CRM data transforms into a financial decision-making engine when it is comprehensive, accurate, and integrated with core banking, portfolio, and accounting systems. A customer relationship management system plays a vital role in unifying sales and finance data, allowing firms to evolve beyond basic contact management and tracking into strategic intelligence.

Grasping the essential features of a CRM is crucial for financial institutions to maximise CRM data for improved financial decision-making. These features enhance pricing, risk evaluation, liquidity planning, and profitability analysis throughout the 2024 and 2025 planning cycles.

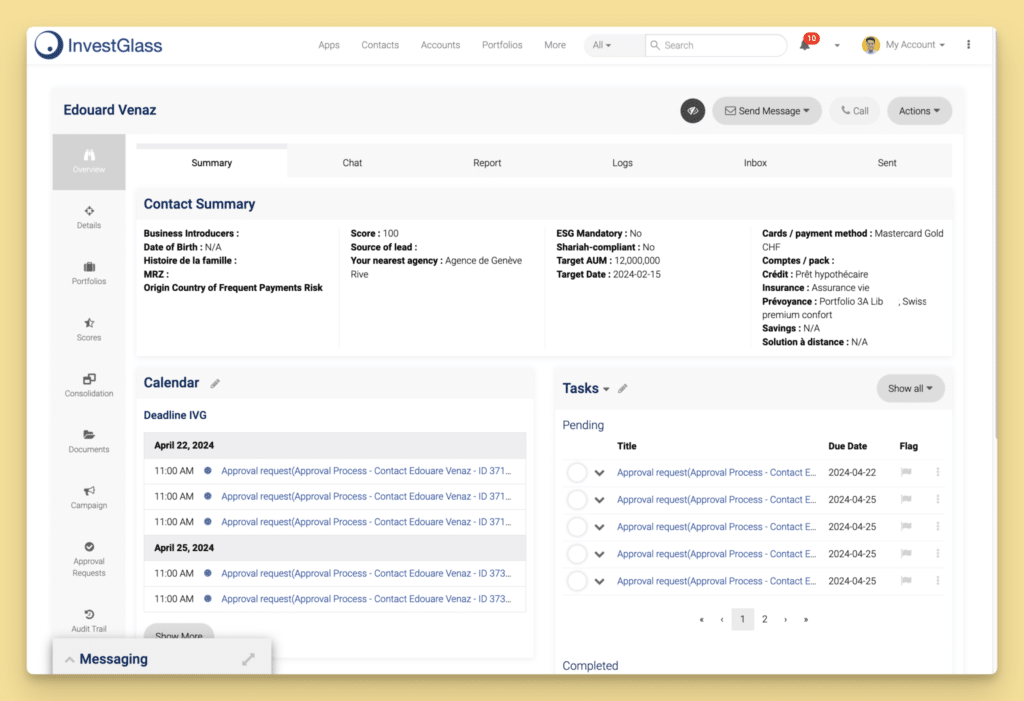

InvestGlass, as a Swiss sovereign CRM and all-in-one automation platform, enables firms to consolidate client, portfolio, and onboarding data within Switzerland, ensuring compliant decision-making under Swiss data protection laws and GDPR.

Practical applications encompass dynamic client segmentation, evaluating product profitability, recommending the next best actions, and real-time forecasting that connects front office activities directly to balance sheet outcomes.

This article provides a straightforward, step-by-step guide to transform fragmented data into a decision-grade CRM framework that delivers tangible financial advantages.

Introduction: Evolving from a Customer Relationship Management Database to a Financial Decision Engine

Imagine a mid-sized Swiss wealth manager in 2024 using separate systems for customer relationship management, portfolio management, and accounting. Advisors spend extensive time reconciling spreadsheets, while finance leaders struggle to answer basic questions about client profitability and pricing optimisation.Although the data exists, it is siloed, preventing a complete view necessary for confident financial decisions. Without consistent data across these systems, reliable financial decision-making becomes more difficult as gaps and inaccuracies erode trust.

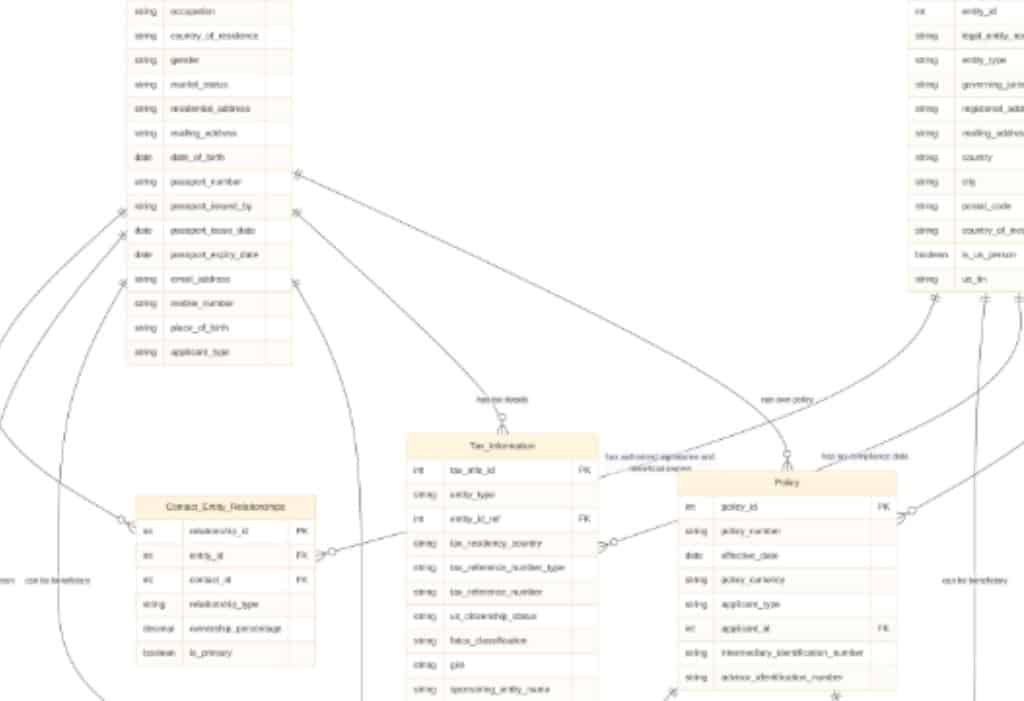

In the financial services sector, CRM data encompasses far more than just contact information and meeting notes. It includes detailed client profiles, KYC documentation, interaction histories, product holdings, cash flow records, service requests, and patterns of client behaviour that reveal how customers engage with your organisation. When financial institutions manage this data effectively—ensuring it is well-structured, consistent, and interconnected—it transforms from a static repository into a powerful, dynamic tool for informed decision-making.

This guide illustrates how banks, wealth managers, insurers, and asset managers can harness integrated CRM and financial data to make quicker, more accurate financial decisions at the levels of individual relationships, products, and overall balance sheets. We emphasise practical applications relevant to the financial planning cycles of 2024 and 2025.

InvestGlass, a Swiss-hosted CRM and automation platform, is used by regulated financial institutions to consolidate these diverse data points while adhering to Swiss data sovereignty regulations. Throughout this article, we will demonstrate how firms leverage InvestGlass to build a robust, decision-grade CRM foundation that links client engagement directly to financial performance.

Step 1: Establish a Decision-Ready CRM Data Foundation

Meaningful financial decisions require accurate, well-structured, and properly permissioned data within your CRM systems, rather than scattered contact notes or informal relationship tracking. To extract actionable insights, your data foundation must be robust enough to support the analyses you plan to undertake.

A high-quality CRM dataset in finance includes several critical components:

Veri Kategorisi | Temel Unsurlar |

|---|---|

Müşteri Profilleri | KYC profillerini, risk profillerini, yatırım hedeflerini, belgelenmiş tercihleri tamamlayın |

İlişki Hiyerarşileri | Hane yapıları, tüzel kişilik ilişkileri, intifa hakkı sahipliği |

Portföy Verileri | Varlıklar, değerlemeler, performans geçmişi, görev türleri |

Etkileşim Kayıtları | İletişim geçmişi, toplantı notları, hizmet talepleri, kampanya yanıtları |

Finansal Metrikler | Gelir ilişkilendirmesi, ücret yapıları, hizmet maliyetleri, karlılık göstergeleri |

Consider a Swiss private bank that consolidated data from its core banking system, portföy yöneti̇m araci, and email communications into InvestGlass during 2024. Previously, advisors lacked visibility of total relationship value alongside recent client interactions. After integration, they identified that some clients generating modest fee revenue were among the most engaged, indicating opportunities for relationship growth. |

Standardised data models are essential. When clients, households, entities, accounts, and products adhere to consistent frameworks, it becomes possible to accurately link revenue, costs, and risks across the organisation. Without such data consistency, aggregating client information is challenging, leading to unreliable insights that hinder strategic decision-making.

Regular data quality checks, conducted daily or weekly, help identify issues before they affect reporting. Typical problems include missing risk ratings, incorrect contact details, or mismatched currency information. Automated validation features within your CRM can highlight these discrepancies early, allowing operations teams to resolve them proactively instead of discovering errors during critical reporting periods.

Step 2: Integrate CRM Data with Financial and Risk Systems

Customer relationship management alone does not suffice for effective financial decision-making. The true advantage is realised when your CRM seamlessly integrates with essential systems such as core banking, portfolio management, treasury, and accounting software, providing a comprehensive view of each client relationship alongside its financial implications.

InvestGlass acts as the central hub within your technology ecosystem, synchronising data securely with platforms like Avaloq, Temenos, or bespoke portfolio engines through APIs hosted in Switzerland.This financial-services-focused CRM and automation system eliminates manual data entry between systems and ensures advisors and finance teams operate from a single source of truth.

Effective integration involves several specific data flows:

- Portföy sistemlerinden CRM'e aktarılan günlük pozisyonlar ve değerlemeler

- Muhasebe yazılımından ücretlerin, komisyonların ve işlem maliyetlerinin toplu olarak içe aktarılması

- Risk platformlarından risk puanlarının, kredi derecelendirmelerinin veya derecelendirme geçişlerinin gecelik güncellemeleri

- Real-time alerts when key thresholds are breached across any connected system

With these connections, finance teams gain the ability to view client-level profitability, product margins, and cash flow schedules directly within CRM dashboards. This integration eliminates the need for spreadsheet reconciliations, minimises errors, and speeds up decision-making processes.This removes the need for spreadsheet reconciliations, reducing errors and accelerating decision-making cycles.

Consider a 2025 example where an insurer integrates CRM and policy administration data to refine underwriting strategies by segment. By analysing historical claims frequency alongside client behaviour patterns stored in the CRM, the risk team identifies that highly engaged policyholders in certain segments have significantly better loss ratios. This insight guides both pricing decisions and the allocation of marketing resources towards the most profitable customer groups.

Integrating CRM with Accounting Software

Connecting customer relationship management systems with accounting software is a critical step for financial institutions aiming to streamline operations and enhance client relationships. By linking CRM with accounting platforms, firms gain a consolidated view of customer interactions and financial data, enabling more informed, data-driven decisions organisation-wide.

This integration automates routine tasks and significantly reduces manual data entry, freeing up valuable time for customer service representatives and advisors to focus on improving client engagement. For instance, when a CRM like Salesforce Financial Services Cloud integrates with accounting software, all relevant customer interactions, transaction histories, and financial records synchronise in real-time. This guarantees both front office and finance teams access the same current information, improving accuracy and consistency in client communications.

With a unified view of customer financial data and relationship history, businesses can personalise their services, respond more promptly to client needs, and identify opportunities for cross-selling or upselling. Automated workflows triggered by financial events, such as overdue invoices or major account changes, enable proactive outreach and tailored support, further enhancing client engagement.

Ultimately, integrating CRM with accounting software converts raw data into actionable insights, supporting data-driven decisions that boost business performance and client satisfaction. By eliminating data silos and streamlining processes, financial institutions can provide a seamless customer experience while maintaining robust operational controls.

Step 3: Leverage CRM Data to Enhance Client-Level Financial Decisions

The initial application of CRM data for financial decisions occurs at the individual client or household level where financial advisors operate daily. CRM systems help build and sustain strong client relationships, which are vital for success in financial services. Here, enhanced customer insights directly translate into improved client relationships and stronger business results.

Advisors in 2024 and 2025 face several key decisions benefiting from integrated CRM data:

- Developing investment proposals based on comprehensive risk profiles and historical preferences

- Adjusting credit limits informed by relationship profitability and behavioural patterns

- Pricing advisory mandates that reflect true service costs and client value

- Prioritising outreach based on engagement trends and revenue potential

By combining communication history with portfolio performance and risk profile data, advisors can recommend products that better suit client needs. This method enhances customer service quality while minimising the risk of mis-selling, which is crucial for maintaining regulatory compliance and protecting the institution’s reputation. Effective CRM data management turns scattered customer information into organised intelligence, driving measurable sales performance and enabling teams to close deals faster.

A practical example: a wealth manager calculates recurring fee revenue and estimates the service costs per client by considering factors such as meeting frequency, administrative requests, and the complexity of portfolio reporting. The resulting analysis reveals:

Müşteri Katmanı | Yıllık Gelir | Hizmet Maliyeti | Net Kâr | Müşterilerin Yüzdesi |

|---|---|---|---|---|

Karlı | 15.000 CHF üzeri | 5.000 CHF'nin altında | 10.000 CHF üzeri | 25% |

Marjinal | 8,000 ila 15,000 CHF | 5,000 ila 8,000 CHF | 0 ila 7.000 CHF | 45% |

Zarar Etme | 8.000 CHF'nin altında | 8.000 CHF üzeri | Negatif | 30% |

This segmentation informs different strategies: personalised services and proactive outreach for profitable clients, efficiency improvements for marginal relationships, and fee discussions or service model changes for loss-making accounts. Financial CRM software assists businesses in enhancing customer interactions, simplifying lead management, and delivering personalised services that exceed expectations. |

InvestGlass workflows can automatically trigger alerts when a client’s profitability drops below a set threshold or when cash balances exceed a specified idle cash ratio. These timely notifications empower advisors to intervene promptly, preventing minor issues from escalating and enhancing client management across the portfolio. This capability is especially valuable for institutions seeking the best CRM for private banks.

Step 4: Use CRM Insights to Inform Portfolio and Product Decisions

Beyond individual client interactions, aggregated CRM data reveals which products and mandates are truly profitable after factoring in acquisition costs, servicing efforts, and client retention. This analysis often challenges assumptions based solely on headline fee rates.

The approach involves categorising clients by portfolio type, mandate category, and risk profile within the CRM, then evaluating realised margins, portfolio outcomes, and retention statistics across these segments. Predictive analytics can further forecast future profitability based on observed client behaviour.

For example, in 2024, a wealth manager compared two popular offerings: a low-fee discretionary mandate and a higher-fee execution-only service. While initial gross margin analysis favoured the execution-only product, a full allocation of service costs—including trade support, reporting demands, and relationship management time—revealed that the discretionary mandate generated significantly higher net margins. Moreover, discretionary clients showed retention rates averaging 92%, compared to 78% for execution-only clients.

This insight prompted the firm to reorient marketing automation campaigns away from execution-only products towards discretionary mandates with superior risk-adjusted returns. Client acquisition strategies became more focused, targeting prospects more likely to adopt the higher-retention offering.

In addition to profitability, CRM-linked portfolio analytics assist finance and risk teams in monitoring product risk concentrations. They track exposures by sector, currency, ESG rating, and other dimensions across the client base. When thresholds are exceeded, workflow automation triggers alerts and reviews before regulatory or internal policy breaches occur. These capabilities can be integrated with AI-driven portfolio management strategies to optimise risk-adjusted performance.

Step 5: Forecast Revenue, Liquidity, and Capital Using CRM Data

CRM data serves as a leading indicator, empowering financial leaders to forecast revenue and liquidity more proactively than relying solely on accounting figures. While financial reports reflect historical performance, CRM insights offer a forward-looking perspective, enabling timely and informed financial planning. While financial reports reflect past performance, CRM data provides insight into likely future outcomes, allowing proactive planning.

Opportunity pipelines, mandate renewals, and anticipated inflows or outflows recorded within the CRM can inform monthly revenue forecasts spanning six to twelve months. This approach shifts financial planning from a retrospective exercise to a proactive, forward-looking strategy.

For example, a Swiss asset manager in 2025 uses InvestGlass to model scenarios based on:

- Conversion rates for prospects at various pipeline stages

- Müşteri segmentine göre yeni görevler için ortalama bilet büyüklüğü

- Seasonal redemption patterns from historical data

- Müşteri katılım puanları ile bilgilendirilen yetki yenileme olasılıkları

By adjusting these variables, finance teams can create optimistic, baseline, and pessimistic revenue forecasts with well-documented assumptions. This structured, data-driven approach replaces guesswork with rigorous analysis that can be tested and refined over time.

Treasury and asset liability management teams also benefit from these forecasting capabilities. Expected client cash flows derived from CRM data enhance liquidity management and capital planning, particularly for term deposits and structured products where timing is crucial. Real-time access to CRM-based forecasts enables treasury to adapt positions as client behaviour changes.

Regulators and internal risk committees in FINMA-supervised institutions require transparent documentation of assumptions behind financial projections. CRM-driven forecasting provides audit trails that satisfy these demands, offering clear evidence of the customer data and historical information underpinning the forecasts.

Step 6: Support Risk Management and Compliance Decisions with CRM Data

CRM data is also critical for risk and compliance management, not just sales. European and Swiss regulations require firms to demonstrate understanding of clients and maintain appropriate controls.

Onboarding, KYC, and suitability records stored within InvestGlass, combined with automated KYC verification workflows, support risk-based decision-making throughout the client lifecycle. Examples include:

- Tightening trading limits for high-risk jurisdictions

- Siyasi olarak maruz kalan kişiler için gelişmiş izleme

- Adjusted service models for clients with complex beneficial ownership

- Scheduling periodic reviews based on risk classification rather than arbitrary intervals

In 2024, monitoring uncovered behavioural patterns that often signalled potential compliance issues, such as frequent changes of address, large cash transactions inconsistent with declared sources of wealth, and unexpected cross-border activities. Identifying these patterns through CRM analysis enables compliance teams to initiate timely reviews, preventing problems from escalating.

CRM segmentation helps compliance allocate enhanced due diligence and review resources according to actual risk, improving operational efficiency while ensuring high-risk relationships receive appropriate attention.

For firms required to keep regulatory and client records within Swiss borders, data sovereignty is essential. InvestGlass provides hosting options in Swiss data centres or on-premise deployments, ensuring that sensitive customer data and compliance documents remain securely within the appropriate jurisdictional boundaries.

Step 7: Employ AI and Automation to Transform CRM Data into Action

Once CRM data is structured and integrated, AI can assist decision-making by recommending next best actions and predicting outcomes. Modern CRM platforms with AI tools enable users without advanced technical skills to manage data, utilise automation, and access information through intuitive interfaces. This converts raw data into practical guidance advisors and risk officers can act on promptly.

InvestGlass AI evaluates leads and existing clients for upsell opportunities or retention risks by analysing indicators such as:

- Engagement measured by email opens, portal logins, and meeting frequency

- Karşılaştırma ölçütlerine ve müşteri beklentilerine göre portföy performansı

- Hizmet bileti sıklığı ve çözüm memnuniyeti

- Life event indicators suggesting changing financial needs

AI automates tasks that would otherwise require hundreds of manual hours, including duplicate detection, record enrichment, format validation, and extracting details from emails and documents. AI continuously monitors data quality, flags issues as they arise, and makes sophisticated data management accessible via simple interfaces. It reduces manual data work by 41%, allowing sales teams to concentrate on building relationships. Organised data helps sales teams close deals 23% faster, as they spend more time selling rather than searching for information. Built-in AI tools also identify trends, such as seasonal demand spikes, informing staffing and inventory planning.

In 2024, an advisory team utilised AI to prioritise quarterly client reviews whenever portfolios deviated beyond set thresholds. The system automatically identified 47 relationships requiring attention, which would have otherwise been recognised only after a significant delay. Workflow automation works alongside AI by managing tasks, reminders, and approvals based on quantitative criteria. For example, a portfolio experiencing a drawdown exceeding acceptable limits triggers a review task, while low fee coverage ratios generate alerts for account management. These automated processes guarantee consistent enforcement of business rules throughout the organisation. Transparency is essential when employing AI for financial decisions. Advisors and risk officers need to understand the data points influencing recommendations to ensure accountability and regulatory compliance. InvestGlass offers clear explanations of AI scoring factors, enabling firms to justify their recommendations when necessary.

Measuring CRM Return on Investment (ROI)

Understanding CRM ROI is essential for financial institutions seeking to justify technology investments and stimulate growth. Measuring ROI involves weighing costs, such as implementation, maintenance, and training, against tangible benefits like increased revenue from improved customer relationships and more efficient sales processes.

Research from Nucleus Research shows organisations implementing CRM can achieve an average ROI of 245%, with some realising returns up to 600%. These gains stem from enhanced customer service, streamlined sales, and higher satisfaction, all contributing to increased revenue and client loyalty.

To measure CRM ROI accurately, firms should monitor key performance indicators such as sales conversion rates, client retention, average revenue per client, and customer satisfaction before and after CRM deployment. Improvements in these areas can be directly linked to better management of customer relationships and effective use of CRM data.

Additionally, institutions should consider time saved through automation and reduced manual work, plus improved compliance and reporting. Regularly reviewing these outcomes ensures CRM systems continue to deliver measurable growth and support strategic goals.

Overcoming Common CRM Challenges

Successful CRM implementation in financial services requires addressing common obstacles like data quality, user adoption, and system integration. Tackling these challenges is vital to achieving enhanced client management, customer satisfaction, and business results.

Data quality is often the primary challenge. Inaccurate, incomplete, or outdated CRM data undermines decisions and trust. Firms should establish regular data validation, enforce consistent entry standards, and use automated tools to flag issues. Maintaining accurate, current CRM data is fundamental to effective client management.

User adoption is crucial. Even the best CRM fails without user comfort. Comprehensive training, ongoing support, and clear communication of benefits promote adoption and maximise value. Involving users in CRM selection and configuration increases buy-in and ensures suitability.

Integration with systems like accounting software is essential for a unified customer view and streamlined processes. Seamless integration reduces manual entry, minimises errors, and enables comprehensive client and financial analysis.

Proactively addressing these challenges unlocks CRM potential, leading to better client management, higher satisfaction, and stronger outcomes.

Best Practices for CRM Data Security

Protecting sensitive client data is paramount for financial institutions using CRM. Following best practices safeguards information, supports compliance, and builds client trust.

Key measures include robust encryption for data at rest and in transit, strict access controls with role-based permissions, and regular backups to prevent data loss and enable recovery.

Compliance with regulations like GDPR is mandatory. Firms should maintain clear data retention policies and configure CRM systems to support regulatory needs. Regular audits ensure ongoing alignment and enable swift responses to threats.

Using a customer data platform (CDP) can enhance data management by unifying customer data across systems, improving security and efficiency. Even specialised deployments such as CRM for Swiss dental practices benefit from the same principles of secure data centralisation. Staff training and awareness are vital to maintain a strong security culture.

Adhering to these practices ensures CRM data security and integrity, enabling better client management and positive business results while maintaining client trust.

Implementing a CRM Data Strategy for Enhanced Financial Decisions

This section presents a practical roadmap for firms beginning in 2024, aiming to achieve measurable improvements in decision-making within 6 to 12 months. The phased strategy manages complexity effectively and delivers clear value at each stage.

1. Aşama: Keşif ve Veri Denetimi (1 ila 4. Haftalar) Evaluate data quality across CRM, portfolio, and financial systems. Identify gaps, inconsistencies, and integration requirements. Document decision-making processes that would benefit from enhanced data.

2. Aşama: Temel Sistemlerin Entegrasyonu (5 ila 12. Haftalar) Link CRM with core banking, portfolio management, and accounting platforms. Set up automated data flows and validation procedures to reduce manual data entry.

Phase 3: Deployment of Decision Dashboards (Weeks 13 to 20) Launch dashboards showcasing client profitability, product margins, and pipeline forecasts. Train finance and front office teams on their use. Replace spreadsheet analyses with CRM-generated reports.

Phase 4: Introduction of AI and Automation (Weeks 21 to 30) Implement scoring models to assess retention risks and upsell opportunities. Deploy automated alerts and task management based on business rules. Refine models using initial feedback.

Firmalar ilerlemeyi takip etmek için 3 ila 5 ölçülebilir hedef belirlemelidir:

- Gelir tahmini doğruluğunu 6 ay içinde 15% artırın

- Manuel elektronik tablo mutabakatlarını ayda 20 saat azaltın

- Müşteri karlılığı görünürlüğünü 60%'den 95% ilişkiye yükseltme

- 30% ile düzenleyici raporları hazırlama süresini azaltın

InvestGlass projects typically start with digital onboarding and KYC processes, which immediately improve data quality and consistency. Building on this strong foundation, firms then expand their capabilities to include portfolio dashboards, marketing automation, and risk management workflows. This phased approach ensures that each stage leverages verified data from the previous steps, creating a seamless and reliable progression.

Looking ahead, firms preparing for 2026 and beyond should anticipate rising customer expectations and regulatory demands. Building a solid CRM foundation today enables rapid adaptation, whether incorporating new data sources, adopting advanced analytics, or meeting emerging compliance requirements.

Why Choose InvestGlass for CRM-Driven Financial Decisions

InvestGlass is a Swiss sovereign CRM, portfolio management, and client portal platform specifically developed for regulated financial institutions. Unlike general CRM systems adapted for financial services, InvestGlass is purpose-built from the ground up to support banking, wealth management, and insurance workflows.

Key strengths for improved financial decisions include:

- Entegre Dijital Onboarding ve KYC: Comprehensive client files from day one, with document management and suitability assessment embedded

- Portföy Raporlama: Real-time portfolio views linked to CRM client records enable true relationship-level profitability analysis

- Pazarlama Otomasyonu: Campaign management targeting clients based on financial characteristics, not just demographics

- İş Akışı Otomasyonu: Business rules triggering tasks, alerts, and approvals based on financial thresholds and risk indicators

- Müşteri Portalı: Self-service access reducing administrative workload while enhancing client engagement

InvestGlass is hosted in Switzerland or available for on-premise deployment, fully supporting Swiss data protection laws, GDPR, and the internal data residency policies of banks and asset managers. This setup addresses common concerns that often limit the adoption of cloud-based CRM solutions. Its typical clients include private banks, external asset managers, family offices, insurers, fintech companies, and specialised users such as therapists who require integrated CRM tools to manage customer relationships throughout the client lifecycle. These organisations benefit from having CRM, compliance, and portfolio management capabilities combined within a single platform, avoiding the complexity of multiple disparate systems. Unlike competitors such as Salesforce Financial Services Cloud, HubSpot, and Microsoft Dynamics 365, InvestGlass offers Swiss data sovereignty alongside financial services-specific functionality tailored to the needs of regulated institutions. The platform empowers firms to improve client engagement while ensuring the highest standards of data security and regulatory compliance. For organisations interested in unifying their financial and CRM data into actionable dashboards and workflows, InvestGlass provides customised demonstrations aligned with their unique data environments and use cases.

SSS

How quickly can a financial institution start using CRM data for better decisions?

Most banks and wealth managers experience noticeable improvements in decision-making within 60 to 90 days when implementing targeted pilots such as revenue forecasting or client profitability analysis. This process generally involves a two-week data evaluation, followed by a four to six-week integration phase with core systems, and concludes with a concise training period for finance and front office teams. InvestGlass adopts this structured approach, ensuring minimal disruption to existing core banking operations and enabling firms to validate benefits before scaling up.

What financial metrics should be tracked inside the CRM?

Key metrics encompass relationship-level revenue, client service costs, assets under management, net new money, fee coverage ratios, and product-specific margins. Each metric should be accurately linked to corresponding CRM fields and data sources to maintain consistency and auditability in dashboards over time. Combining metrics such as profit per client segment requires integrating CRM engagement data with accounting inputs, underscoring the importance of seamless system integration for effective financial reporting.

Is it safe to store sensitive financial data in a CRM platform?

For regulated institutions, ensuring safety relies on the CRM provider’s security framework, hosting environment, data encryption, and access controls. InvestGlass delivers hosting within Swiss data centres or offers on-premise deployment options, featuring role-based access and comprehensive audit trails tailored to the requirements of banking and wealth management. The platform adheres to regulatory standards such as FINMA circulars and GDPR, giving compliance and risk officers confidence in the protection of sensitive financial data.

Do smaller advisory firms benefit from CRM-driven financial decisions?

Independent asset managers and small advisory boutiques often gain significant advantages from structured CRM data, as it replaces manual spreadsheets and reliance on individual memory with systematic, efficient processes. Small teams, even those with fewer than ten advisers, can utilise InvestGlass to centralise client information, monitor recurring revenue, track client interactions, and forecast cash flows without needing dedicated analysts. The platform’s cloud-based access and ready-made templates minimise the necessity for large internal IT resources, bringing enterprise-level capabilities within reach of smaller firms.

How does CRM data assist with regulatory reviews and audits?

Regulators increasingly demand comprehensive client records, detailed documentation of advice, and clear proof of suitability and KYC compliance. A unified CRM platform like InvestGlass securely archives onboarding documents, risk assessments, investment recommendations, client feedback, and interaction logs complete with timestamps and user details. This organised and traceable data repository facilitates quicker audit responses, lowers operational risks during regulatory examinations, and evidences strong processes for managing customer relationships and meeting compliance requirements.

İlgili makaleler

İsviçre Egemen CRM: Yapay Zeka Üzerine Kurulu.

Hareket etmeye hazır.