복잡한 운영 워크플로우를 간소화할 수 있습니다. 스위스의 데이터 주권에 대한 이러한 노력은 민감한 금융 데이터를 보호할 뿐만 아니라 신뢰를 강화하고 관할권 간 규제 준수를 용이하게 하여 오늘날의 상호 연결된 금융 세계에서 중요한 이점을 제공합니다.

궁극적으로 개발은행의 성공은 재무적 성과뿐만 아니라 실질적인 개발 영향력으로 측정됩니다. 명확한 사명, 잘 실행된 전략, 적절한 기술 도구를 갖춘 금융 혁신가는 번창할 뿐만 아니라 혁신적인 변화를 촉진하여 국가의 경제 및 사회 복지에 크게 기여하는 기관을 구축할 수 있습니다. InvestGlass는 개발 은행이 복잡성을 해결하고 규정을 준수하며 글로벌 무대에서 긍정적인 영향력을 극대화할 수 있도록 지원하여 이 중요한 사명을 완수할 준비가 되어 있습니다.

참조

1] 금융 행위 감독청(FCA). [https://www.fca.org.uk/

2] 독일 금융감독청(BaFin). [https://www.bafin.de/EN/Homepage/homepage_node.html

3] 오소리티 데 마르셰 파이낸스(AMF). [https://www.amf-france.org/en/regulation/regulation-homepage

4] 스위스 금융시장감독청(FINMA). [https://www.finma.ch/en/

5] 금융 부문 감시 위원회(CSSF). [https://www.cssf.lu/en/

6] 싱가포르 통화청(MAS). [https://www.mas.gov.sg/

7] 홍콩 증권선물위원회(SFC). [https://www.sfc.hk/en/

8] 금융 서비스 기관 (FSA) 일본. [https://www.fsa.go.jp/en/

9] 아부다비 글로벌 마켓(ADGM) 금융 서비스 규제 당국(FSRA). [https://www.adgm.com/financial-services-regulatory-authority

10] Capital Market Authority (CMA) Saudi Arabia. [https://cma.gov.sa/en/RulesRegulations/Pages/default.aspx

11] 바레인 중앙은행 (씨비비)

개발 은행 및 커뮤니티 파이낸싱 - 10가지 FAQ

1. 개발은행은 영리를 목적으로 하나요?

개발 은행은 일반적으로 이익이 아닌 공공 또는 지역 사회 발전을 목표로 운영됩니다. 이들의 임무는 전통적인 은행이 간과할 수 있는 특히 소외된 지역의 경제 성장, 인프라 및 일자리 창출을 촉진하는 프로젝트에 자금을 지원하는 것입니다.

2. 나만의 은행을 시작하려면 비용이 얼마나 드나요?

은행을 창업하려면 위치, 규제 요건, 비즈니스 모델에 따라 최소 100만 달러에서 최대 400만 달러까지 상당한 자본 투자가 필요합니다. 개발 금융 기관의 경우, 커뮤니티 중심인지 상업 중심인지에 따라 최소 금액이 달라질 수 있습니다.

3. 나만의 은행을 직접 시작할 수 있나요?

It’s not possible to create a bank solely for personal use. Regulatory agencies require banks to serve the financial mainstream, maintain capital adequacy, and meet public service standards, just as specialised financial CRMs, like InvestGlass for therapists and healthcare practices, must align with sector-specific compliance and client-care expectations. However, you could establish a private credit union or investment network under strict legal and financial oversight.

4. 나만의 은행을 설립하는 것이 합법인가요?

네, 합법적이지만 엄격하게 규제됩니다. 해당 국가의 중앙은행 또는 금융 당국(예: 필리핀의 경우 필리핀 중앙은행)으로부터 승인 및 지정을 받아야 합니다. 신청자는 풍부한 경험, 재정 능력, 건전한 사업 계획을 입증해야 합니다.

5. 개발 파이낸싱이란 무엇인가요?

개발 금융은 특히 저소득층이나 신흥 지역의 경제 성장 프로젝트를 지원하기 위해 제공되는 자금을 말합니다. 주로 인프라, 농업 또는 소규모 기업을 대상으로 하며, 지역사회가 공식 경제에 진입하고 지역의 재정 문제를 해결할 수 있도록 지원합니다.

6. 지역 개발 은행은 기존 은행과 어떻게 다른가요?

지역사회 개발 은행은 이익을 극대화하기보다는 서비스가 부족한 지역을 지원하는 데 중점을 둡니다. 이들은 신용 협동조합 이용 기회 개선, 자격 있는 신청자 지원, 지역 금융망 구축과 같은 사회적 영향을 통해 성공을 평가합니다.

7. 커뮤니티 개발 은행 자금은 누가 신청할 수 있나요?

지원 자격은 일반적으로 지역사회 발전을 목표로 하는 중소기업, 비영리단체, 지방 정부, 기업가 등입니다. 신청 절차에는 일반적으로 재정 서류, 프로젝트 제안서, 지역사회에 미치는 영향에 대한 증명이 필요합니다.

8. 개발 은행은 대출 신청을 어떻게 평가하나요?

재정적 실행 가능성, 사회적 영향, 위험 평가를 기준으로 평가합니다. 신청자의 경험, 비즈니스 실적, 프로젝트의 개발 목표와의 일치 여부가 승인에 중요한 요소입니다.

9. 개발 은행은 어떤 문제를 해결하는 데 도움을 주나요?

개발 금융 기관은 신용 부족, 인프라 부족, 농촌 지역 투자 부족 등 금융 시장의 공백을 해결합니다. 이들은 접근 가능한 금융 지원과 장기적인 지원을 제공함으로써 지역 사회가 지속 가능한 성장 주기에 진입하도록 돕습니다.

10. 내 지역의 개발 은행은 어떻게 찾을 수 있나요?

국가 금융 디렉토리, 지방 정부 웹사이트 또는 개발 금융 네트워크를 검색하는 것부터 시작할 수 있습니다. 예를 들어 필리핀의 경우, 공인된 개발 은행은 재무부 또는 BSP에 등재되어 있는 경우가 많습니다.